For many, the “American Dream” is synonymous with homeownership. It represents stability, equity building, and a sense of belonging. However, there is a precarious financial state that many homeowners find themselves in, often unexpectedly: being “house poor.” In the realm of personal finance, being house poor describes a situation where an individual or family spends a disproportionate amount of their total income on homeownership expenses—including mortgage payments, property taxes, insurance, and maintenance—leaving little to no room for other life necessities, savings, or discretionary spending.

While you may own a beautiful property that is appreciating in value, your daily quality of life might suffer because your liquid cash is swallowed by your four walls. Understanding the mechanics of this phenomenon is essential for anyone looking to navigate the real estate market without sacrificing their long-term financial health.

Defining the “House Poor” Reality: Ratios and Metrics

At its core, being house poor is a matter of cash flow. In the financial world, lenders and advisors often use specific benchmarks to determine how much house a person can actually afford. When these benchmarks are ignored or stretched to their absolute limits, the risk of becoming house poor skyrockets.

The 28/36 Rule and Debt-to-Income (DTI) Ratios

The most common metric used to identify a healthy financial balance is the 28/36 rule. This guideline suggests that a household should spend no more than 28% of its gross monthly income on housing-related expenses and no more than 36% on total debt service (which includes car loans, student loans, and credit cards).

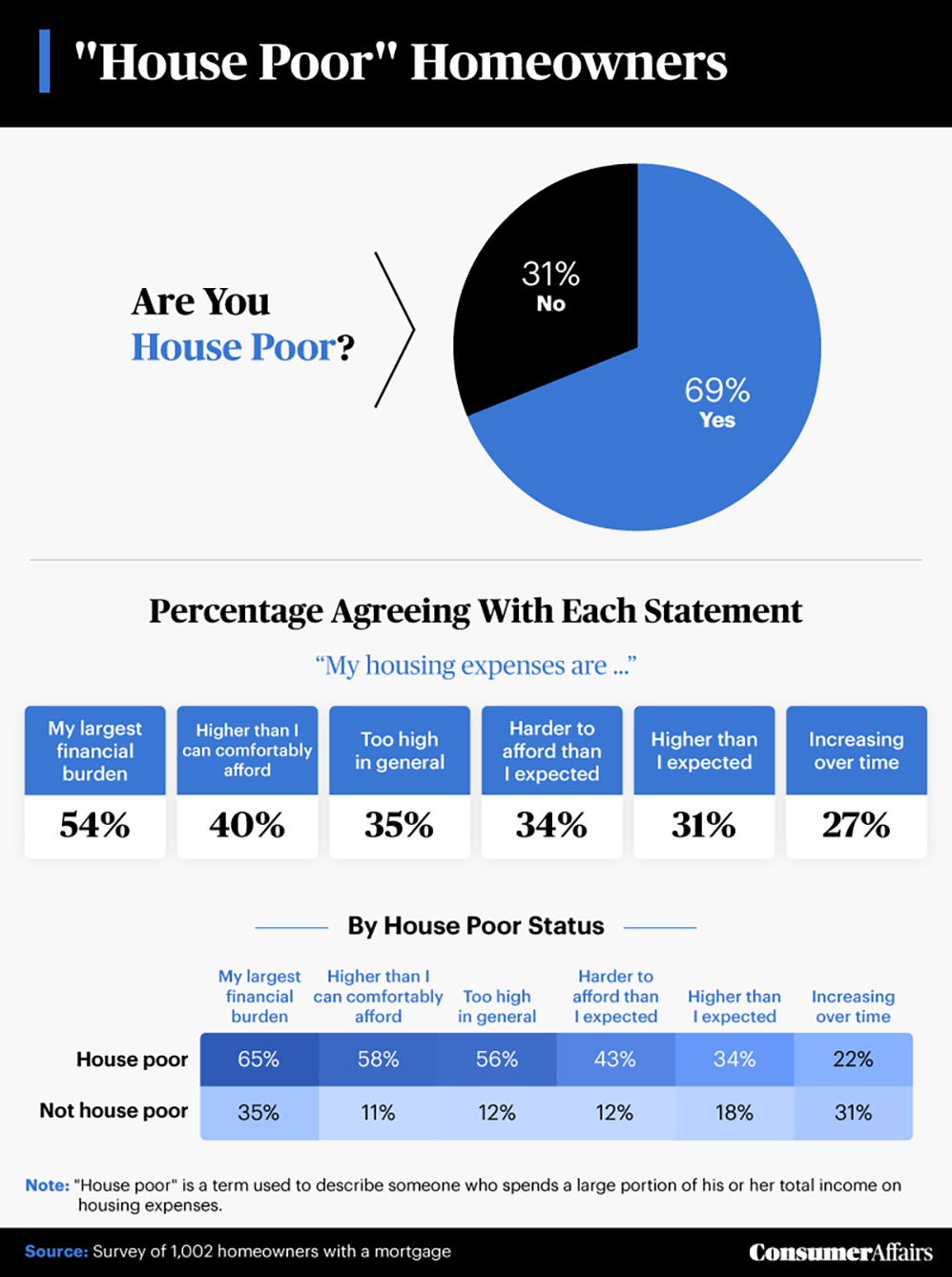

When a homeowner’s housing costs begin to exceed 30% or 40% of their gross income, they enter the “house poor” zone. While a bank might approve a loan with a DTI ratio as high as 43% or even 50% in certain circumstances, doing so often leaves the borrower with insufficient funds for groceries, healthcare, and emergency savings.

The Difference Between Paper Wealth and Liquidity

