In the world of finance, numbers are more than just digits on a screen; they are the narrative of your economic health. Whether you are tracking the performance of a stock portfolio, analyzing the growth of a small business, or simply trying to understand the impact of inflation on your monthly budget, the ability to calculate percentage increase and decrease is an essential skill. Mastery of these calculations allows investors and professionals to move beyond surface-level data and gain a deeper understanding of trends, volatility, and value.

This guide explores the mathematical foundations of percentage changes through the lens of personal and business finance, providing you with the tools necessary to make informed, data-driven decisions.

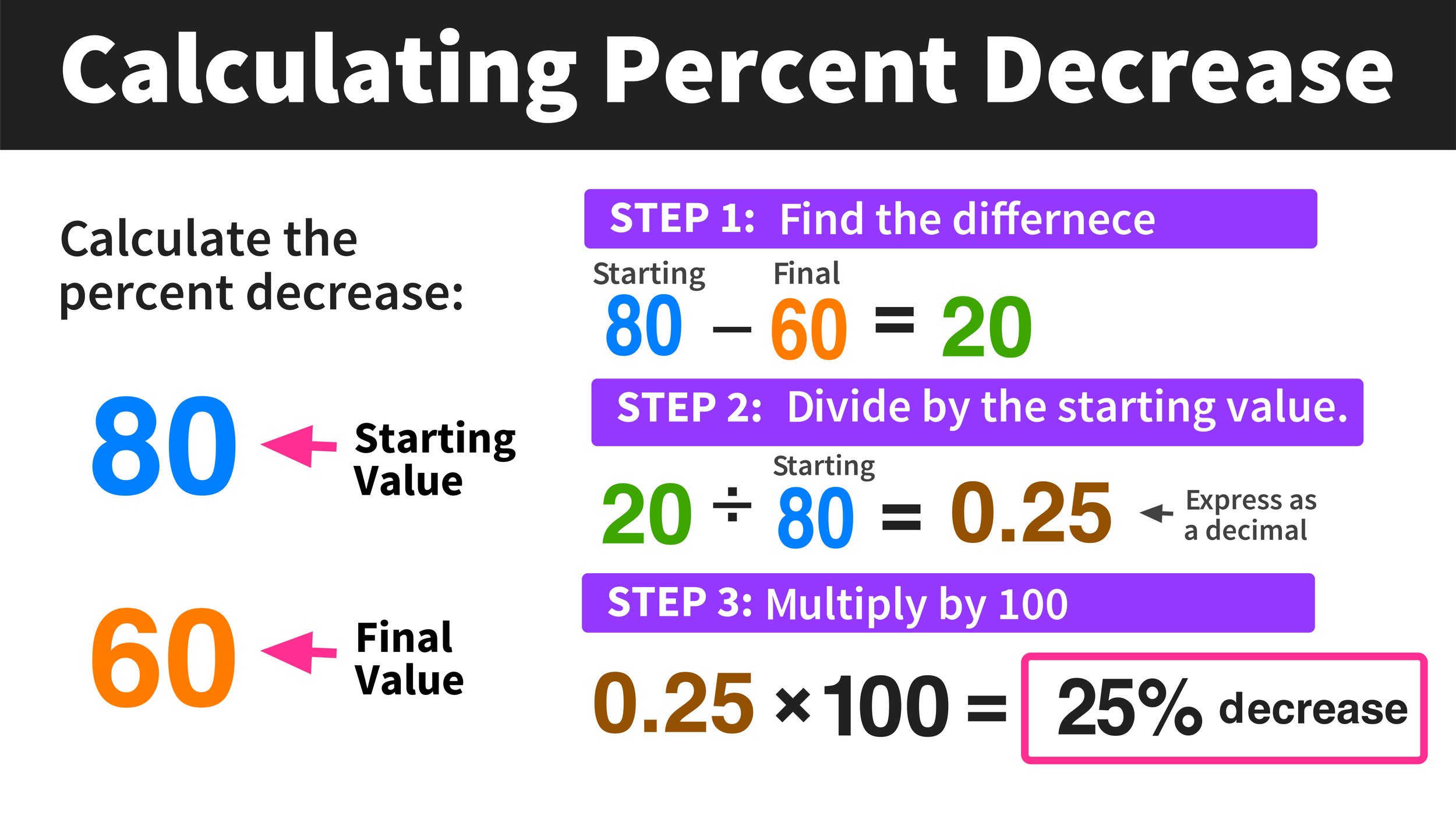

1. The Core Mechanics: Understanding the Percentage Change Formula

At its heart, calculating a percentage change is the process of measuring the relative difference between an old value and a new value. In financial terms, this represents the rate of return, the rate of loss, or the pace of growth over a specific period.

The Universal Formula

To find the percentage increase or decrease, you follow a simple three-step process:

- Subtract the original value (the “old” number) from the new value.

- Divide that result by the original value.

- Multiply the final number by 100 to convert it into a percentage.

The Formula: ((New Value - Old Value) / |Old Value|) × 100

Interpreting the Results

When you apply this formula, the sign of the resulting number tells you the direction of the change. A positive result indicates a percentage increase, signifying growth, profit, or an appreciation in value. Conversely, a negative result indicates a percentage decrease, representing a loss, a discount, or a depreciation in value. In the context of money management, distinguishing between these two is the first step in auditing your financial performance.

Why the Base Value Matters

A common mistake in financial analysis is dividing by the “new” value instead of the “old” value. In finance, the original investment is your “base.” If you invest $1,000 and it grows to $1,200, your growth is relative to the $1,000 you started with. Understanding this “base-level” logic is crucial because it ensures that your calculations accurately reflect the reality of your capital’s movement.

