For millions of Americans, Social Security benefits form a critical pillar of their retirement income strategy. It’s a guaranteed stream of income designed to provide financial stability in your later years, yet the question of when to start collecting it is fraught with complexities and often elicits more questions than answers. There isn’t a single “right” age for everyone, as the optimal claiming strategy is deeply personal, influenced by a myriad of factors including your health, financial situation, marital status, and long-term goals. Understanding the various age milestones and the implications of each decision is paramount to maximizing your lifetime benefits and securing your financial future. This comprehensive guide will demystify the age requirements, explore the key factors influencing your choice, and outline strategies to help you make an informed decision about when to start collecting your Social Security.

Understanding Social Security’s Key Age Milestones

The Social Security Administration (SSA) defines several critical age points that dictate how much you can receive in benefits. Missing or misunderstanding these milestones can have a significant and irreversible impact on your retirement income.

Early Retirement Age (ERA): The 62-Year Mark

The earliest age you can begin receiving Social Security retirement benefits is 62. While this option provides immediate income, it comes with a significant and permanent reduction in your monthly benefit amount. The rationale behind this reduction is simple: by starting earlier, you’re expected to receive benefits for a longer period, so the total payout is spread over more months.

The reduction percentage varies based on your Full Retirement Age (FRA). For someone with an FRA of 67, claiming at 62 means a permanent reduction of approximately 30%. This means if your Primary Insurance Amount (PIA) – the benefit you would receive at your FRA – is $2,000, claiming at 62 would reduce your monthly check to around $1,400. This reduction is permanent, meaning your benefit won’t increase to your FRA amount once you reach your FRA, barring cost-of-living adjustments (COLAs). Deciding to claim at 62 might be suitable for individuals with pressing financial needs, those who are unable to work due to health issues, or those with a shorter life expectancy. However, it’s crucial to weigh the immediate cash flow against the long-term impact of a permanently smaller monthly payment.

