For millions of Americans, Social Security benefits represent a crucial component of their retirement income, providing a financial bedrock in their golden years. However, a common misconception is that these benefits are entirely tax-free. The reality is more nuanced: depending on your total income in retirement, a portion of your Social Security benefits may be subject to federal income tax, and in some cases, state income tax. Understanding these rules is essential for effective financial planning and to avoid unwelcome surprises come tax season.

This guide will demystify the taxation of Social Security benefits, walking you through the federal rules, the calculation of taxable amounts, and strategies to manage your tax liability. By gaining clarity on “how much tax on Social Security,” you can better prepare for a financially secure retirement.

The Foundations of Social Security Benefit Taxation

The taxation of Social Security benefits isn’t a straightforward percentage applied to all recipients. Instead, it’s determined by a concept known as “provisional income,” a specific calculation used by the IRS to ascertain if and how much of your benefits are taxable. This system was introduced in 1983 and expanded in 1993, reflecting an ongoing effort to ensure the long-term solvency of the Social Security program while maintaining fairness.

Understanding Your Provisional Income

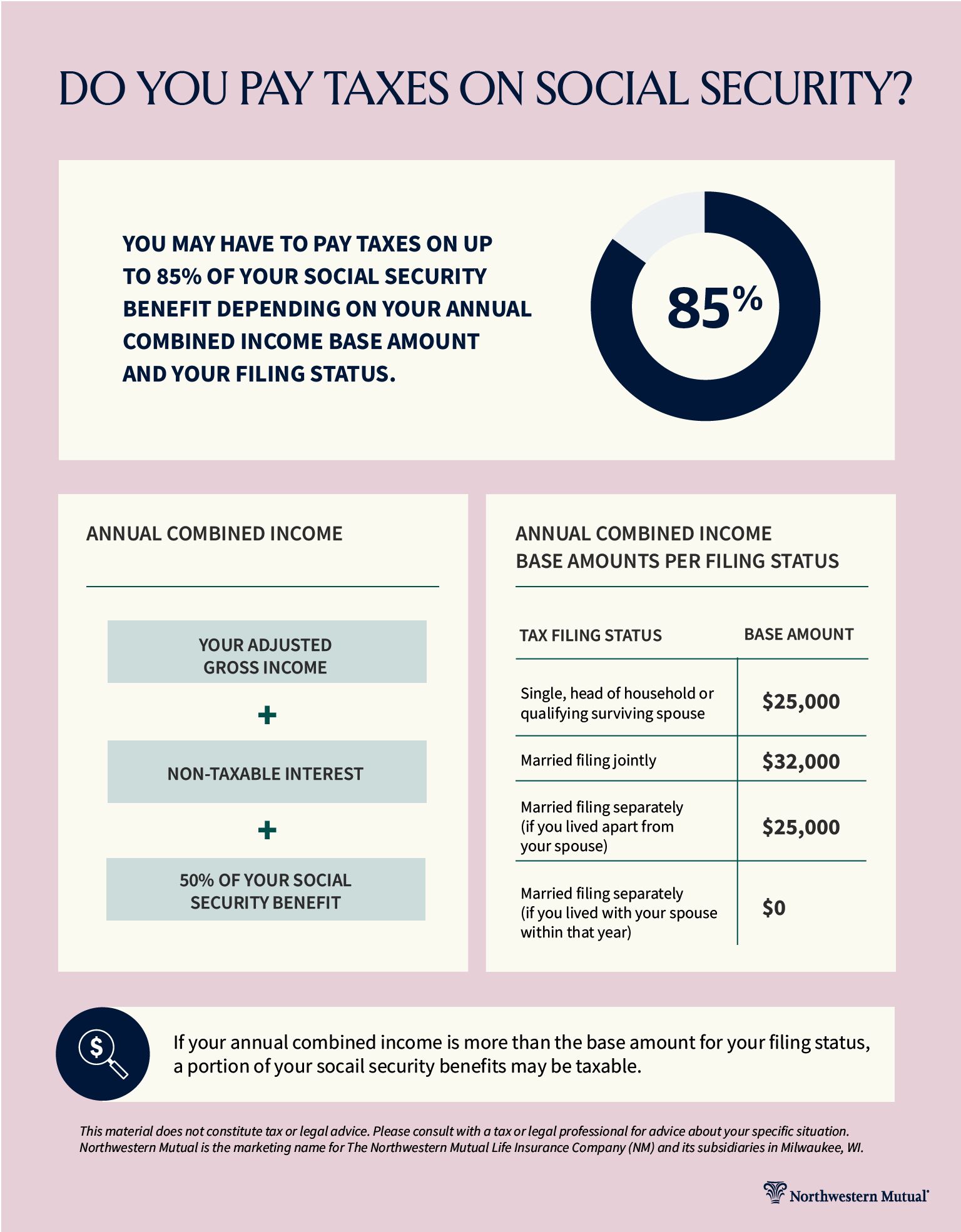

The cornerstone of determining your Social Security tax liability is your provisional income. This figure is not your adjusted gross income (AGI) as you might typically think of it, but a modified version calculated specifically for Social Security taxation purposes. Your provisional income is the sum of:

- Your Adjusted Gross Income (AGI) from your federal tax return (excluding Social Security benefits).

