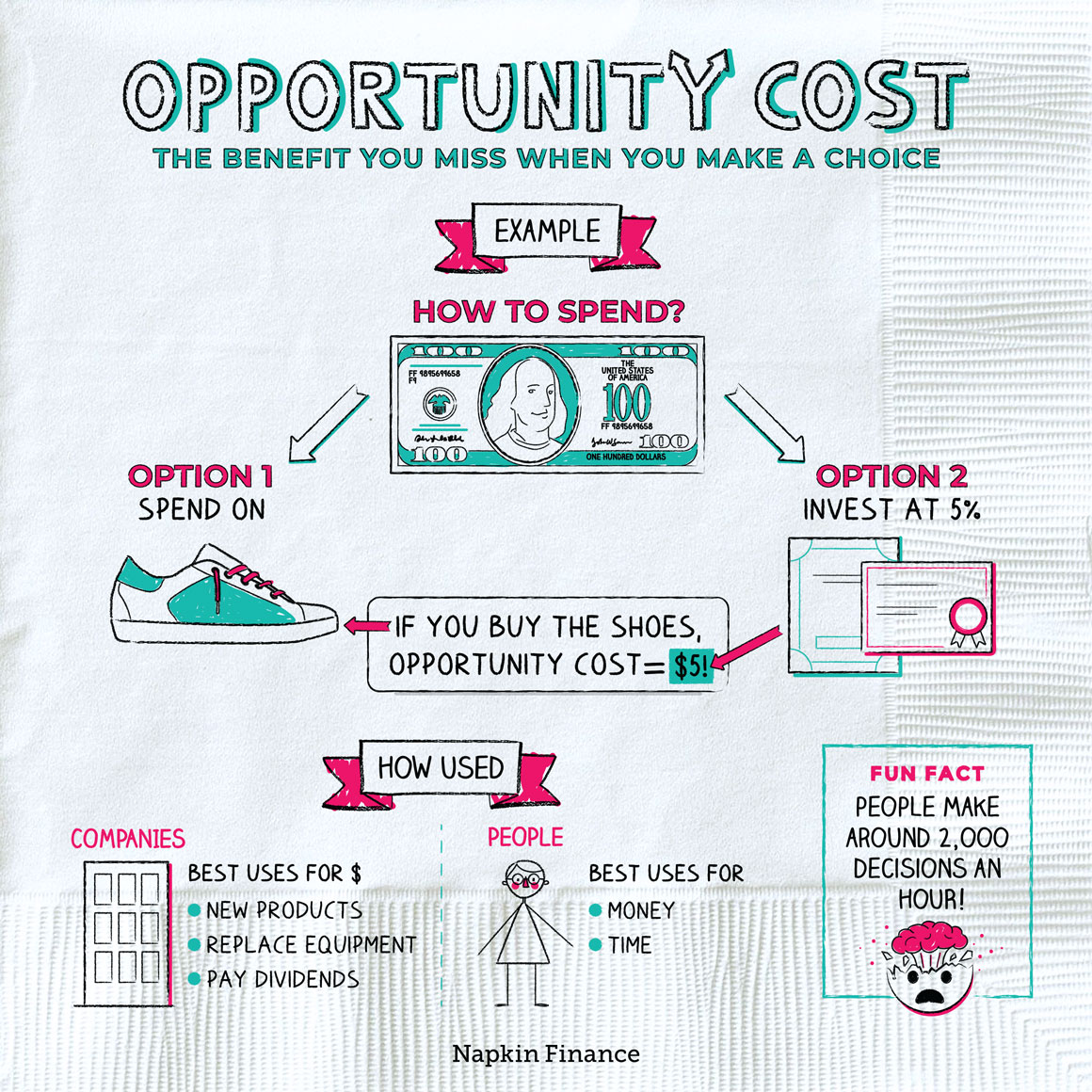

In the world of finance, every choice carries a hidden price tag. Whether you are managing a household budget, overseeing a corporate portfolio, or deciding where to allocate your next $1,000 investment, you are constantly making trade-offs. This fundamental economic principle is known as “opportunity cost.”

