The anticipation of payday is a universal experience, often accompanied by the burning question: “How much will my check be?” Whether you’re a salaried employee, an hourly worker, a freelancer, or someone awaiting a government benefit, understanding the components that determine your final take-home amount is crucial for effective personal finance management. This isn’t merely about curiosity; it’s about budgeting, planning, and ensuring financial stability.

Deciphering your check, be it a traditional paper one or a direct deposit notification, can feel like navigating a complex maze of acronyms, percentages, and deductions. From mandatory taxes to voluntary contributions, numerous factors chip away at your gross earnings before the net amount lands in your account. This article will demystify the journey from gross pay to net pay, explore various types of checks you might receive, and equip you with the knowledge to accurately estimate, understand, and even optimize your future income.

Understanding Your Paycheck: The Foundation of Regular Income

For most working individuals, the regular paycheck is the cornerstone of their financial life. However, the number you see on your offer letter or hear during salary negotiations is rarely the amount that hits your bank account. This discrepancy arises from a series of essential deductions.

Gross vs. Net Pay: Decoding the Numbers

The fundamental distinction to grasp is between gross pay and net pay.

- Gross Pay is the total amount of money you earned before any deductions are taken out. For hourly workers, this is calculated by multiplying your hourly rate by the number of hours worked, plus any overtime. For salaried employees, it’s your annual salary divided by the number of pay periods in a year. Gross pay can also include bonuses, commissions, and other forms of compensation.

- Net Pay (often referred to as take-home pay) is the amount you actually receive after all deductions have been subtracted from your gross pay. This is the figure that truly impacts your budget and spending power.

The journey from gross to net is where the complexities often begin, encompassing a range of mandatory and voluntary deductions that are critical to understand.

Mandatory Deductions: Taxes, Social Security, and Medicare

These are the non-negotiable subtractions from your paycheck, legally required by federal, state, and sometimes local governments. They fund essential public services and social safety nets.

- Federal Income Tax: This is perhaps the largest deduction for many. The amount withheld depends on your income level, filing status, and the information you provide on your W-4 form (Employee’s Withholding Certificate). The U.S. has a progressive tax system, meaning higher earners pay a larger percentage of their income in taxes.

- State Income Tax: Most states also levy an income tax, though some, like Florida, Texas, and Washington, do not. Similar to federal taxes, the amount depends on your income and state-specific tax laws.

- Local Income Tax: Some cities or localities may also impose their own income taxes, adding another layer of deduction.

- Social Security Tax (FICA – Old-Age, Survivors, and Disability Insurance): This tax funds benefits for retirees, survivors, and disabled individuals. As of current laws, employees typically pay 6.2% of their gross wages up to a certain annual limit. Employers match this contribution.

- Medicare Tax (FICA – Hospital Insurance): This tax funds health insurance for individuals aged 65 or older and certain younger people with disabilities. Employees typically pay 1.45% of all their gross wages, with no income limit. High-income earners may also pay an additional Medicare tax.

Understanding these mandatory deductions is crucial because they represent a significant portion of your earnings that you will never see in your bank account, yet they are vital contributions to society.

Voluntary Deductions: Benefits, Retirement, and More

Beyond the mandatory deductions, many individuals opt for a range of voluntary deductions that contribute to their financial well-being and future security. While these reduce your net pay, they often provide significant benefits.

- Health Insurance Premiums: If you receive health, dental, or vision insurance through your employer, your share of the premium is typically deducted from your paycheck.

- Retirement Contributions (e.g., 401(k), 403(b)): Many employers offer retirement plans where you can contribute a portion of your gross income, often pre-tax, which reduces your taxable income in the current year. Employer matching contributions are a valuable benefit to take advantage of.

- Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs): These accounts allow you to set aside pre-tax money for qualified medical expenses, further reducing your taxable income.

- Life Insurance Premiums: If you purchase supplemental life insurance through your employer, the premiums will be deducted.

- Disability Insurance Premiums: Similar to life insurance, short-term and long-term disability premiums can be deducted.

- Union Dues: If you are a member of a labor union, your membership dues will often be automatically deducted.