Full Retirement Age (FRA): The Sweet Spot

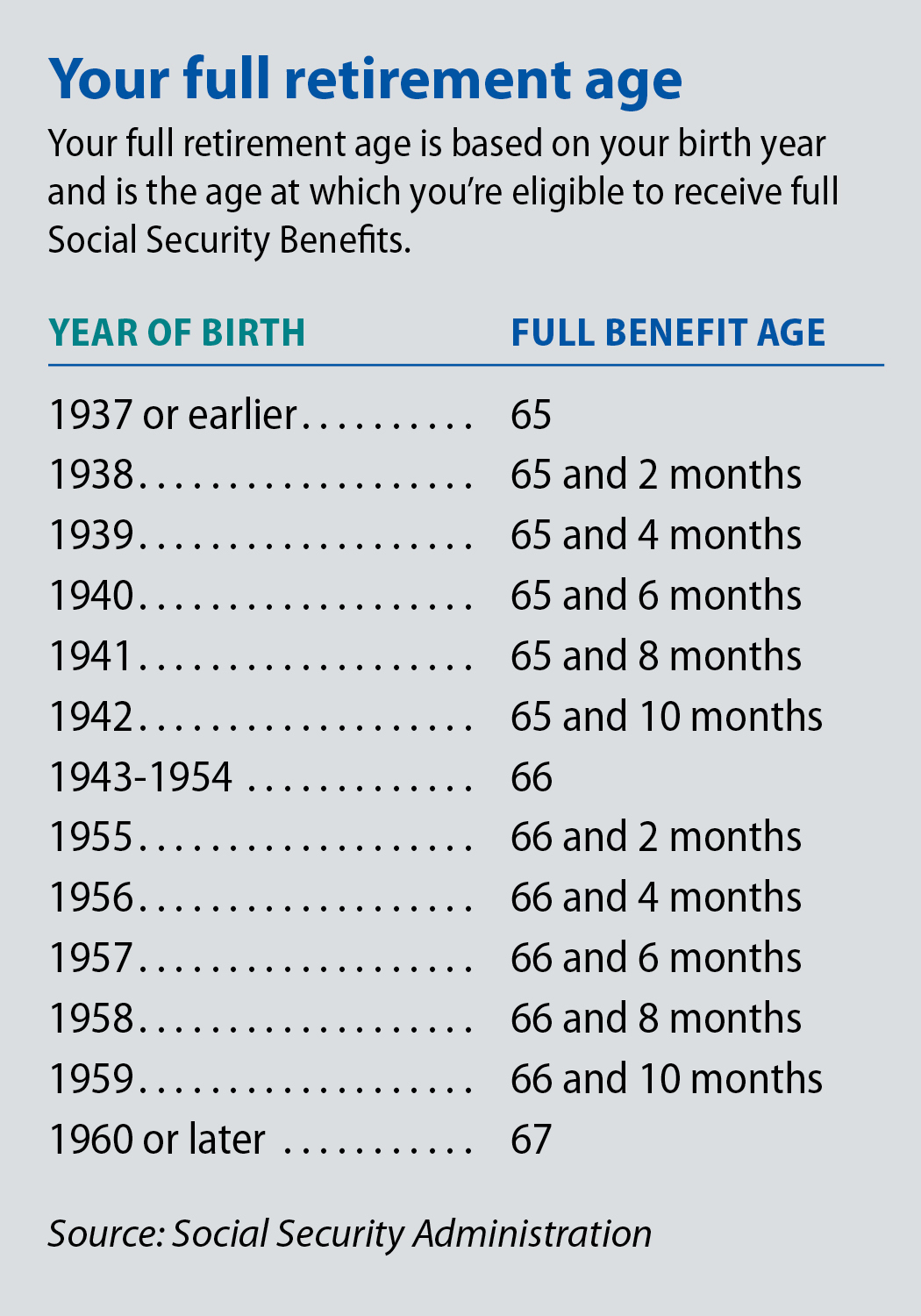

Your Full Retirement Age (FRA) is the age at which you are entitled to receive 100% of your Primary Insurance Amount (PIA). This age is determined by your birth year and has been gradually increasing over time. For those born in 1943-1954, FRA is 66. For those born in 1960 or later, it is 67. There’s a sliding scale for birth years in between.

| Year of Birth | Full Retirement Age |

|---|---|

| 1943-1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and later | 67 |

Claiming at your FRA ensures you receive the full benefit you’ve earned without any early retirement reductions. For many, this is considered the “sweet spot,” balancing immediate income with maximized individual benefits. Reaching FRA also eliminates the earnings test, meaning you can work and earn any amount without having your Social Security benefits temporarily withheld. This flexibility can be a significant advantage for those who wish to supplement their retirement income with part-time work or a new venture.

Delayed Retirement Credits (DRC): Beyond FRA

For those who can afford to wait beyond their Full Retirement Age, the Social Security Administration offers Delayed Retirement Credits (DRCs). These credits provide an incentive to postpone claiming benefits, resulting in a significantly larger monthly payment. For each year you delay claiming benefits past your FRA, up to age 70, your monthly benefit increases by a certain percentage, typically 8% per year.

This means that if your FRA is 67 and you delay claiming until age 70, your monthly benefit will be approximately 124% of your PIA (100% at FRA + 3 years * 8% per year = 24% increase). This growth is substantial and provides a powerful hedge against inflation, as your increased benefit amount will continue to receive annual cost-of-living adjustments. For individuals with good health and other sufficient retirement savings, delaying until age 70 can be one of the most effective strategies to maximize lifetime benefits, especially given rising life expectancies. The decision to delay benefits effectively “buys” a higher guaranteed income stream for life, making it a powerful component of longevity planning.

Factors Influencing Your Claiming Decision

The “right” age to collect Social Security is a highly individualized decision. It necessitates a thorough evaluation of various personal, financial, and family-related factors. A blanket recommendation seldom applies, emphasizing the importance of personalized analysis.

