For decades, the gold standard of passive investing has been the Exchange-Traded Fund (ETF) and the mutual fund. These “pooled” vehicles allowed investors to buy a single share that represented a basket of hundreds, or even thousands, of companies. However, as financial technology evolves, a more sophisticated approach—once reserved for the ultra-wealthy—has moved into the mainstream. This strategy is known as direct indexing.

Direct indexing is the process of purchasing the individual constituent stocks of an index directly in a brokerage account, rather than buying a fund that tracks that index. While it sounds simple, the implications for tax efficiency, personalization, and risk management are profound. In an era where “one-size-fits-all” no longer satisfies the modern investor, direct indexing offers a path toward a more granular, optimized portfolio.

Understanding the Mechanics of Direct Indexing

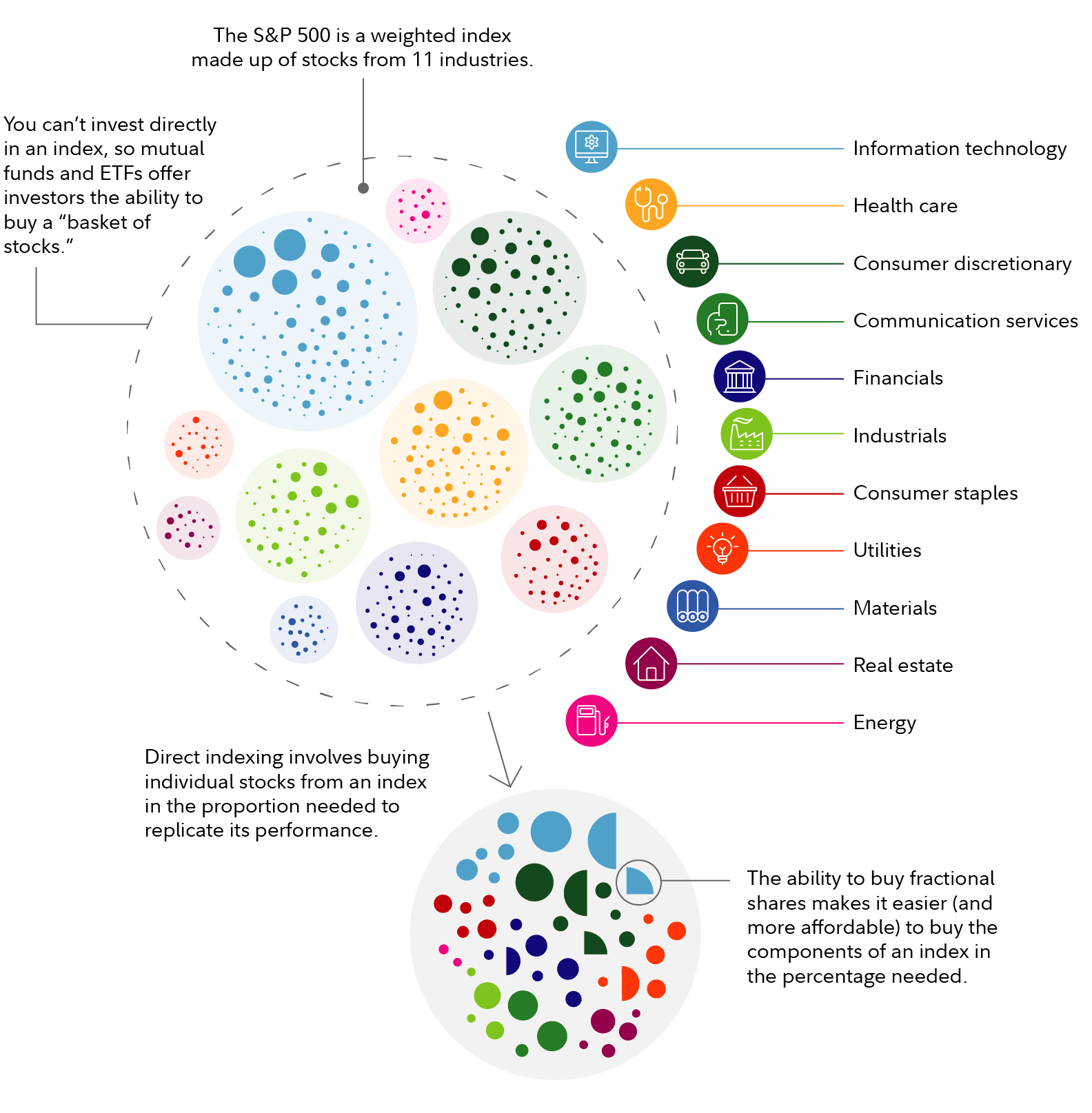

To understand direct indexing, one must first look at how traditional index funds work. When you buy an S&P 500 ETF, you own a single ticker symbol. The fund manager handles the buying and selling of the 500 underlying companies. You receive the average return of those 500 companies, minus a small management fee.