- Any tax-exempt interest (e.g., interest from municipal bonds).

- One-half (50%) of your Social Security benefits for the year.

This combined figure dictates whether you will pay taxes on 0%, 50%, or 85% of your Social Security benefits. It’s crucial to understand that even if you have a modest Social Security benefit, other sources of income, such as pensions, IRA distributions, or wages, can push your provisional income above the thresholds, making a portion of your benefits taxable.

The Income Thresholds for Taxation

Once your provisional income is calculated, it’s compared against specific income thresholds set by the IRS. These thresholds vary based on your tax filing status. There are two tiers of taxation:

- Up to 50% Taxable: If your provisional income exceeds the first threshold, up to 50% of your Social Security benefits may be subject to federal income tax.

- Up to 85% Taxable: If your provisional income exceeds the second and higher threshold, up to 85% of your Social Security benefits may be subject to federal income tax.

It’s important to note that these thresholds are not indexed for inflation, meaning they remain static even as average incomes and the cost of living rise. This fixed nature can lead to more retirees facing taxation on their benefits over time.

How Provisional Income Dictates Your Tax Liability

The precise amount of your Social Security benefits that are taxable depends entirely on which provisional income tier your income falls into. The rules are slightly different for single filers versus those who are married and filing jointly.

Single Filers’ Provisional Income Tiers

For individuals filing as single, head of household, or qualifying widow(er), the thresholds are:

- Provisional Income Between $25,000 and $34,000: If your provisional income falls within this range, you may have to pay income tax on up to 50% of your Social Security benefits. The amount taxed is the lesser of:

- 50% of your Social Security benefits, or

- 50% of the amount by which your provisional income exceeds $25,000.

- Provisional Income Exceeding $34,000: If your provisional income is above $34,000, you may have to pay income tax on up to 85% of your Social Security benefits. The amount taxed is the lesser of:

- 85% of your Social Security benefits, or

- The sum of (a) 85% of the amount by which your provisional income exceeds $34,000, PLUS $4,500 (which is 50% of the $9,000 range between $25,000 and $34,000).

If your provisional income is below $25,000, none of your Social Security benefits are taxable.

Married Filing Jointly Provisional Income Tiers

For married couples filing jointly, the thresholds are more generous:

- Provisional Income Between $32,000 and $44,000: If your provisional income falls within this range, you may have to pay income tax on up to 50% of your Social Security benefits. The amount taxed is the lesser of:

- 50% of your Social Security benefits, or

- 50% of the amount by which your provisional income exceeds $32,000.

- Provisional Income Exceeding $44,000: If your provisional income is above $44,000, you may have to pay income tax on up to 85% of your Social Security benefits. The amount taxed is the lesser of:

- 85% of your Social Security benefits, or

- The sum of (a) 85% of the amount by which your provisional income exceeds $44,000, PLUS $6,000 (which is 50% of the $12,000 range between $32,000 and $44,000).

If your provisional income is below $32,000, none of your Social Security benefits are taxable.

What About Married Filing Separately?

For married couples filing separately, the rules are typically less favorable. If you lived with your spouse at any time during the tax year and file separately, up to 85% of your Social Security benefits are generally taxable, regardless of your income. This is a significant penalty designed to discourage couples from filing separately solely to reduce their Social Security tax liability. If you lived apart from your spouse for the entire tax year, you would follow the same rules as a single filer.

Strategies to Minimize Social Security Benefit Taxation

Understanding the rules is the first step; the next is to proactively manage your income to potentially reduce the amount of Social Security benefits subject to tax. Strategic financial planning can make a significant difference in your retirement tax burden.

Managing Your Provisional Income

Since provisional income is the key determinant, strategies should focus on keeping this figure below the thresholds if possible, or at least minimizing the amount by which it exceeds them.

- Qualified Charitable Distributions (QCDs): If you are 70½ or older and have a traditional IRA, you can make a QCD directly from your IRA to a qualified charity. These distributions count towards your required minimum distributions (RMDs) but are excluded from your AGI, thereby reducing your provisional income.

