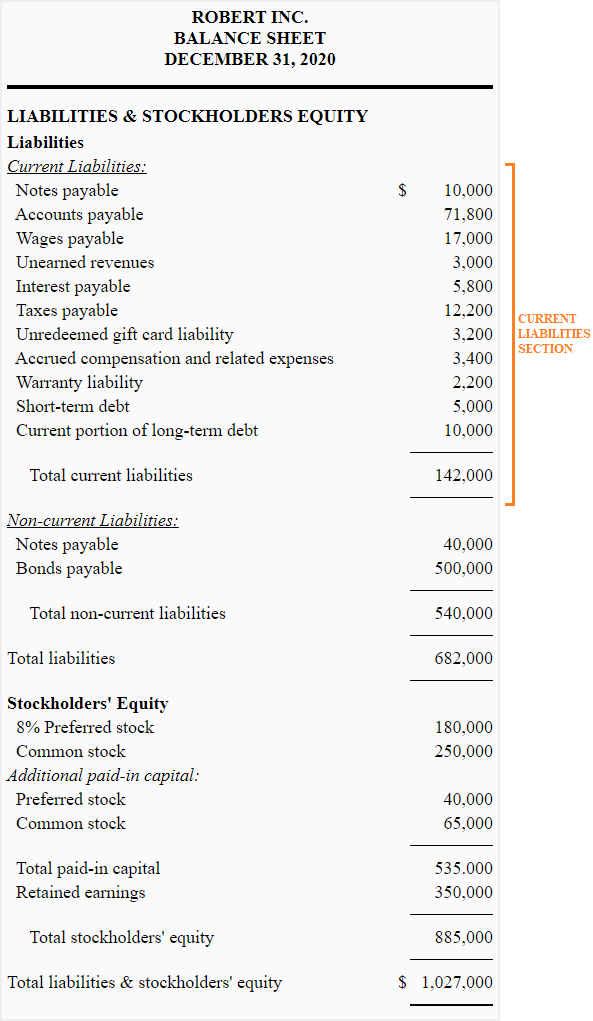

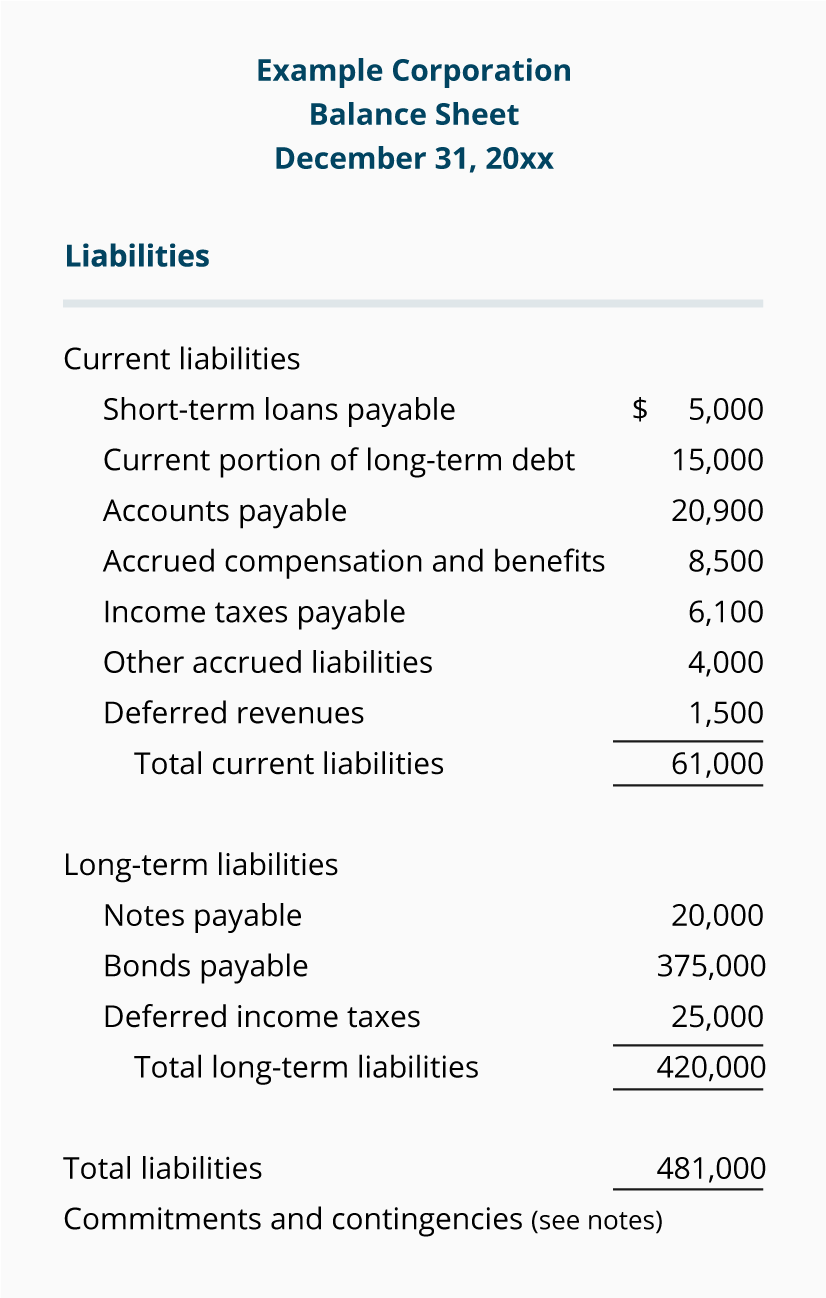

In the world of business finance and personal accounting, the balance sheet serves as a primary health check for any entity. Among its most critical components are liabilities—the debts and obligations owed to outside parties. However, not all debts are created equal. To understand a company’s immediate financial viability and its ability to meet its promises, one must look specifically at current liabilities.

Current liabilities represent the short-term financial obligations that a business or individual is expected to settle within one year or within a single operating cycle. They are the “bills” of the business world, and managing them effectively is the difference between a thriving enterprise and one facing a liquidity crisis. This article explores the nuances of current liabilities, their impact on financial ratios, and why they are a cornerstone of sound fiscal management.

Understanding the Fundamentals of Current Liabilities

At its core, a current liability is a debt that requires a near-term outflow of resources—usually cash—to satisfy. On a standard balance sheet, liabilities are categorized by their maturity dates. While long-term liabilities like mortgages or 30-year bonds represent future commitments, current liabilities are the immediate hurdles that must be cleared to keep the doors open.

Definition and the “One-Year” Rule

The standard accounting definition of a current liability is any obligation due within one year. However, for some industries with long production times (such as shipbuilding or heavy infrastructure), this definition may expand to include the “operating cycle”—the time it takes to turn cash into inventory and back into cash. For the vast majority of businesses and personal finance scenarios, the twelve-month rule is the gold standard. These liabilities are typically settled using current assets, which are resources like cash, accounts receivable, or inventory that are expected to be converted into cash within the same timeframe.

The Relationship Between Assets and Liabilities