In contrast, with direct indexing, you don’t own the fund; you own the 500 individual stocks themselves. If Apple, Microsoft, and Amazon are in the index, they appear as individual line items in your brokerage account.

How Direct Indexing Differs from ETFs and Mutual Funds

The primary difference lies in ownership and control. In an ETF, the “wrapper” prevents you from interacting with the underlying securities. If the S&P 500 is up 10%, but 100 of the companies within that index are actually down for the year, you cannot realize the losses of those 100 companies to offset your taxes because you only own the “wrapper.”

Direct indexing removes that wrapper. By owning the individual securities, you gain the ability to sell specific “losers” while keeping the “winners,” a level of control that is mathematically impossible within a pooled fund. This transition from “buying a product” to “owning a strategy” represents a paradigm shift in wealth management.

The Role of Fractional Shares and Automation

In the past, direct indexing was impractical for the average investor. To replicate the S&P 500, you would need enough capital to buy at least one full share of every company, some of which trade for hundreds or thousands of dollars. Furthermore, the commissions on 500 separate trades would have been astronomical.

Two major shifts in the financial industry changed this: zero-commission trading and fractional shares. Today, sophisticated algorithms can buy 1/100th of a share of an expensive stock, allowing an investor with a $100,000 portfolio—or even less—to perfectly mimic a massive index. Automation handles the rebalancing, ensuring the portfolio stays aligned with the target index without the investor having to manually place hundreds of trades.

The Strategic Advantages: Why Investors are Shifting Away from Pooled Vehicles

The surge in popularity of direct indexing is not merely a trend; it is driven by tangible financial advantages that can lead to higher after-tax returns. For high-earning investors or those with complex financial lives, the benefits of direct indexing often outweigh the simplicity of a standard ETF.

