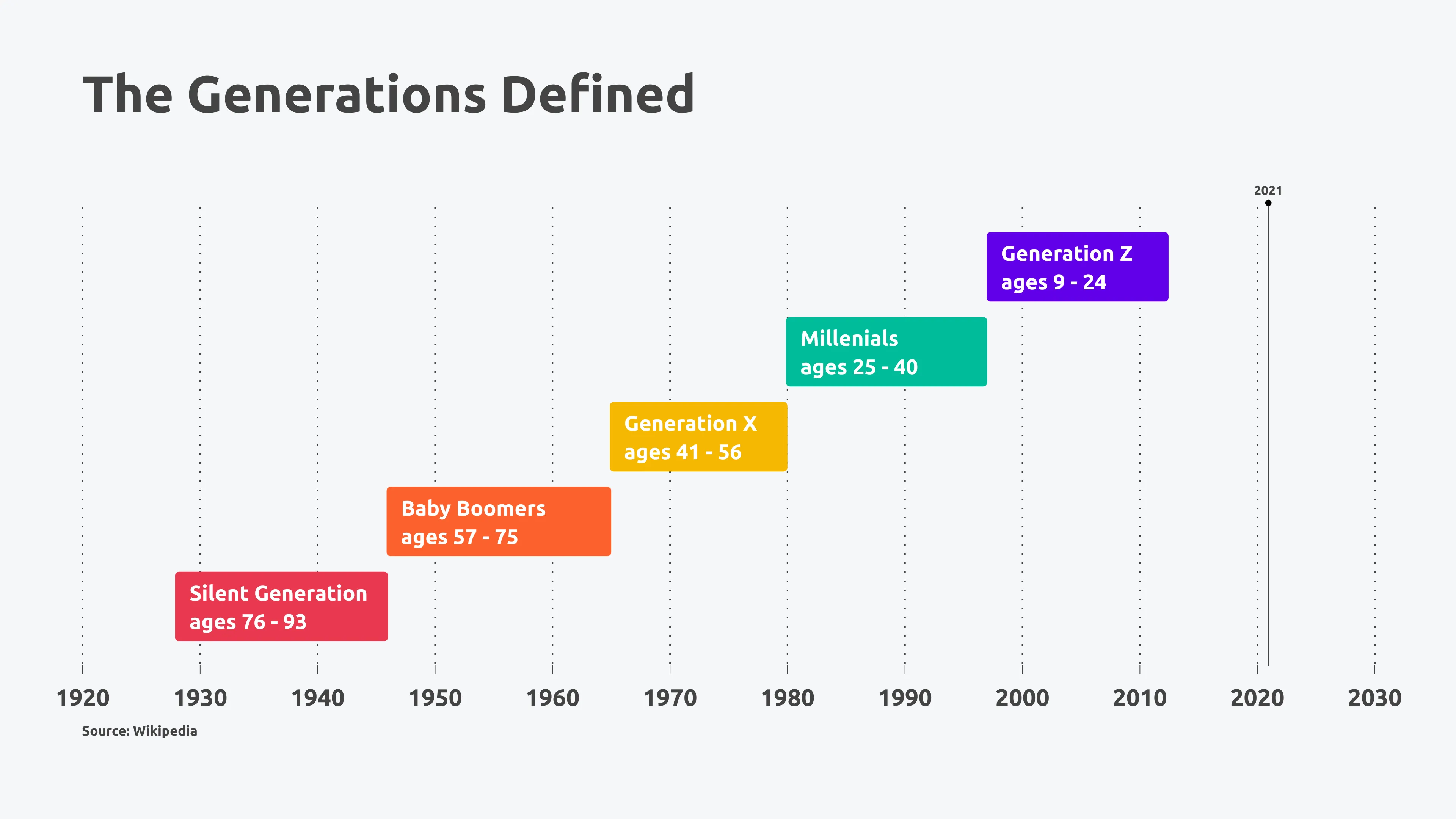

To understand the financial profile of an individual born in 1940, one must first identify their generational cohort: the Silent Generation. Born between 1928 and 1945, this group is often overshadowed by the larger-than-life Greatest Generation that preceded them and the massive Baby Boomer demographic that followed. However, from a financial and economic perspective, the 1940 cohort represents one of the most disciplined and wealthy demographics in history.

Those born in 1940 entered the world at a pivotal moment. The Great Depression was waning, but its scars were deep, and World War II was beginning to reshape the global economy. This unique entry point created a “financial DNA” characterized by caution, resilience, and an extraordinary capacity for long-term wealth accumulation. Today, as this cohort navigates their eighties, their influence on personal finance, estate planning, and the “Great Wealth Transfer” is profound.

Defining the Silent Generation: The Economic Context of 1940

The financial mindset of the 1940 birth year was forged in an era of scarcity and global upheaval. Unlike the post-war optimism that defined the Boomers, those born in 1940 were raised by parents who had lived through the total collapse of the banking system. This upbringing instilled a unique set of fiscal values that remain relevant in today’s volatile market.

