In the world of mathematics, a rate is defined as a ratio that compares two different quantities which have different units. While this definition might sound like a simple concept found in a middle school textbook, it serves as the fundamental bedrock of the global financial system. When we transition from the classroom to the boardroom or the personal brokerage account, understanding “what is a rate in math” becomes the difference between financial literacy and costly ignorance.

In finance, rates are the pulse of the economy. They dictate how much your savings will grow, how much a mortgage will cost, and how quickly the value of a currency fluctuates against another. To truly master your money, you must first master the mathematical application of rates.

Understanding the Mathematical Foundation of Rates in Finance

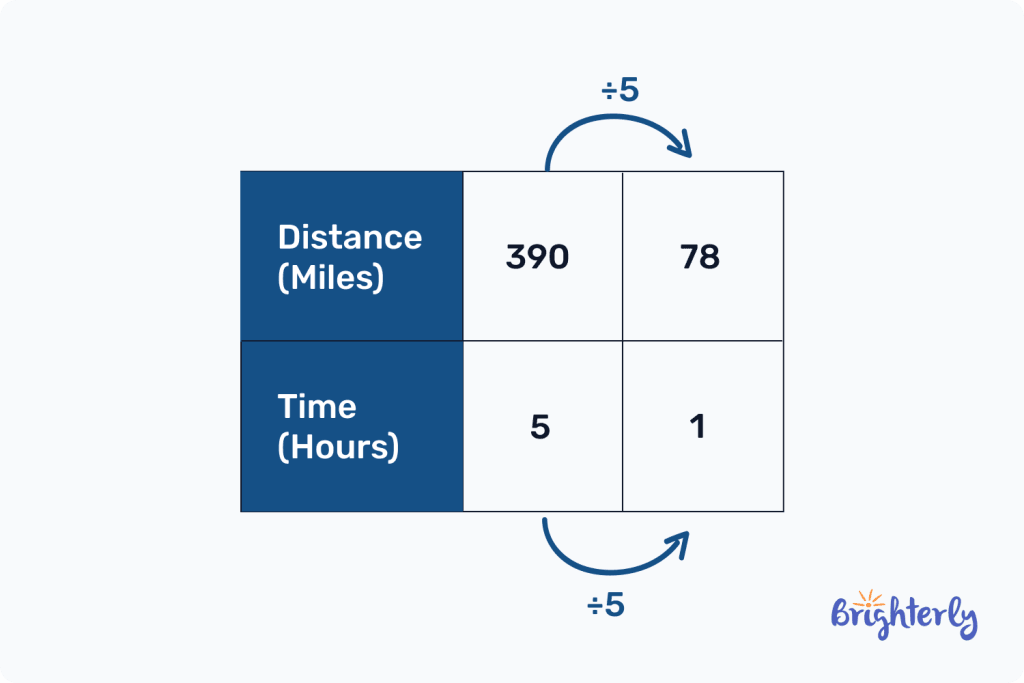

Before diving into complex investment strategies, we must establish a clear mathematical baseline. At its core, a rate is a comparison. If a car travels 60 miles in one hour, the rate is 60 miles per hour. In finance, if a bank pays you $5 for every $100 you deposit over a year, the rate is 5% per annum.

Defining a Rate: Ratios, Proportions, and Units

Mathematically, a rate is expressed as a fraction. The numerator represents one quantity, and the denominator represents another. The distinguishing factor of a “rate” compared to a standard “ratio” is that the units must be different. For example, comparing five apples to ten apples is a ratio (units are the same). Comparing five dollars to one hour of work is a rate (units are different: currency vs. time).

In the context of money, the most common denominator is time. Whether we are discussing interest rates, inflation rates, or rates of return, we are almost always measuring a change in value over a specific duration. This temporal element is what allows investors to project future wealth and calculate the present value of future cash flows.

The Difference Between a Ratio and a Rate in Wealth Management

In financial analysis, we use both ratios and rates, but they serve different purposes. A “Price-to-Earnings (P/E) ratio” compares two dollar amounts (Price per share and Earnings per share), essentially canceling out the units to provide a multiplier.

Conversely, a “Dividend Growth Rate” measures the percentage increase in dividends over time. Understanding this distinction is vital. A ratio tells you where a company stands at a static moment in time; a rate tells you how fast that company is moving. For a sophisticated investor, the rate is often more important than the ratio because it indicates momentum and future potential.

Interest Rates: The Cost of Money and the Power of Compounding

Perhaps the most significant application of rates in the “Money” niche is the interest rate. Mathematically, an interest rate is the percentage of a principal amount charged by a lender to a borrower or paid by a bank to a saver.

Simple Interest vs. Compound Interest

The mathematical divergence between simple and compound interest is where many individuals fail to optimize their finances.

- Simple Interest is calculated only on the principal amount. The formula is $I = P times r times t$ (Interest = Principal × Rate × Time).

- Compound Interest is calculated on the principal plus any accumulated interest.