- Loan Repayments: In some cases, employers might facilitate deductions for company loans or other specific financial arrangements.

While these deductions reduce your current take-home pay, they are often strategic investments in your health, retirement, and overall financial future.

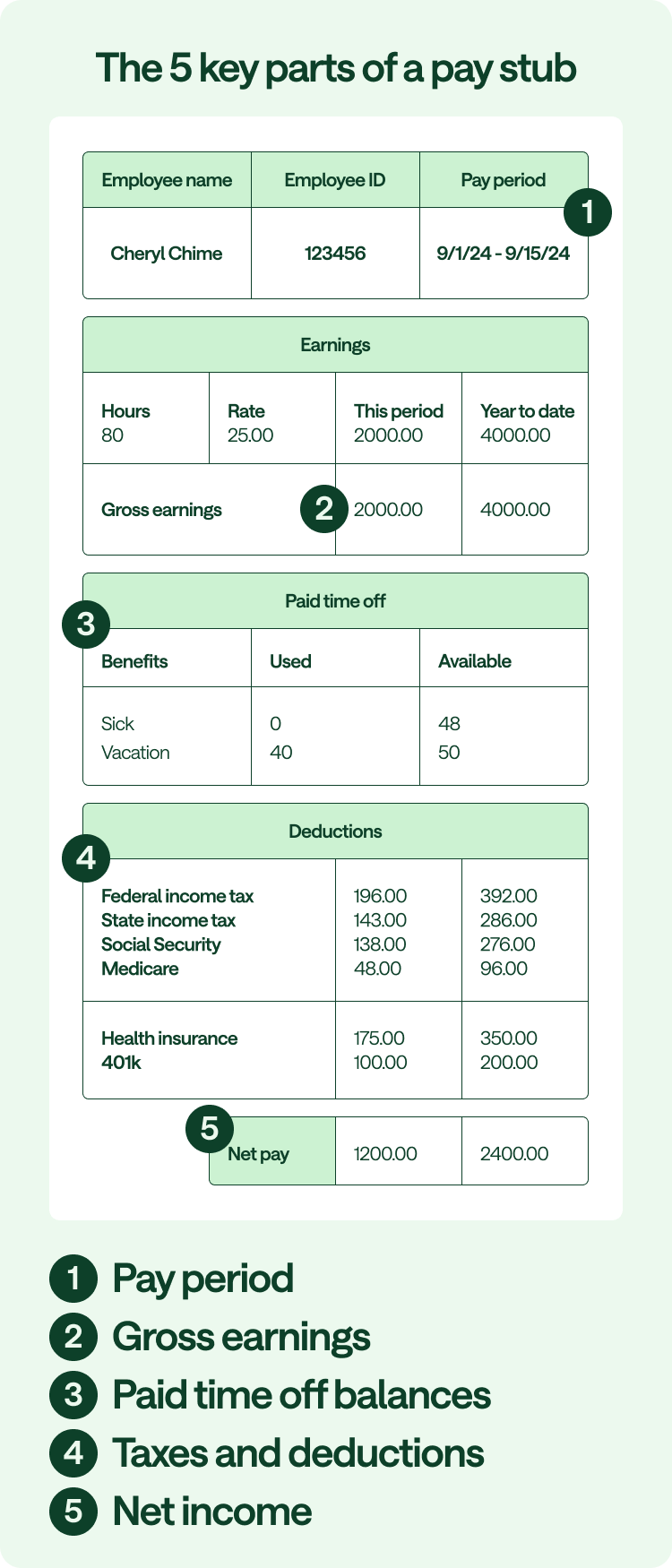

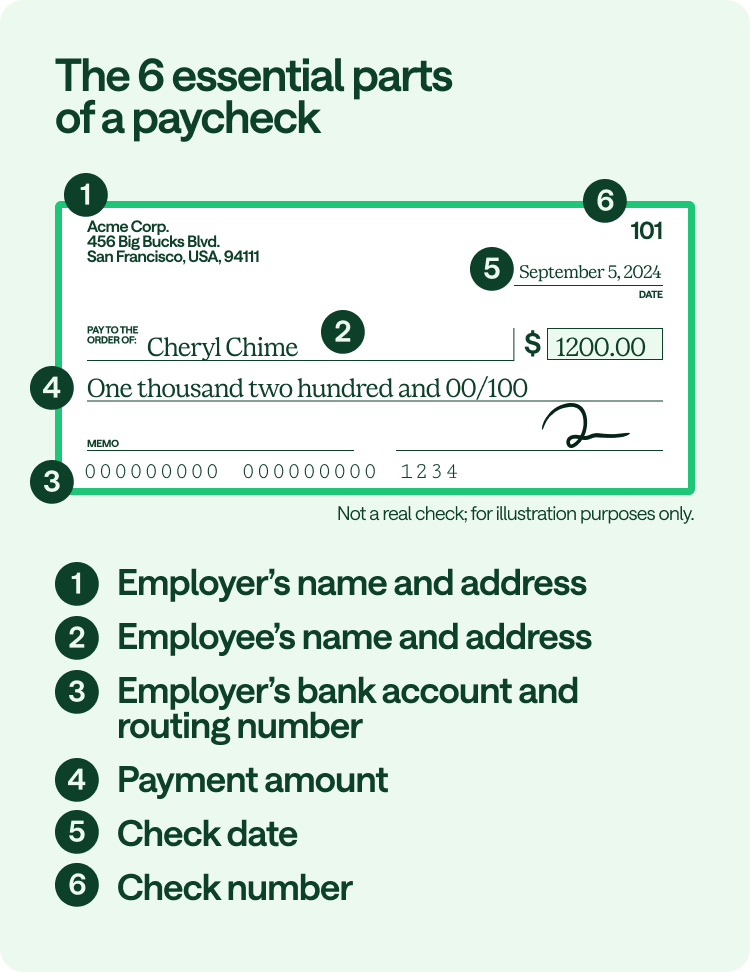

Navigating Pay Stubs and Online Portals

Your pay stub (or online pay portal) is the definitive record of how your gross pay transforms into net pay. It itemizes all earnings and deductions. It’s essential to review it regularly to ensure accuracy. Key elements to look for include:

- Your name, address, and employee ID.

- Pay period dates.

- Gross wages for the current period and year-to-date.

- Detailed breakdown of all federal, state, and local taxes withheld.

- Itemized list of all voluntary deductions (e.g., 401(k), health insurance).

- Your net pay for the current period and year-to-date.

- Accrued vacation, sick leave, or paid time off (PTO) balances.

Regularly checking your pay stub helps you catch errors, understand changes in your deductions, and verify that your tax withholdings align with your financial goals.

Beyond the Regular Paycheck: Other Forms of Income

While regular employment paychecks are common, the question “How much will my check be?” can apply to many other forms of financial remuneration, each with its own set of considerations.

Contractor Payments and Freelance Income

For independent contractors, freelancers, or self-employed individuals, the concept of a “check” is very different. Clients typically pay the gross agreed-upon amount, and there are no employer-initiated tax withholdings. This means:

- Self-Employment Tax: Freelancers are responsible for both the employee and employer portions of Social Security and Medicare taxes (12.4% for Social Security up to the annual limit, and 2.9% for Medicare on all income).

- Estimated Taxes: Since taxes aren’t withheld, freelancers must typically make quarterly estimated tax payments to the IRS and state tax agencies to avoid penalties.

- Deductible Business Expenses: A significant benefit for freelancers is the ability to deduct legitimate business expenses (home office, supplies, software, travel, etc.), which reduces their taxable income.

- 1099 Forms: Clients typically issue Form 1099-NEC (Nonemployee Compensation) if they pay you over a certain threshold, documenting your gross earnings.

Understanding these distinctions is vital for managing cash flow and avoiding a hefty tax bill at year-end.

Government Benefits: Unemployment, Disability, and Social Security

Individuals receiving government benefits also wonder about their check amounts. These can include:

- Unemployment Benefits: These payments are often a percentage of your previous earnings, up to a state-defined maximum. They are typically taxable at the federal level and sometimes at the state level.

