Understanding the history of financial markets is not merely an academic exercise; for the modern investor, it is a prerequisite for survival. When people ask, “When was the stock market crash?” they are often looking for a single date, but history reveals a series of pivotal moments that have reshaped the global economy. From the speculative frenzy of the 1920s to the algorithmic lightning strikes of the 21st century, each crash offers unique lessons in risk management, human psychology, and the resilience of capital markets.

In this comprehensive guide, we will explore the major stock market crashes in history, examining their causes, their impacts, and the strategic takeaways that can help you protect your personal finance portfolio today.

The Great Depression and the Watershed Moment of 1929

The most famous answer to the question of when the stock market crashed is, undoubtedly, 1929. This event remains the gold standard for financial catastrophes, marking the end of an era of unprecedented prosperity and the beginning of a decade of global economic hardship.

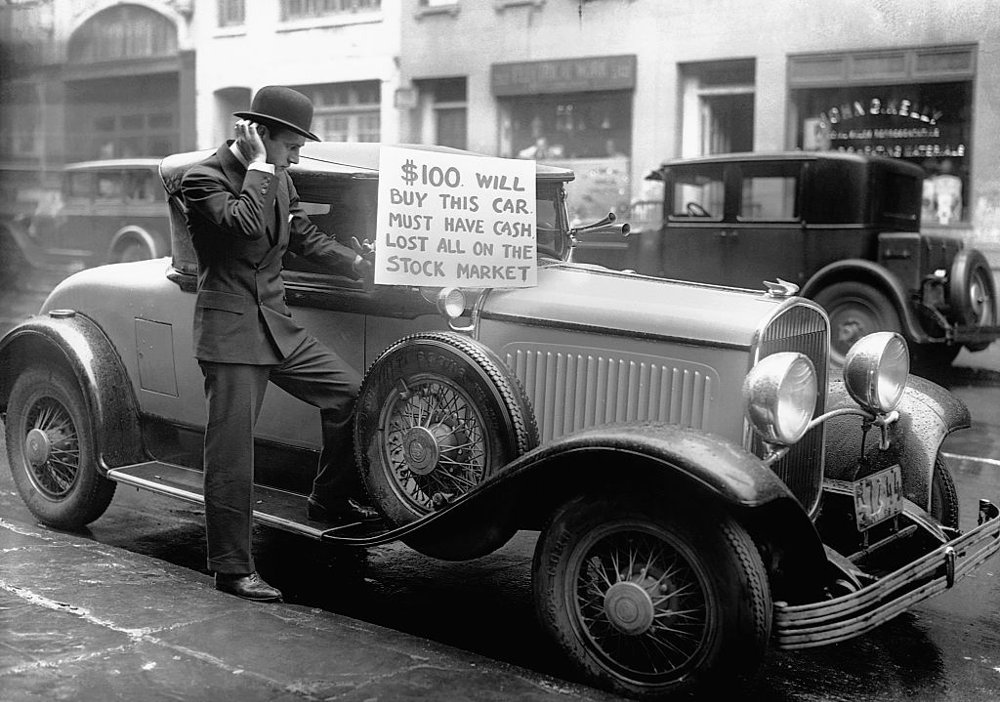

The Roaring Twenties and the Speculative Build-up

The decade leading up to 1929, known as the “Roaring Twenties,” was characterized by rapid industrialization and the birth of a consumerist culture. For the first time, the general public began investing in the stock market en masse. However, this enthusiasm was fueled by dangerous financial practices. Investors were buying stocks “on margin,” meaning they were borrowing up to 90% of the purchase price to bet on rising valuations. This leverage created a massive bubble that was disconnected from the actual earnings of the companies involved.

Black Tuesday: October 24–29, 1929

The collapse did not happen in a single hour. It began on “Black Thursday,” October 24, when the market opened 11% lower. After a brief period of institutional intervention, the true panic set in on “Black Tuesday,” October 29. On that day, prices collapsed entirely as investors scrambled to sell their shares at any price. Massive amounts of wealth evaporated instantly, and because so many had bought on margin, they were left with debts they could never hope to repay.

The Aftermath and Lasting Lessons

The 1929 crash was the catalyst for the Great Depression. It led to a complete overhaul of the American financial system, including the creation of the Securities and Exchange Commission (SEC) in 1934. The primary lesson for modern money management is the danger of excessive leverage. When you invest with borrowed money, you amplify your gains, but you also ensure that a market correction can lead to total financial ruin.

Black Monday: The 1987 Algorithmic Shock

For decades after the Great Depression, the markets remained relatively stable. That changed on October 19, 1987, a date known as “Black Monday.” This event is unique because, unlike 1929, it wasn’t triggered by a fundamental economic collapse but rather by a failure of the market’s internal mechanics.