A critical aspect of being house poor is the disparity between net worth and liquidity. You may have $200,000 in home equity, but if your bank account is empty three days before payday, that equity provides no immediate relief. Real estate is an illiquid asset; you cannot easily “spend” the value of your kitchen or your backyard to pay for a dental emergency or a car repair. This lack of liquidity creates a paradox where a person appears wealthy on paper but lives in a state of constant financial anxiety.

Why Homeowners Find Themselves House Poor

Becoming house poor is rarely a deliberate choice. It is often the result of a combination of market pressures, emotional decision-making, and a lack of foresight regarding the “hidden” costs of maintaining a property.

Overextending in Competitive Markets

In “seller’s markets” where inventory is low and demand is high, buyers often face intense pressure to bid above their comfort zone. The fear of missing out (FOMO) can lead individuals to maximize their borrowing capacity. When a buyer focuses solely on the maximum loan amount a bank is willing to provide, they often fail to account for how that monthly payment will feel when combined with the realities of daily life, such as rising utility costs or inflation.

Underestimating the Total Cost of Ownership

Many first-time buyers calculate affordability based strictly on the PITI (Principal, Interest, Taxes, and Insurance) estimate. However, the true cost of owning a home extends far beyond the monthly mortgage check.

- Maintenance and Repairs: A general rule of thumb is to set aside 1% to 2% of the home’s value annually for maintenance. On a $500,000 home, that is $5,000 to $10,000 a year.

- HOA Fees and Special Assessments: Homeowners Association fees can rise annually, and unexpected “special assessments” for neighborhood repairs can cost thousands of dollars.

- Utility Scaling: Moving from a 1,000-square-foot apartment to a 2,500-square-foot home often results in a doubling or tripling of heating, cooling, and water bills.

The Impact of Variable Expenses and Economic Shifts

Economic volatility plays a significant role in tipping the scale toward being house poor. Property taxes are not static; they are reassessed periodically and can jump significantly if home values in the area rise. Similarly, homeowners insurance premiums have seen record increases in recent years due to climate risks. If a homeowner’s income remains stagnant while these “fixed” housing costs rise, a budget that was once manageable can quickly become unsustainable.

