For the vast majority of individuals, a home is not just a place of shelter; it is the cornerstone of their financial portfolio. Within the realm of personal finance and real estate law, the term “homestead property” carries significant weight, representing a powerful tool for tax savings, asset protection, and long-term wealth preservation. Understanding the nuances of homestead status is essential for any homeowner looking to optimize their financial health and safeguard their equity against unforeseen liabilities.

In its simplest terms, a homestead property is a legal designation for a person’s primary residence. However, the financial implications of this designation are far-reaching. From providing substantial property tax relief to offering a “bulletproof” shield against certain types of creditors, the homestead designation is one of the most beneficial financial provisions available to property owners in many jurisdictions.

The Financial Mechanics of Homestead Laws: Definition and Eligibility

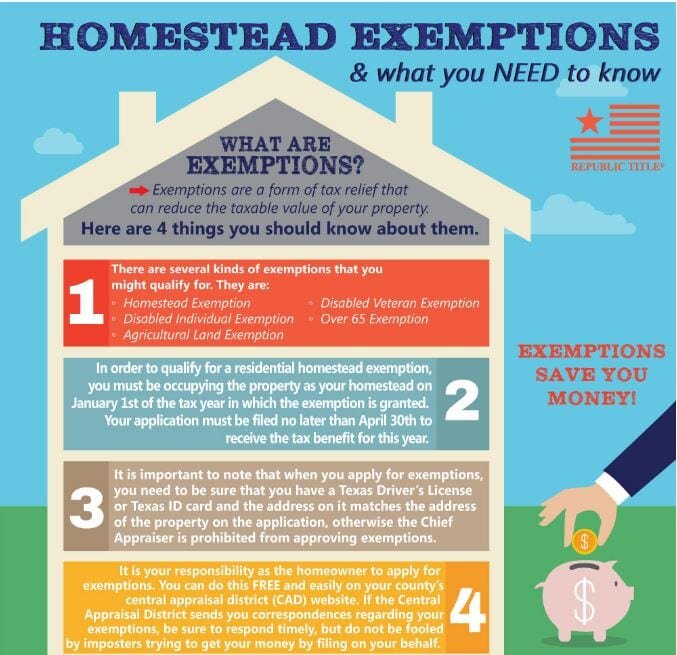

To leverage the financial benefits of a homestead, one must first understand what qualifies a property for this status. While laws vary significantly by state and country, the core principle remains consistent: the property must serve as the owner’s permanent, primary residence.

Primary Residence vs. Investment Property

From a personal finance perspective, the distinction between a primary residence and an investment property is critical. An investment property, such as a rental house or a vacation home, is treated as a business asset. While it offers tax deductions for depreciation and maintenance, it rarely qualifies for homestead protection. A homestead property, conversely, is where the owner lives the majority of the year, is registered to vote, and receives mail. By focusing the “homestead” status on the primary residence, the law aims to protect the stability of the family unit and ensure that individuals are not rendered homeless due to financial misfortune.

Legal Requirements and Documentation

Securing homestead status is rarely automatic. It requires proactive financial management and administrative diligence. Typically, a homeowner must file a “Declaration of Homestead” or a “Homestead Exemption” application with their local county appraiser or tax assessor. The documentation often requires proof of residency, such as a driver’s license matching the address, utility bills, or voter registration. For the savvy investor, ensuring this paperwork is filed immediately after closing on a home is a high-priority task, as the financial benefits often do not apply retroactively.

Maximizing Wealth through Homestead Tax Exemptions

One of the most immediate “Money” benefits of a homestead property is the reduction of annual carrying costs through tax exemptions. In an environment where property values are rising, these exemptions can save a homeowner thousands of dollars every year, effectively increasing their disposable income and improving the property’s overall return on investment.

Reducing Your Property Tax Liability

A homestead exemption typically works by deducting a specific dollar amount or percentage from the home’s assessed value before the property tax is calculated. For example, if a home is valued at $400,000 and the jurisdiction offers a $50,000 homestead exemption, the owner is only taxed on $350,000. Over a 30-year mortgage, the cumulative savings from this reduction can be redirected into retirement accounts, college funds, or further real estate investments.