Personal Health and Life Expectancy

One of the most critical considerations is your personal health and projected life expectancy. If you have a family history of longevity or are in excellent health, delaying benefits to maximize your monthly payments might be a smart move, as you’re likely to collect the higher amount for a longer period. Conversely, if you face significant health challenges or have a shorter life expectancy, claiming earlier might make more sense, ensuring you receive benefits for as long as possible. Financial planners often discuss a “break-even” point—the age at which the cumulative total of your higher delayed benefits surpasses the cumulative total of your lower early benefits. This point typically falls in your late 70s or early 80s, highlighting that those who live longer truly benefit from delaying.

Spousal and Survivor Benefits

The claiming decision for married couples is significantly more complex, as it involves optimizing benefits for two individuals and considering potential survivor benefits. For example, a spouse may be eligible for up to 50% of their partner’s Full Retirement Age benefit if their own benefit is lower. Additionally, if one spouse passes away, the surviving spouse can claim the higher of their own benefit or 100% of the deceased spouse’s benefit.

Strategic claiming by the higher-earning spouse can significantly impact the surviving spouse’s future income. If the higher earner delays their benefits, their larger benefit amount will also translate into a larger survivor benefit for their spouse. While the “file and suspend” strategy was largely eliminated for new filers after April 2016, certain individuals (born before January 2, 1954) can still utilize a “restricted application” to claim spousal benefits while allowing their own benefit to grow. Understanding these intricate rules is essential for couples to maximize their combined lifetime benefits. Divorced individuals may also be eligible for benefits based on an ex-spouse’s record under certain conditions.

Other Income and Financial Needs

Your current and projected income streams play a pivotal role. If you plan to continue working full-time or part-time before your Full Retirement Age (FRA) while collecting Social Security, your benefits might be subject to the Social Security earnings test. If your earnings exceed a certain limit, a portion of your benefits will be withheld. For example, in 2024, for those below FRA, $1 in benefits will be withheld for every $2 earned above $22,320. In the year you reach FRA, the reduction is $1 for every $3 earned above a higher limit ($59,520 in 2024), and this only applies to earnings before the month you reach FRA. Once you reach FRA, the earnings test no longer applies.

Your existing retirement savings (401(k)s, IRAs, pensions), other investments, and ongoing financial obligations (mortgage, healthcare costs) also factor into the decision. If you have substantial other resources, you might be able to delay Social Security and allow it to grow. Conversely, if Social Security will be your primary source of retirement income, claiming earlier might be a necessity to cover living expenses.

Tax Implications of Social Security Benefits

It’s crucial to understand that a portion of your Social Security benefits may be taxable, depending on your “provisional income.” Provisional income includes your adjusted gross income (AGI), tax-exempt interest, and 50% of your Social Security benefits.

- If your provisional income is between $25,000 and $34,000 (single filers) or $32,000 and $44,000 (married filing jointly), up to 50% of your benefits may be taxable.

- If your provisional income exceeds $34,000 (single) or $44,000 (married filing jointly), up to 85% of your benefits may be taxable.

This means that strategically managing other retirement withdrawals (e.g., from pre-tax vs. Roth accounts) can influence the taxability of your Social Security benefits. Integrating your Social Security claiming strategy with your broader tax planning is a sophisticated but often rewarding endeavor.

Strategies for Maximizing Your Social Security Benefits

Given the complexities, a strategic approach is essential. There are several proactive steps you can take to enhance your Social Security benefits and ensure they align with your overall financial plan.

The Power of Delaying (If Feasible)

For many, the most straightforward strategy for maximizing benefits is to delay claiming until age 70. As discussed, Delayed Retirement Credits offer an 8% annual increase beyond your Full Retirement Age, creating a powerful compounding effect that can significantly boost your monthly income for life. This strategy is particularly potent for individuals who are in good health, have sufficient alternative income sources (such as other retirement savings or part-time work), or are the higher earner in a couple. Delaying provides a higher guaranteed income stream, which acts as an excellent form of longevity insurance, protecting against the risk of outliving your other savings.