The Ripple Effects on Your Financial Portfolio

Being house poor is not just about having a tight monthly budget; it has long-term implications for an individual’s entire financial trajectory. When the majority of your income is tied up in a single asset, you lose the ability to diversify and grow your wealth in other areas.

Stagnation of Retirement and Investment Portfolios

One of the greatest costs of being house poor is the opportunity cost of missed investments. Compound interest is a powerful tool, but it requires consistent contributions. If a mortgage payment is so high that it prevents you from contributing to a 401(k) or an IRA, you are essentially betting your entire retirement on the appreciation of your home. While real estate generally appreciates, it rarely outperforms a diversified stock market portfolio over the long term, and it carries the risk of localized market crashes.

The Erosion of the Emergency Fund

Financial security is built on the foundation of an emergency fund—typically three to six months of living expenses. For those who are house poor, building this fund is nearly impossible. This creates a dangerous cycle: when a major home repair is needed (like a new roof or HVAC system), the homeowner is forced to rely on high-interest credit cards or HELOCs (Home Equity Lines of Credit), further increasing their monthly debt obligations and deepening their financial strain.

Psychological Stress and Lifestyle Constraints

Money is one of the leading causes of stress and relationship friction. Being house poor often leads to a “lock-in” effect where individuals feel they cannot afford to change jobs, take a vacation, or even dine out with friends. The “dream home” can quickly begin to feel like a “gilded cage,” where the walls represent a financial burden rather than a sanctuary.

Practical Solutions and Exit Strategies

If you find yourself in a house-poor situation, or if you are looking to avoid one, there are several strategic moves you can make to rebalance your finances and regain your peace of mind.

Pre-Purchase Strategy: The “Stress Test”

Before buying a home, it is vital to perform a personal financial stress test. Instead of looking at what the bank allows, look at your net (take-home) pay. Ensure that your total housing costs do not exceed 25% to 30% of your net income, rather than your gross. Additionally, try “living” on the projected mortgage payment for six months while you are still renting. Save the difference between your current rent and the future mortgage; if you find it difficult to manage, you know the house is too expensive for your lifestyle.

Increasing Cash Flow and Reducing Expenses

If you are already in a home and feeling the squeeze, there are two primary levers: increase income or decrease costs.

- House Hacking: Consider renting out a spare bedroom, the basement, or even a garage space to generate passive income that offsets the mortgage.

- Aggressive Budgeting: Use a zero-based budget to identify “leaks” in your spending. While it won’t fix a massive mortgage gap, cutting subscriptions and dining out can provide the breathing room needed to build a small repair fund.

- Appealing Property Tax Assessments: If you believe your home has been overvalued by the county, you can file an appeal to potentially lower your property tax bill.

Long-term Exit Strategies: Refinancing and Downsizing

When the situation becomes untenable, more drastic measures may be necessary to protect your financial future.

- Refinancing: If interest rates have dropped or your credit score has significantly improved since you bought the home, refinancing to a lower rate can reduce your monthly payment. (Note: Always calculate the “break-even” point to ensure the closing costs of the refinance are worth the monthly savings).

- Downsizing: Selling a home that is too expensive and moving into a more affordable property is often the most effective way to “reset” your finances. While it may feel like a step backward, the infusion of cash from the sale and the reduction in monthly overhead can allow you to jumpstart your retirement savings and live a much more stress-free life.

Conclusion: Prioritizing Financial Health Over Property Prestige

Being “house poor” is a modern financial trap that stems from the desire to achieve the ultimate status symbol of success. However, true financial freedom isn’t found in the size of your mortgage or the zip code of your residence; it is found in the flexibility of your capital and the security of your savings.

By understanding the true debt-to-income ratios, accounting for the hidden costs of maintenance, and being willing to make objective decisions about affordability, you can ensure that your home remains an asset rather than a liability. In the world of personal finance, the best house is not necessarily the biggest one—it is the one that allows you to live the rest of your life with confidence and ease.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.