- Social Security Benefits: Payments for retirement, disability, or survivor benefits are calculated based on your earnings history. A portion of these benefits may be taxable depending on your “combined income” (adjusted gross income + non-taxable interest + one-half of your Social Security benefits).

- Disability Insurance: Whether private or state-funded, these checks provide income replacement. Taxability depends on who paid the premiums (if the employer paid, it’s usually taxable; if you paid with after-tax money, it’s often tax-free).

The rules for each benefit type are complex and specific, requiring careful review of official communications to determine net amounts.

Investment Distributions and Dividends

If you’re an investor, your “check” might come in the form of investment distributions or dividends.

- Dividends: Payments made by companies to their shareholders. These can be “qualified” (taxed at lower capital gains rates) or “ordinary” (taxed at ordinary income rates).

- Capital Gains: Profits from selling investments (stocks, real estate, etc.) for more than you paid for them. These are categorized as short-term (held for one year or less, taxed at ordinary income rates) or long-term (held for more than one year, taxed at preferential capital gains rates).

- Interest Income: Money earned from savings accounts, bonds, or CDs. This is typically taxed at ordinary income rates.

While not a “check” in the traditional sense, these income streams directly impact your overall financial picture and require careful tax planning.

Refunds and Reimbursements

Sometimes, your “check” comes as a reimbursement or a refund.

- Tax Refunds: If you overpaid your estimated or withheld taxes throughout the year, the government issues a refund. This is not income; it’s the return of your own money.

- Expense Reimbursements: If you incur business expenses out-of-pocket, your employer might reimburse you. These are generally not taxable income as long as they are legitimate business expenses and you provide adequate substantiation.

While these payments boost your current cash flow, it’s important to understand their tax implications and distinguish them from earned income.

Factors Influencing Your Check’s Size

Beyond the basic categories of earnings and deductions, several dynamic factors can significantly impact the final amount of your check.

Employment Status: Full-time, Part-time, Hourly, Salary

The nature of your employment directly shapes how your gross pay is calculated.

- Hourly Workers: Their check amount fluctuates based on the exact number of hours worked, including any overtime (typically 1.5 times the regular rate for hours over 40 in a workweek).

- Salaried Employees: Receive a fixed amount per pay period, regardless of hours worked (as long as they meet job requirements). Their checks are generally more predictable, barring changes in benefits or tax elections.

- Part-time Workers: Similar to hourly, but often with fewer hours and potentially different eligibility for benefits.

Understanding your employment status helps predict the consistency and variability of your checks.