Long-Term Savings and the “Assessment Cap”

In several high-growth regions, homestead status provides an even more potent financial benefit: a cap on annual assessment increases. For instance, some states limit the increase in a homesteaded property’s assessed value to 3% per year, even if the market value of the home increases by 20%. This creates a significant “tax subsidy” for long-term homeowners. From a wealth-building perspective, this cap makes the cost of homeownership more predictable and protects the owner from being “priced out” of their own home by rising taxes, which is a common risk in gentrifying or booming markets.

Asset Protection: Securing Your Equity from Creditors

In the world of personal finance, “defense” is just as important as “offense.” While many focus on growing their net worth, protecting existing assets from litigation and debt is equally vital. Homestead property laws provide some of the strongest asset protection available under the law.

The Shield Against Unforeseen Financial Liability

In many jurisdictions, the homestead designation protects the equity in a home from being seized to satisfy a judgment from creditors. This means that if an individual is sued—perhaps due to a car accident, a failed business venture, or a professional liability claim—the primary residence remains off-limits to most creditors. In states with “unlimited” homestead protection, such as Florida or Texas, an individual could theoretically own a multi-million dollar home, and it would remain protected even in the face of a massive civil judgment. This makes the homestead property an essential component of a robust asset protection strategy for entrepreneurs and high-net-worth individuals.

Limitations and Exceptions of Homestead Protection

It is a common financial misconception that homestead status protects a home from all debts. There are critical exceptions that every homeowner must understand to avoid a false sense of security. Generally, homestead protection does not apply to:

- Mortgage Foreclosures: If you fail to pay the loan used to purchase the home, the lender can still seize the property.

- Tax Liens: The government can still seize a homestead for unpaid property taxes or federal income taxes.

- Mechanic’s Liens: If you hire a contractor to improve the home and fail to pay them, they can often place a lien on the homestead.

- Past Due Child Support/Alimony: In many areas, family court obligations supersede homestead protections.

Understanding these boundaries is essential for integrated financial planning, ensuring that while the home is protected from “outsider” creditors, the owner remains diligent about “insider” obligations.

Homestead Property in Estate Planning and Wealth Transfer

The financial utility of a homestead property extends beyond the lifetime of the owner. It plays a pivotal role in estate planning, ensuring that a family’s most significant asset is transferred efficiently to the next generation without being eroded by debt or legal complications.

Preserving the Family Legacy

When a homeowner passes away, the homestead status often confers “survivorship rights.” This means that even if the homeowner had significant personal debts at the time of death, the homestead property can often pass to heirs (such as a spouse or children) free and clear of those creditor claims. This ensures that the equity built over decades remains within the family, serving as a legacy and a source of intergenerational wealth rather than being liquidated to pay off medical bills or credit card debt.

Navigating Inheritance and Surviving Spouse Protections

Many jurisdictions have specific “widow/widower” provisions regarding homestead properties. These laws often grant a surviving spouse a “life estate” in the property, allowing them to remain in the home for the rest of their life, even if the property was technically owned solely by the deceased spouse. From a financial planning perspective, this provides an invaluable “safety net,” ensuring housing security for a surviving spouse regardless of the complexities of the deceased’s will or the demands of other heirs.

Conclusion: The Strategic Value of the Homestead

A homestead property is far more than a simple legal definition of where one lives. From a financial standpoint, it is a multi-faceted asset that provides a unique combination of tax efficiency, risk management, and estate security. By securing homestead status, a homeowner is essentially taking out a “free” insurance policy on their equity while simultaneously reducing their annual tax burden.

For anyone serious about personal finance and wealth management, the homestead designation should be viewed as a foundational element of their strategy. It represents a rare instance where the law actively works to protect the individual’s private wealth from the volatility of the economy and the risks of litigation. Whether you are a first-time homebuyer or a seasoned investor, maximizing the benefits of your homestead property is one of the smartest financial moves you can make, ensuring that your home remains not just a place of comfort, but a permanent fortress for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.