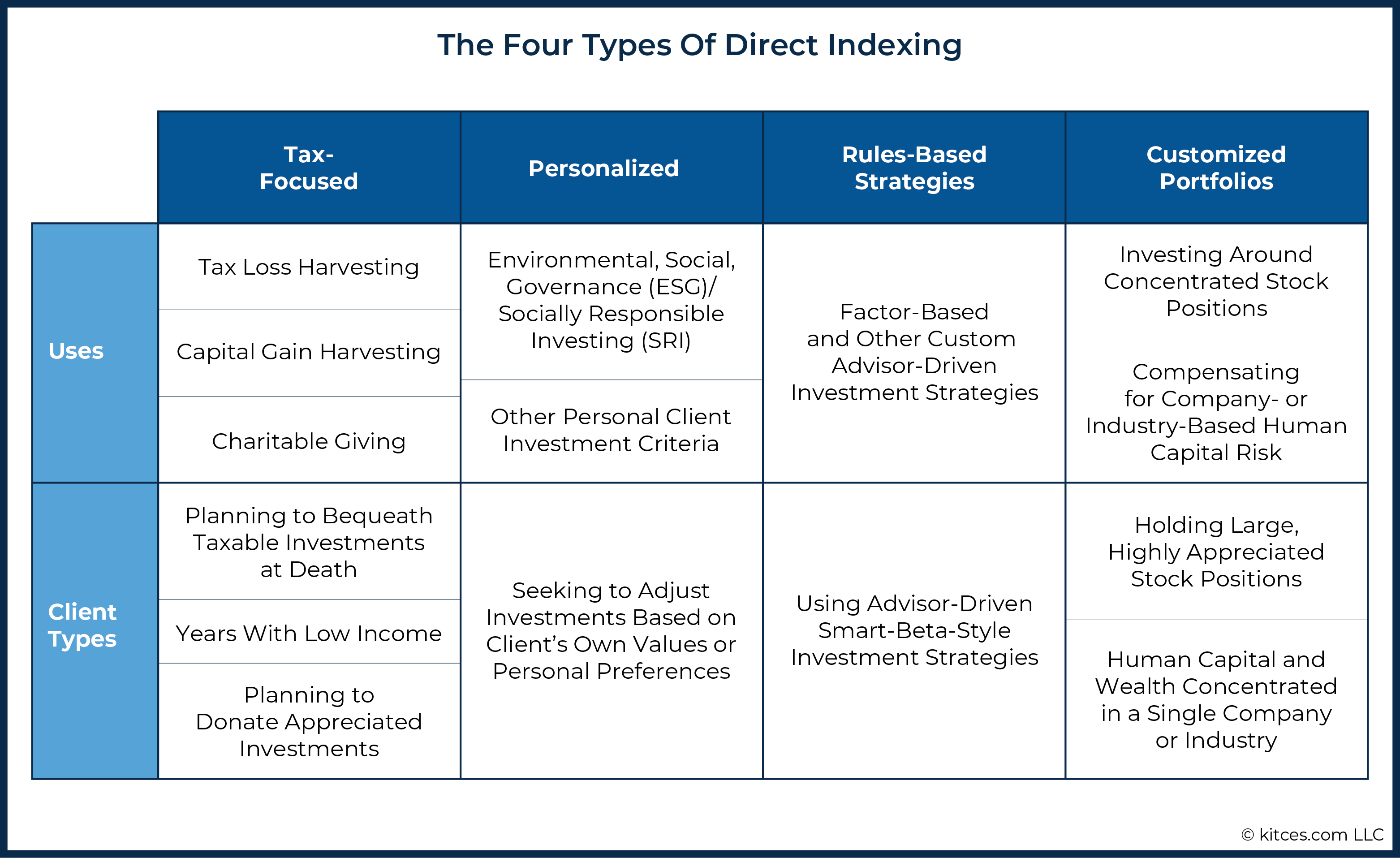

Unlocking the Power of Tax-Loss Harvesting

The most significant “alpha” or outperformance generated by direct indexing comes from tax-loss harvesting. In a traditional ETF, you only realize a capital loss if the entire index drops below your purchase price. However, even in a “up” year for the market, individual stocks within an index frequently decline.

With direct indexing, an automated system can identify these declining stocks, sell them to “harvest” the capital loss, and immediately replace them with a highly correlated stock to maintain the index’s characteristics. These harvested losses can be used to offset capital gains from other investments (like the sale of a business or real estate) or up to $3,000 of ordinary income. Over time, this “tax alpha” can add 0.20% to over 1.00% to an investor’s annual net return, depending on their tax bracket and market volatility.

Values-Based Investing and ESG Customization

Modern investors increasingly want their portfolios to reflect their personal values, often referred to as Environmental, Social, and Governance (ESG) investing. While there are many ESG-themed ETFs, they are static. An ESG ETF might exclude oil companies but include tech giants that an investor may personally find objectionable for privacy reasons.

Direct indexing allows for “tilting” or “screening.” An investor can start with the S&P 500 as a base but instruct the system to “exclude all tobacco companies” or “overweight companies with high board diversity.” This level of surgical precision ensures that the portfolio is not just a financial tool, but an extension of the investor’s personal philosophy.

Managing Concentration Risk and Sector Exposure

Direct indexing is an invaluable tool for corporate executives or employees who receive significant compensation in the form of company stock. If a senior manager at a major tech firm already has 40% of their wealth tied up in their employer’s stock, buying a standard S&P 500 index fund (which is heavily weighted toward tech) actually increases their risk.

Through direct indexing, that investor can build an index that specifically excludes their employer’s stock and the broader industry they work in. This “completion portfolio” balances their overall financial life, ensuring that a downturn in their specific company or sector doesn’t result in a total financial catastrophe.