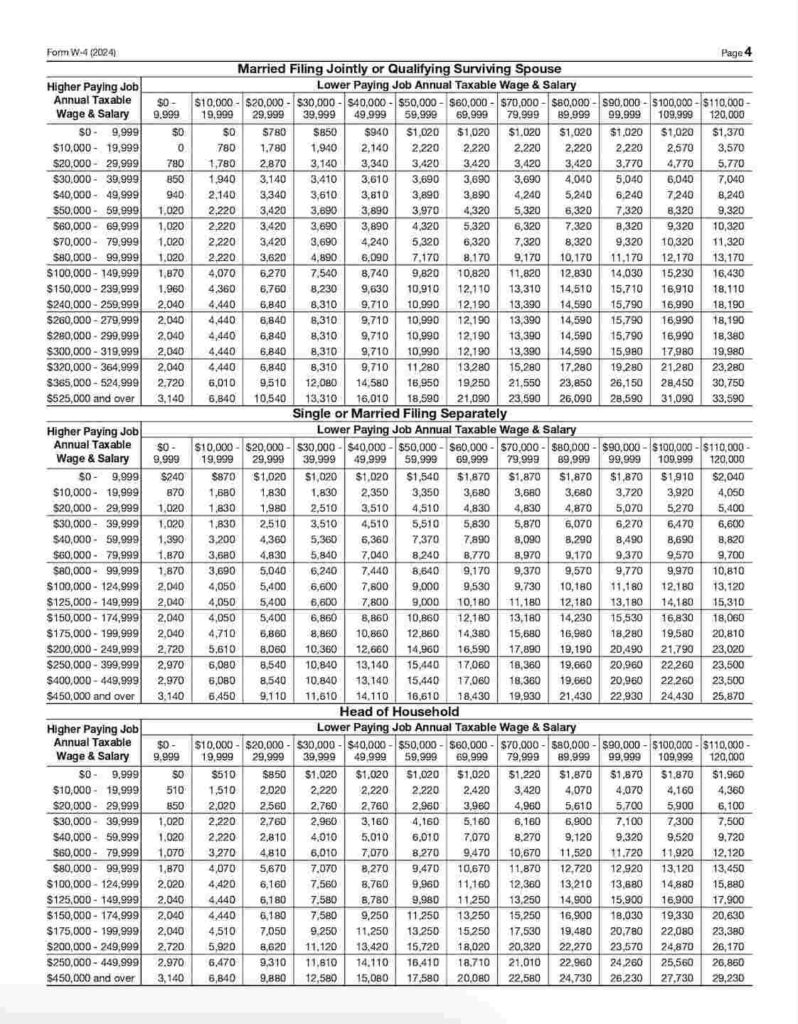

Tax Withholding Strategies

Your choices on Form W-4 (or equivalent state forms) directly influence how much federal (and state) income tax is withheld from each paycheck.

- Claiming “Exemptions” or “Dependents”: In the past, this was a direct factor. Now, the W-4 uses dollar amounts for deductions and credits. The more allowances or credits you claim, the less tax is withheld, resulting in a larger net pay, but potentially a smaller refund or even taxes owed at year-end.

- Additional Withholding: You can elect to have an additional flat dollar amount withheld from each check. This can be useful for those with complex tax situations, side income, or who simply prefer a larger refund.

- Tax Planning: Aligning your W-4 with your anticipated annual income, deductions, and credits is a key component of effective tax planning. The goal is often to have just enough withheld to cover your tax liability without giving the government an interest-free loan (a large refund).

Periodically reviewing and adjusting your W-4 is a smart financial practice, especially after life events like marriage, divorce, having children, or changing jobs.

Benefits Enrollment and Contributions

The decisions you make during your employer’s open enrollment period have a direct and lasting impact on your net pay.

- Tier of Health Insurance: Choosing a PPO over an HMO, or individual coverage over family coverage, will result in different premium deductions.

- Retirement Contribution Percentage: Increasing your 401(k) contribution from 5% to 10% will reduce your net pay but boost your retirement savings and potentially lower your taxable income.

- Other Voluntary Benefits: Opting for commuter benefits, pet insurance, or legal services through payroll deductions will also reduce your take-home pay.

These choices are personal and should align with your health needs, financial goals, and risk tolerance.

Performance-Based Compensation: Bonuses and Commissions

For many in sales or performance-driven roles, bonuses and commissions can significantly impact their overall earnings, but they are often subject to specific withholding rules.

- Bonuses: These one-time payments are often subject to “supplemental wage” tax rules, which can result in a higher initial withholding rate (e.g., a flat 22% federal withholding, though the actual tax rate depends on your overall income).

- Commissions: Paid based on sales or performance, commissions may be treated similarly to regular wages or supplemental wages, depending on how they’re structured and paid.

While these can be substantial additions, it’s important to remember that they are fully taxable and typically subject to significant withholding.

Tools and Strategies for Estimating and Maximizing Your Income

Proactively understanding and influencing your check’s amount is a critical skill for financial empowerment.

Utilizing Online Paycheck Calculators

Many reputable websites offer free paycheck calculators (e.g., ADP, PaycheckCity, IRS Tax Withholding Estimator). These tools allow you to input your gross pay, pay frequency, filing status, dependents, and other deductions to get a close estimate of your net pay.

- Accuracy: While useful, remember these are estimates. They may not account for every unique deduction or local tax.

- Scenario Planning: Use them to run “what if” scenarios, such as how an increase in your 401(k) contribution or a change in your W-4 would impact your take-home pay.