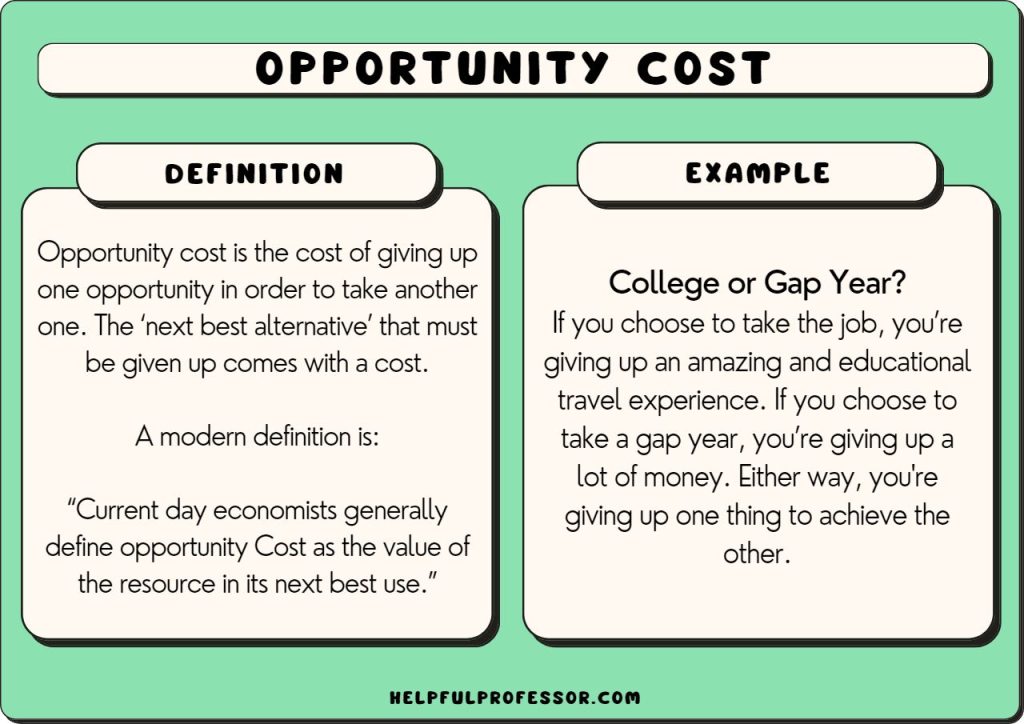

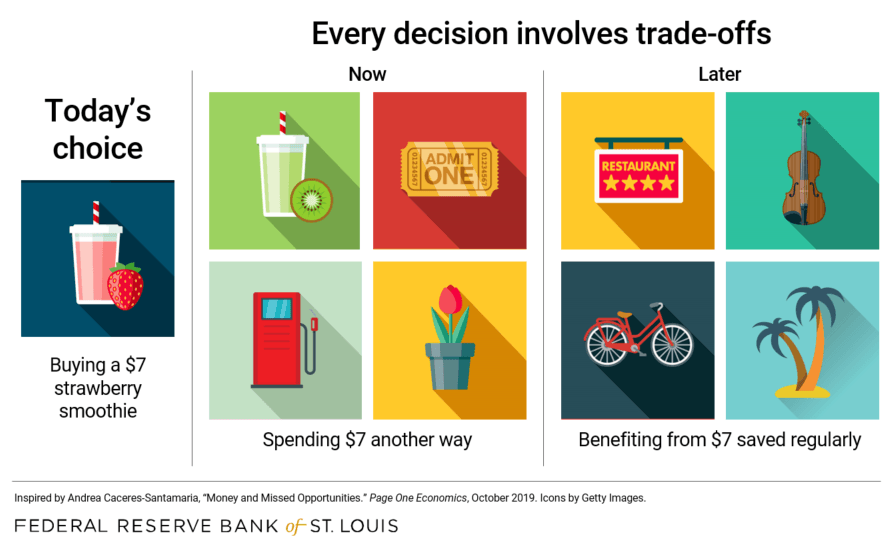

Simply put, opportunity cost is the value of the next best alternative that you give up when making a decision. It is not necessarily the monetary cost of an item, but rather what you could have done with those resources—time, money, or effort—had you chosen differently. In the “Money” niche, understanding this concept is the difference between passive wealth erosion and proactive financial growth. By mastering the calculation of opportunity cost, you can optimize your personal finance strategy and ensure that every dollar is working at its maximum potential.

1. The Fundamentals of Opportunity Cost in Personal Finance

Opportunity cost is often invisible because it represents a “lost” path rather than a direct expense on a bank statement. In personal finance, this concept is most prevalent in the daily tension between immediate consumption and long-term wealth building.

The “Invisible” Cost of Spending vs. Saving

Every time you spend money on a depreciating asset—such as a new car, a designer handbag, or high-end electronics—the opportunity cost is the compounded interest that money could have earned if it were invested in the market.

For example, if you spend $1,000 on a new smartphone today, the “cost” isn’t just the $1,000 out of your bank account. If that same $1,000 were placed in an index fund with an average annual return of 7%, it would be worth approximately $1,967 in ten years. Therefore, the true opportunity cost of the smartphone is nearly $2,000 of future wealth. Recognizing this allows individuals to shift their mindset from “What does this cost?” to “What am I sacrificing for this purchase?”

Time as a Currency in Side Hustles

In the realm of online income and side hustles, time is your most precious resource. Opportunity cost applies here when you choose one income stream over another. If you spend five hours a week managing a low-paying freelance gig that earns you $20 an hour, your opportunity cost is the potential revenue from a higher-skilled project or the time spent learning a new certification that could command $100 an hour later.