Evaluating the Costs and Complexity

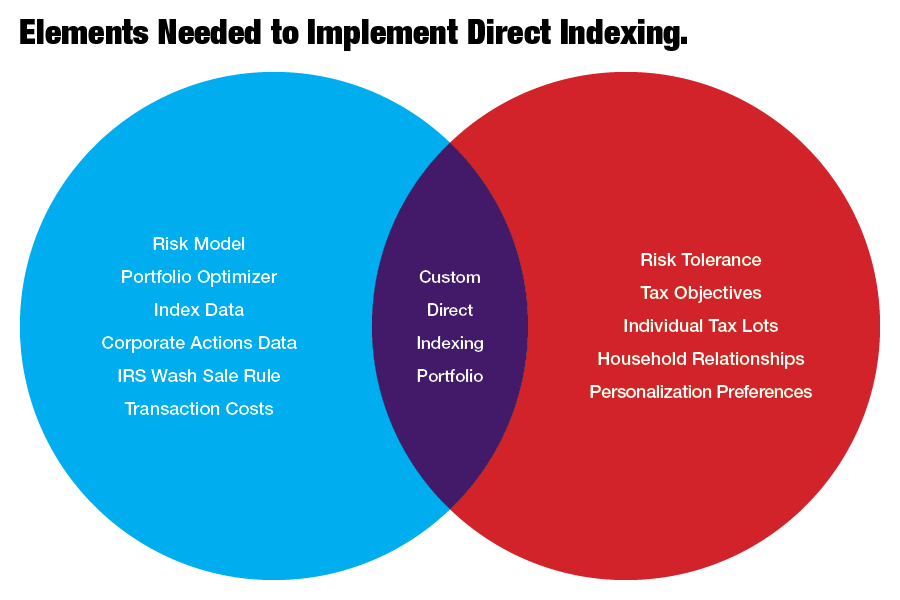

While the benefits of direct indexing are compelling, it is not a “free lunch.” The strategy introduces layers of complexity and costs that investors must weigh against the potential tax savings.

Fee Structures vs. Expense Ratios

Standard index ETFs have become incredibly cheap, with many charging expense ratios as low as 0.03%. Direct indexing is generally more expensive. Because it requires sophisticated software and often involves an investment advisor to oversee the strategy, the total cost can range from 0.15% to 0.40% or more.

Investors must perform a cost-benefit analysis: is the 0.25% extra in fees justified by the 0.50% or 1.00% in tax savings? For someone in a low tax bracket with few capital gains, the math may favor the cheaper ETF. For a high-net-worth individual in a state like California or New York, the tax savings almost always eclipse the higher management fee.

Tracking Error: The Price of Customization

“Tracking error” refers to the difference between the performance of your portfolio and the performance of the benchmark index you are trying to mimic. When you start excluding stocks for ESG reasons or selling stocks for tax-loss harvesting, your portfolio will inevitably deviate from the index.

In some years, your customizations might lead you to outperform the index. In other years, you might underperform. Investors using direct indexing must have the stomach for this variance. They are no longer “the market”; they are “the market, modified.” If the S&P 500 is up 20% and your customized direct index is only up 18% due to your specific exclusions, you must be comfortable with that trade-off.

Is Direct Indexing Right for Your Portfolio?

Direct indexing is a powerful tool, but it is not a universal solution for every investor. Determining whether to make the switch from traditional funds to direct ownership depends on several factors, including portfolio size, tax situation, and investment goals.

Minimum Investment Thresholds and Accessibility

Historically, direct indexing required a minimum of $5 million. As technology has improved, those floors have dropped significantly. Many digital wealth platforms and major brokerages now offer direct indexing for accounts starting at $100,000, and some fintech startups are pushing that even lower.

However, even if you can access it with a smaller amount, it may not be efficient. The complexity of managing 500 stocks creates a significant amount of data and a much longer tax return (Form 8949 can become dozens of pages long). For a $10,000 account, the administrative headache and the higher fee ratio often make direct indexing an illogical choice compared to a simple, low-cost ETF.

When to Stick with Traditional Index Funds

Traditional index funds remain the superior choice for several types of accounts and investors. For instance, in tax-advantaged accounts like a 401(k) or an IRA, the primary benefit of direct indexing—tax-loss harvesting—is irrelevant because trades within those accounts are not taxed. Therefore, paying a higher fee for direct indexing in a retirement account is essentially paying for a benefit you cannot use.

Additionally, for investors who prioritize simplicity and “set-it-and-forget-it” management, the streamlined nature of an ETF is hard to beat. Direct indexing requires a higher level of engagement and a deeper understanding of tax law.

Conclusion: The Future of Personalized Finance

Direct indexing represents the natural evolution of the “Money” niche—moving from mass production to mass customization. Just as technology allowed for the transition from expensive actively managed mutual funds to low-cost ETFs, it is now allowing for the transition to personalized, direct ownership.

For the strategic investor, direct indexing provides a way to optimize for the only thing that truly matters: the amount of money you keep after taxes. By leveraging technology to harvest losses and align portfolios with personal values, direct indexing turns a passive investment strategy into a dynamic financial advantage. As costs continue to fall and accessibility rises, it is likely that direct indexing will become a foundational component of the modern diversified portfolio.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.