The mathematical formula for compound interest—$A = P(1 + r/n)^{nt}$—is arguably the most powerful tool in personal finance. Because the “rate” is applied to an ever-increasing base, the growth is exponential rather than linear. Understanding the math behind this rate allows an investor to see that even a small 1% difference in a rate can result in hundreds of thousands of dollars in difference over a 30-year period.

Annual Percentage Rate (APR) vs. Annual Percentage Yield (APY)

When dealing with credit cards or savings accounts, you will encounter two different mathematical expressions of a rate: APR and APY.

- APR (Annual Percentage Rate) represents the simple interest rate over a year.

- APY (Annual Percentage Yield) takes into account the effect of compounding within that year.

If a savings account has a monthly compounding schedule, the APY will be higher than the APR. Mathematically, lenders prefer to advertise the APR (because it looks lower), while banks looking for deposits prefer to highlight the APY (because it looks higher). Recognizing the math behind these rates prevents you from comparing “apples to oranges” when choosing financial products.

Economic Rates: Navigating Inflation, Exchange, and Taxation

Moving from personal accounts to the broader economy, rates act as the primary indicators of a nation’s financial health. These rates influence everything from the price of a loaf of bread to the success of international trade.

Inflation Rates: The Erosion of Purchasing Power

The inflation rate is a mathematical measurement of the percentage increase in the price level of a basket of goods and services over a period. It is a “rate of change.” If the inflation rate is 3%, $100 today will only have the purchasing power of $97 next year.

For an investor, the math of inflation is a hurdle. If your investment “rate of return” is 5% but the “inflation rate” is 6%, your real rate of return is actually -1%. You are mathematically losing wealth despite seeing a “nominal” increase in your balance. Mastering money requires always calculating the “real” rate versus the “nominal” rate.

Exchange Rates: Mathematical Valuation in Global Trade

An exchange rate is the rate at which one currency can be exchanged for another. It is a ratio of values. For example, if the USD/EUR exchange rate is 0.92, one U.S. Dollar is worth 0.92 Euros.

In the world of forex trading and international business finance, these rates are in constant flux. A “floating rate” is determined by the mathematical equilibrium of supply and demand in the global market. Businesses that operate internationally must use “hedging” strategies to protect themselves from “exchange rate risk”—the mathematical possibility that a shift in the rate will erase their profit margins.

Investment Rates of Return: Measuring Portfolio Success

How do you know if you are a good investor? You look at your rates. In finance, we use several mathematical formulas to determine the efficiency of an investment.

ROI and CAGR: Quantifying Growth Over Time

The most basic measurement is Return on Investment (ROI). The formula is:

[(Current Value - Original Cost) / Original Cost] * 100.

However, ROI does not account for time. If you made a 50% ROI, was that over one year or twenty years? This is where the Compound Annual Growth Rate (CAGR) comes in. CAGR provides a constant rate of return over a specific time period, assuming the profits were reinvested. Mathematically, it “smooths out” the volatility of the market to give you a clear picture of annual performance. It is the gold standard for comparing the performance of different asset classes, such as stocks versus real estate.

The Rule of 72: A Mathematical Shortcut for Investors

One of the most useful mathematical “tricks” involving rates is the Rule of 72. If you want to know how long it will take for your money to double at a given interest rate, divide 72 by the annual rate of return.

- At a 6% rate, your money doubles in 12 years (72 / 6).

- At a 10% rate, your money doubles in 7.2 years (72 / 10).

This mental math allows investors to quickly assess the impact of different rates on their long-term wealth without needing a complex calculator.

Strategic Application: Using Rate Mathematics to Achieve Financial Freedom

Ultimately, the goal of understanding “what is a rate in math” within a financial context is to apply that knowledge to your personal strategy. Success in money is rarely about how much you earn; it is about the rates you control.

Optimizing Your Savings Rate

The “Savings Rate” is the most critical number in personal finance. It is calculated by dividing your monthly surplus by your gross income. If you earn $5,000 and save $1,000, your savings rate is 20%.

Mathematical modeling shows that your savings rate has a much higher impact on your “Time to Financial Independence” than your investment return rate does in the early stages of wealth building. By increasing the rate at which you retain capital, you provide more “fuel” for the interest rates to act upon through compounding.

Debt Management and Rate Arbitrage

Finally, understanding rates allows for “Rate Arbitrage.” This is a strategy where you borrow money at a low rate and invest it at a higher rate. For instance, if you have a mortgage at a 3% fixed rate, but you can earn 7% in a diversified index fund, the math suggests you should not pay off the mortgage early. Instead, you “pocket the spread” of 4%.

This advanced financial maneuver is entirely dependent on a precise mathematical understanding of how different rates interact. If you don’t understand the math, you cannot see the opportunity.

In conclusion, a rate is far more than a mathematical definition; it is the fundamental tool for measuring, growing, and protecting wealth. By viewing your finances through the lens of rates—interest rates, inflation rates, and savings rates—you move from being a passive observer of your money to being its master. Whether you are calculating the APY on a high-yield savings account or the CAGR of a tech stock, the math remains the same: it is all about the relationship between value and time.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.