2. Mastering Percentage Increase for Wealth Building

For any investor or entrepreneur, a percentage increase is the ultimate goal. It represents the “plus side” of the ledger—the dividends, the capital gains, and the revenue growth that build long-term wealth.

Tracking Investment Performance and ROI

The most common application of percentage increase in finance is calculating the Return on Investment (ROI). If you purchased shares in a technology company at $150 per share and the price rises to $210, you need to know the percentage increase to compare this asset’s performance against other benchmarks like the S&P 500.

Using our formula: ((210 - 150) / 150) × 100 = 40%.

A 40% increase is a clear metric that allows you to evaluate whether that specific investment is meeting your financial goals. Without converting these dollar amounts into percentages, it becomes difficult to compare a $60 gain on a $150 stock to a $60 gain on a $1,000 stock.

Analyzing Business Revenue and Profit Margins

For business owners, calculating percentage increases in monthly or annual revenue is vital for scaling. If your business earned $50,000 in Q1 and $65,000 in Q2, that 30% increase indicates successful marketing or operational efficiency. Furthermore, understanding the percentage increase in costs is equally important. If your revenue increased by 30% but your overhead costs increased by 50%, your business is actually becoming less profitable despite higher sales.

The Power of Compounding Percentages

In the realm of personal finance, the “increase” is often cumulative. Compound interest is essentially a percentage increase applied to a balance that has already experienced a percentage increase. By understanding the math, you can better visualize how a steady 7% annual increase can double your wealth over approximately ten years (the Rule of 72). This perspective shifts the focus from short-term wins to long-term mathematical certainties.

3. Navigating Percentage Decrease and Risk Management

While increases build wealth, percentage decreases are the obstacles that must be managed. In finance, a decrease can represent everything from a market correction to the eroding power of inflation.

Calculating Portfolio Drawdowns

In investing, a “drawdown” refers to the percentage decrease from a peak to a trough. If your retirement account hits a high of $500,000 but drops to $425,000 during a market downturn, you have experienced a 15% decrease. Understanding the magnitude of these decreases is essential for risk tolerance. Knowing how to calculate this allows you to set “stop-loss” orders or determine when a portfolio rebalance is necessary to protect your capital.

The Stealth Decrease: Inflation and Purchasing Power

One of the most critical applications of percentage decrease is understanding the “real value” of money. Inflation is a percentage increase in the price of goods, which results in a percentage decrease in the purchasing power of your currency. If inflation is at 5%, the $100 in your pocket effectively “decreases” in value because it can buy 5% fewer goods than it could the year before. For those living on a fixed income or holding large amounts of cash, calculating this decrease is a survival skill that informs how much one needs to invest to outpace rising costs.

Discounting and Consumer Finance

On a more practical, day-to-day level, percentage decreases are used in budgeting and shopping. When a financial tool or a service offers a “25% discount,” you are looking at a percentage decrease in price. Being able to quickly reverse-calculate—or verify—these decreases ensures that you are actually receiving the value promised by retailers and service providers.

4. Advanced Insights: The Asymmetry of Gains and Losses

One of the most profound lessons in financial mathematics is the asymmetrical relationship between percentage increases and decreases. This is a concept that every serious investor must internalize to manage risk effectively.

The “Recovery” Math

A common misconception is that if an asset loses 50% of its value, it only needs a 50% gain to return to its original price. This is mathematically false and a dangerous trap for the uninformed.

Imagine you have $100. It decreases by 50%. You now have $50. To get back to $100, your $50 must increase by $50. However, $50 is 100% of your current balance. Therefore, a 50% loss requires a 100% gain just to break even.

This mathematical reality highlights why avoiding large percentage decreases (losses) is often more important for long-term wealth than chasing large percentage increases. The deeper the percentage decrease, the exponentially harder the “percentage increase” must work to recover the lost ground.

Using Ratios to Contextualize Change

In business finance, percentage changes are often used alongside ratios. For instance, a 10% increase in debt might be acceptable if accompanied by a 20% increase in equity. By calculating percentage changes across different line items on a balance sheet, financial analysts can spot “red flags” where expenses are increasing at a faster percentage rate than income.

5. Tools and Automation for Financial Accuracy

While knowing the formula is essential for conceptual understanding, modern finance relies on tools to handle these calculations at scale. Accuracy is paramount; a misplaced decimal point in a percentage calculation can lead to significant financial errors.

Leveraging Spreadsheets (Excel and Google Sheets)

For personal budgeting or business tracking, spreadsheets are the gold standard. To calculate percentage change in Excel, you would use a formula like: =(B2-A2)/A2, where A2 is the old value and B2 is the new value. By formatting the cell as a “Percentage,” the software automatically handles the “multiply by 100” step. This allows you to track hundreds of data points—such as daily stock price changes—instantaneously.

Financial Calculators and Fintech Apps

Most modern investment platforms and banking apps provide these calculations for you. When you open a brokerage app, the “Total Return” percentage you see is a real-time calculation of percentage increase or decrease from your cost basis. However, understanding the manual calculation allows you to “audit” these apps and understand exactly what they are measuring (e.g., are they including dividends in the percentage increase, or just the share price?).

Strategic Decision Making

Ultimately, the goal of calculating percentage changes is to facilitate better decision-making. Should you sell a stock that has increased by 20%? Should you cut costs in a department where spending has decreased by only 2% while revenue dropped by 10%? These numbers provide the objective framework needed to remove emotion from financial management.

By consistently applying the principles of percentage increase and decrease, you transform from a passive observer of your finances into an active strategist. You begin to see the movement of money not as random fluctuations, but as measurable trends that can be anticipated, managed, and optimized for long-term prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.