- Tax-Loss Harvesting: Selling investments at a loss to offset capital gains and up to $3,000 of ordinary income can lower your AGI, which in turn reduces your provisional income.

- Roth Conversions (with caution): Converting funds from a traditional IRA to a Roth IRA generates taxable income in the year of conversion. While this increases your provisional income in the short term, future qualified withdrawals from the Roth IRA are tax-free and do not count towards provisional income. This strategy is best implemented before you start receiving Social Security benefits or during years when your other income is unusually low.

- Delaying Distributions from Traditional IRAs/401(k)s: If you don’t need the income, delaying withdrawals from tax-deferred accounts can keep your AGI lower, especially before RMDs kick in at age 73.

The Role of Retirement Account Withdrawals

The type of retirement account you withdraw from significantly impacts your provisional income:

- Traditional IRAs and 401(k)s: Withdrawals from these accounts are generally taxed as ordinary income and are fully included in your AGI, directly increasing your provisional income and potentially making more of your Social Security benefits taxable.

- Roth IRAs and Roth 401(k)s: Qualified withdrawals from Roth accounts are tax-free and do not count towards your AGI. This makes them a powerful tool for managing provisional income in retirement, as they provide income without increasing your Social Security tax liability.

- Taxable Brokerage Accounts: Income from these accounts (dividends, interest, capital gains) generally counts towards AGI, but the principal withdrawals do not.

Tax-Efficient Investment Choices

Consider including tax-efficient investments in your portfolio, especially if you anticipate having high provisional income in retirement.

- Municipal Bonds: Interest earned on municipal bonds is typically exempt from federal income tax and, often, from state and local taxes if you live in the issuing state. This tax-exempt interest is still factored into your provisional income calculation (50% of total Social Security benefits + AGI + all tax-exempt interest), but it doesn’t contribute to your AGI directly, which can be advantageous compared to taxable bond interest.

- Dividend Stocks: Qualified dividends are taxed at lower capital gains rates, which can be more tax-efficient than ordinary income.