Successful side hustlers constantly evaluate their “hourly rate vs. growth potential.” If your side hustle prevents you from resting or developing a scalable business model, the opportunity cost might be your long-term health or the creation of a passive income stream that could eventually replace your full-time job.

2. Opportunity Cost in Investment Strategy

For investors, opportunity cost is a quantitative tool used to compare the performance of different asset classes. It is the yardstick by which we measure whether our capital is being used efficiently.

Comparing Asset Classes: Stocks vs. Real Estate

Investors often face the dilemma of where to park their capital for the long term. If you decide to invest $100,000 in a rental property, the opportunity cost is the return you would have received by putting that money into the S&P 500 or a diversified bond portfolio.

While the real estate might offer rental income and tax benefits, the stock market might offer higher liquidity and historical growth. If the rental property yields a 5% return while the stock market yields 10%, your opportunity cost for choosing real estate is 5% per year. This doesn’t mean real estate was a “bad” choice—as risk profiles and diversification matter—but it highlights the importance of acknowledging what is being left on the table.

The Cost of Sitting on Cash

In periods of market volatility, many investors feel safer holding cash. However, the opportunity cost of “staying on the sidelines” can be devastating due to two factors: inflation and missed market rallies.

Cash loses purchasing power every year as the cost of living rises. Furthermore, some of the market’s best days often follow its worst days. If you pull your money out of the market during a downturn, the opportunity cost is the rapid recovery you miss when the market rebounds. In the world of “Money,” the cost of “doing nothing” is often the most expensive mistake an investor can make.

3. Business and Corporate Finance Applications

For business owners and corporate executives, opportunity cost is a critical component of capital budgeting. Resources are always finite, and choosing Project A almost always means delaying or canceling Project B.

Capital Allocation and Resource Management

A company with $1 million in surplus capital must decide how to use it. They could reinvest in Research and Development (R&D), pay out a dividend to shareholders, or acquire a smaller competitor.