Current liabilities do not exist in a vacuum; they are intrinsically linked to a company’s liquidity. Liquidity refers to how easily an entity can meet its short-term obligations without incurring devastating losses. If a company has $1 million in current liabilities but only $500,000 in cash and liquid assets, it faces a significant risk of insolvency. Understanding this balance is fundamental to business finance, as it dictates how much “breathing room” a manager has to navigate market fluctuations.

Common Examples of Current Liabilities in Business Finance

To master the management of short-term debt, one must recognize the various forms these obligations take. While some are straightforward invoices, others are complex accounting entries that represent future work or deferred payments.

Accounts Payable

Accounts payable (AP) is perhaps the most common current liability. It represents the money a company owes to its suppliers for goods or services purchased on credit. For example, if a retail store receives a shipment of electronics but has 30 days to pay the invoice, that amount sits in accounts payable. AP is a vital tool for cash flow management; by negotiating longer payment terms with vendors, a business can keep its cash longer, using it for other operational needs before the bill comes due.

Short-Term Loans and Notes Payable

Businesses often take out short-term loans to cover seasonal gaps in cash flow or to fund immediate projects. Notes payable are formal written promises to pay a specific sum of money at a certain date, usually with interest. Unlike accounts payable, which are often interest-free if paid on time, short-term notes typically carry a cost of capital. Monitoring these is crucial because a high volume of short-term interest-bearing debt can quickly erode profit margins.

Accrued Expenses and Unearned Revenue

Accrued expenses are liabilities that have been incurred but not yet paid or invoiced. A classic example is wages; employees work throughout the month, but the company might not pay them until the 1st of the following month. During that interval, the owed wages are an accrued liability.