Coordination with a Spouse

For married couples, coordinating claiming strategies can yield substantial long-term benefits. Rather than each spouse claiming independently, consider how one spouse’s decision impacts the other. For instance, the higher-earning spouse might delay their benefits until age 70, not only maximizing their own payment but also ensuring a larger survivor benefit for their spouse. The lower-earning spouse might claim their benefits earlier (e.g., at FRA or 62) to provide some immediate income while the higher earner’s benefits continue to grow. Another strategy for those born before January 2, 1954, is the “restricted application,” allowing them to claim spousal benefits at FRA while letting their own benefits accrue DRCs until age 70. This sophisticated coordination requires careful planning but can result in thousands of dollars more in lifetime benefits for the couple.

Reviewing Your Social Security Statement

The Social Security Administration provides an annual Social Security Statement to workers age 60 and over (or online at any age). This statement is an invaluable tool, providing a summary of your earnings history and estimated benefits at different claiming ages (62, FRA, and 70). Regularly reviewing this statement allows you to:

- Verify the accuracy of your reported earnings, as errors can reduce your future benefits.

- Understand your Primary Insurance Amount (PIA) and how it changes based on your claiming age.

- Estimate potential spousal or survivor benefits.

- Correct any discrepancies in your earnings record promptly, as these can affect your future benefit calculations.

Consulting a Financial Advisor

Given the intricate rules, the significant financial implications, and the deeply personal nature of this decision, consulting a qualified financial advisor specializing in retirement planning is highly recommended. An advisor can:

- Analyze your specific financial situation, health, and goals.

- Run various claiming scenarios and project lifetime benefits for you and your spouse.

- Integrate your Social Security strategy with your overall retirement income, investment, and tax planning.

- Help you understand complex rules, such as those pertaining to spousal, survivor, or divorced spouse benefits.

Their expertise can help you navigate the complexities and make the most informed decision, potentially adding substantial value to your retirement nest egg.

Common Misconceptions and Key Takeaways

The topic of Social Security is often surrounded by myths and misunderstandings. Dispelling these can lead to more confident and effective planning.

Myth: Social Security is “Running Out”

A prevalent concern is that Social Security will “run out” or cease to exist. While the program faces long-term funding challenges, it’s crucial to understand its structure. Social Security operates on a “pay-as-you-go” system, where current workers’ payroll taxes fund current retirees’ benefits. As such, it cannot “run out” as long as there are workers paying into the system. Projections from the Social Security Trustees indicate that while the trust funds may be able to pay only about 80% of scheduled benefits in the coming decades without congressional action, benefits will not disappear. Potential adjustments could include modest tax increases, changes to the FRA, or benefit formula modifications, but a complete collapse is highly unlikely given its status as a foundational pillar of American retirement.

Myth: You Should Always Claim at 62

While claiming at 62 offers immediate income, it comes with a permanent and significant reduction in benefits. It is a decision that should be carefully considered, not a default. The “optimal” age is unique to each individual. Factors like health, other assets, and spousal benefits can significantly alter the best strategy. For many, delaying until their Full Retirement Age or even 70 can lead to a substantially higher guaranteed income for life, offering a powerful hedge against longevity risk.

The Bottom Line: Personalization is Key

Ultimately, there is no universal “best” age to start collecting Social Security. The ideal claiming age is a deeply personal decision that requires careful consideration of your unique circumstances. It involves balancing immediate income needs with the desire for maximized long-term benefits, accounting for health, marital status, financial resources, and life goals. Proactive planning, leveraging available resources from the SSA, and seeking professional advice are essential steps toward making a choice that truly serves your retirement best interests.

By thoroughly understanding the age requirements and the myriad of factors that influence your benefits, you can confidently navigate the Social Security landscape and make an informed decision that secures a stronger financial foundation for your retirement years.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.