The Sudden Descent of October 19

On Black Monday, the Dow Jones Industrial Average (DJIA) plummeted by 22.6% in a single day. To put that into perspective, it remains the largest one-day percentage drop in history. The crash was global, spreading from Hong Kong to Europe and finally to the United States. The shock was intensified by the fact that there was no singular “bad news” event that triggered it; rather, it was a cascade of selling orders.

The Role of Program Trading

The 1987 crash introduced the world to the risks of automated finance. “Program trading”—where computers were set to sell stocks automatically if prices hit certain levels—created a “domino effect.” As prices fell, the computers triggered more sells, which drove prices lower, triggering even more sells. This feedback loop showed that technology, while efficient, could also accelerate a panic to levels humans could not control.

The Introduction of Circuit Breakers

In the wake of 1987, regulators introduced “circuit breakers.” These are mandatory market pauses that kick in if the market drops by a certain percentage (such as 7%, 13%, or 20%). The goal is to give investors a chance to breathe and digest information, preventing the kind of mindless algorithmic selling that defined Black Monday. For the modern investor, this highlights the importance of liquidity and the understanding that markets can move faster than human reaction times.

The 21st Century Meltdowns: Dot-Com and the Great Recession

The turn of the millennium brought two distinct types of crashes: one born of technological overexuberance and the other of systemic banking failure.

2000–2002: The Bursting of the Tech Bubble

In the late 1990s, the “Dot-Com” boom saw investors pouring money into any company with a “.com” in its name, regardless of whether the company had a viable business model or even revenue. By March 2000, the Nasdaq peaked before beginning a long, agonizing slide. Unlike the 1987 crash, this wasn’t a one-day event; it was a slow bleed that lasted two years, wiping out 78% of the Nasdaq’s value. The lesson here for personal finance is clear: valuation matters. Investing in “hype” without fundamental data is gambling, not investing.

2008: The Global Financial Crisis and Housing Collapse

The crash of 2008 was perhaps the most systemic threat to the global economy since 1929. Triggered by a collapse in the subprime mortgage market, it led to the failure of major investment banks like Lehman Brothers. The S&P 500 lost approximately 50% of its value from its peak to its trough in March 2009. This era taught investors about “systemic risk”—the idea that even if your stocks are good, if the underlying banking system fails, everything is at risk. It led to an era of “Too Big to Fail” and massive central bank intervention.

Modern Volatility: The 2020 Flash Crash

The most recent major answer to “when was the stock market crash” is the spring of 2020. This crash was unique because it was caused by an external biological factor—the COVID-19 pandemic—rather than internal economic rot.

The Pandemic Panic

In February and March of 2020, as the world began to realize the scale of the pandemic, the stock market experienced its fastest decline into a bear market in history. In just a few weeks, the S&P 500 dropped by 34%. The level of uncertainty was unprecedented, as businesses across the globe shuttered overnight. This period tested the “circuit breakers” established after 1987 multiple times.

Recovery and the New Normal in Investing

What followed was equally unprecedented: a V-shaped recovery. Driven by massive government stimulus and a “retail trading” revolution fueled by apps like Robinhood, the market reached new all-time highs by the end of 2020. This taught investors a modern lesson: the “Fed Put.” The idea that central banks will intervene to support the economy has changed how investors perceive risk. However, it also created a new environment of high inflation and interest rate sensitivity that we are still navigating today.

Strategies for the Modern Investor: Learning from History

Knowing when the stock market crashed is only useful if you use that knowledge to build a more resilient financial future. History proves that crashes are not “if” events, but “when” events.

Diversification as a Shield

Every crash mentioned—1929, 1987, 2008, and 2020—affected different sectors differently. In 2000, tech crashed while value stocks held up better. In 2008, real estate was the epicenter. Diversification across asset classes (stocks, bonds, real estate, and cash) is the only “free lunch” in investing. It ensures that when one sector crashes, your entire net worth doesn’t go with it.

Emotional Intelligence in Bear Markets

The common thread in every crash is human emotion: greed on the way up and fear on the way down. Most individual investors lose money not because the market crashes, but because they sell at the bottom out of fear and buy at the top out of “FOMO” (Fear of Missing Out). Developing a long-term investment policy statement and sticking to it during periods of high volatility is the hallmark of a professional approach to money.

The Importance of Cash Reserves

Finally, history shows that those with “dry powder”—available cash—during a crash are the ones who build generational wealth. While others are forced to sell at a loss to cover their living expenses, the prepared investor uses the crash as a “sale” to buy high-quality assets at a discount. Maintaining a robust emergency fund ensures that you never become a forced seller during a market downturn.

In conclusion, the question of “when was the stock market crash” reminds us that markets are cyclical. From the speculative ruins of 1929 to the lightning-fast recovery of 2020, history teaches us that while the triggers change, the pattern of human behavior remains the same. By staying informed, diversified, and emotionally disciplined, you can navigate these inevitable storms and use them as opportunities to strengthen your financial legacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.