Unearned revenue, or deferred revenue, is a unique type of liability. It occurs when a customer pays for a service or product in advance. While the company has the cash, it has not yet earned it. Until the product is delivered or the service is rendered, the company “owes” that value to the customer. If the company fails to deliver, that money must theoretically be returned, making it a current liability.

The Role of Current Liabilities in Financial Health Ratios

For investors, creditors, and business owners, the raw dollar amount of current liabilities is less important than how that amount relates to other financial figures. Financial ratios provide a standardized way to measure a company’s “health” regardless of its size.

The Current Ratio: Measuring Liquidity

The Current Ratio is the most fundamental metric for assessing short-term solvency. It is calculated by dividing total current assets by total current liabilities.

- Formula: Current Assets / Current Liabilities = Current Ratio

A ratio above 1.0 indicates that the company has more assets than liabilities due within the year. Generally, a ratio between 1.5 and 3.0 is considered healthy. If the ratio is too low, the company may struggle to pay its bills. If it is excessively high, it might suggest that the company is not using its cash efficiently to grow the business.

The Quick Ratio: The Acid Test

While the current ratio is helpful, it can be misleading if a company’s assets are tied up in inventory that is hard to sell. The Quick Ratio (or Acid-Test Ratio) provides a more conservative view by excluding inventory from the calculation.

- Formula: (Current Assets – Inventory) / Current Liabilities = Quick Ratio

This ratio measures a company’s ability to meet its short-term obligations using only its most liquid assets—cash and accounts receivable. This is a critical metric for lenders who want to know if a business can survive a sudden downturn in sales.

Working Capital Management

Working capital is the difference between current assets and current liabilities. It represents the operational liquidity available to a business. Positive working capital is necessary for a business to pay its employees and suppliers and to meet its obligations while waiting for payments from customers. Effective “Money” management involves optimizing the working capital cycle—speeding up the collection of receivables while strategically managing the timing of liability payments.

Why Current Liabilities Matter to Investors and Creditors

In the broader context of personal and business finance, current liabilities serve as a primary indicator of risk. Understanding how a company handles its short-term debt offers deep insights into its operational efficiency and long-term viability.

Assessing Solvency and Bankruptcy Risk

A sudden spike in current liabilities without a corresponding increase in assets is a major red flag for investors. It often signals that a company is “borrowing from Peter to pay Paul”—using short-term credit to cover operating losses. If a company cannot refinance its short-term debt or pay it off through operations, it may be forced into liquidation or bankruptcy. Creditors look at the total “debt load” to determine the interest rates they will charge; higher perceived risk leads to higher borrowing costs, which further pressures the company’s finances.

Operational Efficiency Indicators

Current liabilities also tell a story about how a company manages its relationships. A company that consistently pays its accounts payable on time likely enjoys strong relationships with suppliers, which can lead to better pricing and priority service. Conversely, if a company is stretching its payables (taking 90 days to pay a 30-day invoice), it may be a sign of cash flow distress. By analyzing the “Accounts Payable Turnover Ratio,” investors can determine how many times per period a company pays off its creditors, providing a window into its organizational discipline.

Strategies for Managing Current Liabilities Effectively

Managing current liabilities is not just about paying bills; it is about strategic timing and capital optimization. Whether in a corporate setting or personal finance, the goal is to maintain a balance that supports growth without inviting excessive risk.

Optimizing Cash Flow Cycles

One of the most effective ways to manage liabilities is to align them with the “Cash Conversion Cycle.” This involves shortening the time it takes to sell inventory and collect receivables while maximizing the time allowed to pay creditors. For example, a business might offer discounts to customers who pay early (improving asset liquidity) while utilizing the full 30 or 60-day window offered by their own suppliers. This “free” credit from vendors is one of the most cost-effective ways to finance operations.

Negotiating Terms and Consolidating Debt

In times of financial tightening, proactive management of current liabilities is essential. This can include negotiating extended payment terms with key vendors or consolidating several high-interest short-term loans into a single lower-interest long-term loan. By moving debt from “current” to “long-term,” a company can improve its current ratio and alleviate immediate cash flow pressure, giving it the necessary room to pivot its strategy or expand its market share.

In conclusion, current liabilities are more than just a list of debts; they are a vital barometer of financial health. By understanding what they are, how they are calculated, and how they interact with assets, anyone involved in business or personal finance can make more informed decisions. Proper management of these short-term obligations ensures that a business remains liquid, credible, and ready to seize future opportunities.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.