If the company chooses R&D, the opportunity cost is the immediate value provided to shareholders through dividends or the market share gained through an acquisition. Financial analysts use “Hurdle Rates”—the minimum rate of return on a project—to ensure that the chosen investment exceeds the opportunity cost of other available options. If a project’s expected return is lower than the return from a simple Treasury bond, the opportunity cost is too high to justify the risk.

Scaling vs. Optimizing Current Operations

Many businesses struggle with the “growth vs. efficiency” trade-off. Choosing to scale—hiring more staff, opening new locations—requires massive capital. The opportunity cost is the ability to optimize current operations to become more profitable.

A business that scales too quickly might sacrifice its profit margins. Conversely, a business that focuses too much on optimization might miss a “first-mover advantage” in a new market. Analyzing opportunity cost helps leadership teams determine the “weighted” value of these paths, ensuring that the chosen direction aligns with the company’s long-term financial health.

4. Practical Examples to Master the Concept

To truly internalize opportunity cost, we must look at specific, relatable scenarios that demonstrate how these choices play out over time.

Example 1: The Choice of Higher Education or Immediate Career Entry

Consider a 22-year-old deciding whether to pursue a two-year MBA or enter the workforce immediately.

- The Direct Cost: Tuition and books might cost $100,000.

- The Opportunity Cost: Two years of a starting salary (e.g., $60,000/year) totaling $120,000.

- Total Economic Cost: $220,000.

To justify the degree, the individual must believe that the MBA will increase their lifetime earnings by significantly more than $220,000 to offset the lost wages and the tuition expense. This is why financial experts often suggest looking at the “Return on Investment” (ROI) of a degree rather than just the prestige of the institution.

Example 2: Debt Repayment vs. Investing

One of the most common debates in personal finance is whether to pay off a mortgage early or invest the extra cash in the stock market.

- Scenario: You have an extra $1,000 a month and a mortgage with a 3% interest rate.

- Choice A: Pay down the mortgage. You get a guaranteed 3% return by avoiding interest.

- Choice B: Invest in the stock market. You expect a 7-8% return over the long term.

The opportunity cost of paying down the 3% mortgage is the 4-5% “spread” you lose by not investing in the market. While the peace of mind of a debt-free home has value, the financial opportunity cost is the significant wealth accumulation lost over 15 to 30 years.

5. Integrating Opportunity Cost into Your Financial Routine

How do you apply this without suffering from “analysis paralysis”? The goal isn’t to calculate the cost of every cup of coffee, but to apply the logic to major financial decisions.

Create a Decision Framework

When faced with a significant financial choice—be it a career change, a large purchase, or an investment—ask yourself three questions:

- What is the “Next Best” alternative? (If I don’t buy this, where does the money go?)

- What is the quantifiable return on that alternative? (Interest, growth, or time saved?)

- Does the current choice offer a non-monetary value that outweighs the financial loss? (Sometimes, the opportunity cost of a vacation is high, but the mental health benefits are higher.)

The Power of Automation

One of the best ways to combat the negative effects of opportunity cost in personal finance is to automate the “better” choice. By setting up automatic transfers to your investment accounts, you remove the daily decision-making process. You effectively lower the opportunity cost of “forgetting” to invest or “accidentally” spending your surplus.

Conclusion

Opportunity cost is the silent engine of the financial world. It reminds us that every “Yes” to one expenditure is a “No” to another potential future. In the context of money, investing, and business finance, those who succeed are not necessarily those who make the most money, but those who make the most efficient use of the resources they have.

By evaluating your choices through the lens of what you are giving up, you gain a clearer perspective on your path to financial independence. Whether it’s choosing an index fund over a high-interest savings account or prioritizing a scalable side hustle over a flat-fee gig, understanding opportunity cost ensures that your financial decisions are rooted in strategy rather than impulse. Remember: the most expensive thing you can own is a missed opportunity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.