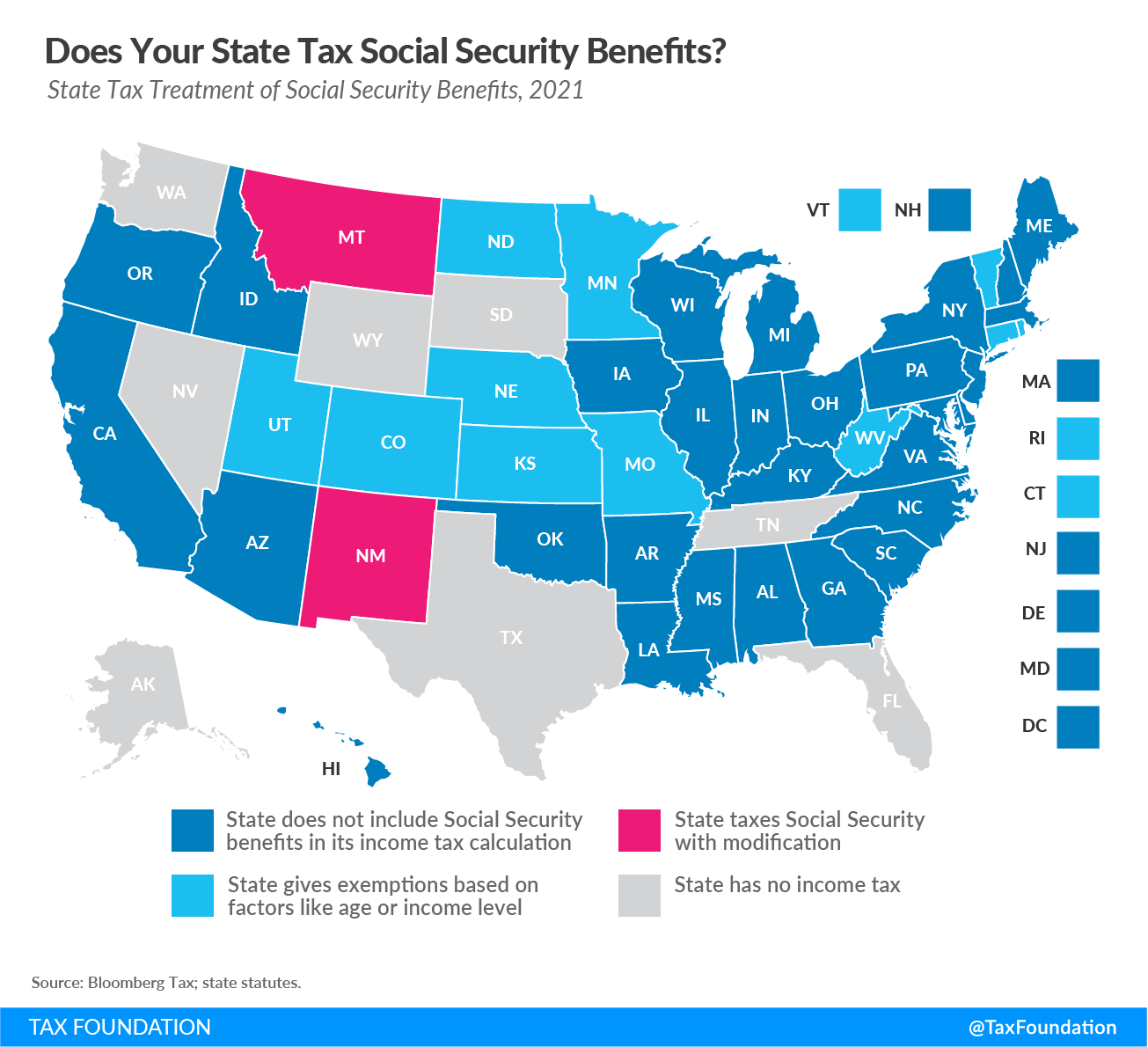

State-Level Taxation of Social Security Benefits

Beyond federal taxes, a handful of states also tax Social Security benefits. While the vast majority of states (over 35) do not tax these benefits, it’s crucial to be aware of the specific rules in your state of residence, especially if you live in one of the states that do.

The Majority of States Don’t Tax Benefits

For most retirees, state income tax on Social Security benefits is not a concern. States like Florida, Texas, Nevada, and Washington, for example, have no state income tax at all, naturally meaning they don’t tax Social Security. Many other states that do have an income tax choose to exempt Social Security benefits entirely. This list includes popular retirement destinations and many other states across the country.

States That Do Tax Benefits (or Have Unique Rules)

A limited number of states tax Social Security benefits, though they often provide their own specific exemptions or thresholds that differ from federal rules. These states typically have their own calculation methods, which might include different income limits, exemptions based on age, or other factors. For instance, some states might use AGI, while others might have a separate calculation similar to the federal provisional income. It is imperative to check your state’s current tax laws or consult a local tax professional if you reside in or plan to move to a state that taxes Social Security benefits. The rules can change, and what applies federally may not apply at the state level.

Reporting and Withholding Social Security Taxes

The process of reporting and potentially paying taxes on your Social Security benefits is relatively straightforward once you understand the underlying principles. The Social Security Administration (SSA) provides the necessary documentation, and you have options for how to manage your tax payments throughout the year.

Form SSA-1099: Your Key Document

Each year, the Social Security Administration sends out Form SSA-1099, “Social Security Benefit Statement.” This crucial document details the total amount of benefits you received during the previous year. You will need this form when preparing your federal income tax return (and potentially your state return) to accurately calculate your taxable Social Security benefits. Box 5 of this form shows your net benefits for the year, which is the figure you’ll use in your provisional income calculation.

Electing Voluntary Withholding

To avoid a large tax bill at the end of the year, many retirees choose to have federal income tax withheld directly from their monthly Social Security benefits. You can arrange this by submitting Form W-4V, “Voluntary Withholding Request,” to the Social Security Administration. You can choose to have 7%, 10%, 12%, or 22% of your monthly benefit withheld. This can be an effective “pay-as-you-go” method, similar to how taxes are withheld from wages, helping to prevent underpayment penalties.

Estimated Tax Payments

If you prefer not to have taxes withheld from your Social Security benefits, or if your other income sources (like pensions, IRA distributions, or self-employment income) mean that withholding from Social Security alone isn’t enough, you may need to make quarterly estimated tax payments. These payments cover not only potential taxes on your Social Security benefits but also taxes on other non-wage income. The IRS Form 1040-ES, “Estimated Tax for Individuals,” provides guidance on how to calculate and pay these amounts throughout the year.

Conclusion

The question of “how much tax on Social Security” is one that every retiree, or near-retiree, should understand. It’s clear that Social Security benefits are not universally tax-free, and the amount subject to taxation hinges on your overall provisional income. By carefully calculating your provisional income against federal thresholds and being mindful of your state’s specific rules, you can gain a clear picture of your tax liability.

Proactive planning, including strategic use of retirement accounts, managing withdrawals, and considering tax-efficient investments, can significantly impact the amount of tax you pay on your benefits. Whether it’s electing voluntary withholding or making estimated payments, there are practical steps you can take to manage your tax obligations throughout retirement. Given the complexities involved, especially when coordinating various income sources and state laws, consulting a qualified financial advisor or tax professional is highly recommended to ensure your retirement plan is optimized for tax efficiency and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.