Reviewing Your Tax Withholding (Form W-4) Annually

As mentioned, your W-4 is a powerful tool.

- Life Changes: Revisit your W-4 after major life events (marriage, divorce, birth of a child, purchasing a home, significant income change).

- IRS Estimator: The IRS Tax Withholding Estimator tool is highly recommended. It guides you through a series of questions about your income, deductions, and credits to recommend the most accurate W-4 settings for your situation.

- Avoid Surprises: Adjusting your W-4 helps ensure you neither overpay (giving the government an interest-free loan) nor underpay (facing a tax bill or penalties).

Budgeting and Financial Planning

Understanding your check’s amount is fundamental to creating and sticking to a budget.

- Know Your Net Income: Your budget should always be based on your net (take-home) pay, not your gross.

- Track Expenses: Once you know your net income, you can allocate funds for necessities (housing, food, transportation), debt repayment, savings, and discretionary spending.

- Goal Setting: Your check is a means to an end. Financial planning involves aligning your income with your short-term and long-term goals (e.g., buying a home, retirement, education, travel).

Exploring Opportunities for Increased Earnings

If your current check isn’t meeting your financial needs or goals, consider ways to increase your income.

- Negotiate Salary/Raises: Regularly assess your market value and be prepared to negotiate your salary or ask for raises based on performance and contributions.

- Skill Development: Acquire new skills or certifications that can lead to promotions or higher-paying roles.

- Side Hustles: Explore opportunities for online income, freelance work, or part-time gigs to supplement your main income.

- Investment Income: As discussed, strategically investing can generate additional income streams over time.

What to Do If Your Check is Incorrect or Delayed

Discovering an incorrect or delayed check can be frustrating and disruptive to your financial planning. Knowing the proper steps to take is crucial.

Reviewing Your Pay Stub Thoroughly

Before contacting anyone, meticulously examine your pay stub.

- Compare to Prior Stubs: Look for discrepancies in hours worked, hourly rate, gross pay, and specific deductions.

- Check Deductions: Verify that all expected deductions are present and correct, and no unexpected ones have appeared.

- Ensure Proper Pay Period: Confirm the pay period covered by the check matches your expectations.

Often, a quick review can reveal a simple explanation, such as an incorrect time entry, a new benefit enrollment deduction, or a one-time adjustment.

Contacting HR or Payroll

If you identify an error or a delay, the first point of contact should be your company’s Human Resources (HR) or Payroll department.

- Be Prepared: Have your pay stub, any relevant documentation (e.g., time sheets, offer letter, benefit enrollment forms), and a clear explanation of the issue ready.

- Document Everything: Keep a record of who you spoke with, the date and time, and the agreed-upon next steps. Follow up in writing (email) to create a paper trail.

- Understand Resolution Timelines: Inquire about the expected timeline for resolving the issue and issuing any necessary adjustments or corrected payments.

Most companies have established procedures for handling pay discrepancies and are motivated to resolve them promptly.

Understanding Your Rights and Recourse

If issues persist or are not resolved satisfactorily, understand your legal rights.

- Fair Labor Standards Act (FLSA): The FLSA governs minimum wage, overtime pay, recordkeeping, and child labor standards for most private and public employment. It ensures employees are paid for all hours worked.

- State Labor Laws: Many states have their own labor laws that may offer additional protections regarding timely payment of wages, final paychecks, and handling of deductions.

- Department of Labor: If your employer fails to address a significant pay discrepancy, you can file a complaint with the U.S. Department of Labor (or your state’s Department of Labor). They can investigate wage violations and help recover unpaid wages.

While these steps are a last resort, knowing your rights provides peace of mind and protection against potential wage theft or persistent errors.

Understanding “how much will my check be” is far more than just anticipating a deposit; it’s a fundamental aspect of financial literacy. By meticulously understanding gross versus net pay, mandatory and voluntary deductions, and the various factors influencing your income, you gain control over your financial destiny. Whether you’re decoding a traditional pay stub, managing freelance income, or navigating government benefits, proactive engagement with your financial details is the key to effective budgeting, strategic planning, and ultimately, achieving your financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.