The Impact of the Great Depression and WWII on Financial Mindsets

While a child born in 1940 wouldn’t remember the breadlines of the 1930s, they grew up in the immediate aftermath of the Great Depression. The household culture was one of “waste not, want not.” This resulted in a lifelong aversion to unnecessary debt. In the world of personal finance, the 1940 cohort is known for high savings rates and a preference for tangible assets. Their early years were also defined by wartime rationing, which reinforced the idea that resources are finite and must be managed with extreme care.

Scarcity vs. Stability: The Foundation of Lifelong Saving Habits

For someone born in 1940, the concept of “financial security” was never taken for granted. As they entered the workforce in the late 1950s and early 1960s, they benefited from a period of unprecedented economic expansion. However, rather than succumbing to the consumerism that would define later decades, many in this cohort maintained a conservative fiscal posture. They prioritized the “emergency fund” long before it became a standard piece of advice from modern financial influencers. This discipline allowed them to weather subsequent economic downturns, such as the stagflation of the 1970s and the 2008 financial crisis, with greater resilience than younger peers.

Wealth Accumulation and the Golden Age of Pension Systems

The 1940 cohort reached their peak earning years during what many economists call the “Golden Age of Capitalism.” This period provided unique financial vehicles that are largely unavailable to Gen Z or Millennials today, contributing to the significant net worth many individuals in this group hold.

The Rise and Fall of Defined Benefit Plans

One of the most significant financial advantages for those born in 1940 was the prevalence of the “Defined Benefit” pension plan. Unlike the modern 401(k) or IRA, which shifts the investment risk onto the employee, pensions guaranteed a set monthly income for life. This provided the 1940 cohort with a level of retirement “floor” security that is rare in the 21st century. Because their basic needs were often covered by a combination of Social Security and corporate pensions, they were able to invest their surplus capital into other growth vehicles, such as the stock market and real estate.

Real Estate as the Cornerstone of Generational Wealth

The 1940 birth year was perfectly positioned to capitalize on the post-war housing boom. Many purchased their first homes in the 1960s when the price-to-income ratio was significantly lower than it is today. Over the following sixty years, they witnessed a massive appreciation in property values. For many in the Silent Generation, their primary residence became their most successful “investment,” often outperforming their equity portfolios. This “locked-in” wealth is a primary driver of the current discussions surrounding the intergenerational transfer of assets.

Navigating the Modern Financial Landscape in Late Retirement

As individuals born in 1940 transition into their mid-eighties, their financial focus has shifted from accumulation to preservation and distribution. Managing wealth at this stage of life requires a sophisticated understanding of tax law, healthcare costs, and liquidity.

Managing Required Minimum Distributions (RMDs) and Tax Efficiency

For those with significant tax-deferred savings in IRAs or 401(k)s, the 1940 cohort is currently in the thick of Required Minimum Distributions (RMDs). Navigating these withdrawals is a complex financial task. If not managed correctly, RMDs can push a retiree into a higher tax bracket and increase the cost of their Medicare premiums. High-net-worth individuals in this age group often utilize strategies like Qualified Charitable Distributions (QCDs), allowing them to donate their RMD directly to charity to avoid the tax hit—a move that combines philanthropy with savvy tax planning.

The Rising Costs of Healthcare and Long-Term Care Planning

Perhaps the greatest financial challenge for someone born in 1940 is the escalating cost of long-term care. While Medicare covers many medical expenses, it does not cover extended stays in assisted living or memory care facilities. Those who did not purchase long-term care insurance decades ago are now finding themselves “self-insuring” through their savings. This stage of life requires a delicate balance: ensuring there is enough liquidity to pay for high-quality care while attempting to preserve an inheritance for the next generation.

The Great Wealth Transfer: Strategic Estate Planning for the 1940 Cohort

The Silent Generation, including those born in 1940, is currently part of the largest transfer of wealth in human history. It is estimated that trillions of dollars will pass from this generation to their Baby Boomer and Gen X children over the next two decades.

Passing the Torch: Trusts, Wills, and Beneficiary Designations

For the 1940 cohort, estate planning is no longer a “future task”—it is an immediate priority. Professional financial management for this group often involves the creation of Revocable Living Trusts to avoid the cost and publicity of probate. Additionally, there is a heavy focus on “stretch” strategies for beneficiaries, although the SECURE Act of 2019 has changed the rules regarding how quickly heirs must withdraw funds from inherited IRAs. Strategic gifting—utilizing the annual gift tax exclusion—is another common tool used by this generation to reduce the size of their taxable estate while helping their grandchildren with education or first-time home purchases.

Philanthropy and Impact Investing as a Legacy Tool

Many individuals born in 1940 are looking beyond their immediate family to consider their broader impact. We are seeing a surge in “legacy gifting,” where assets are directed toward charitable foundations or donor-advised funds (DAFs). This generation values the idea of “doing well by doing good.” In the realm of business finance, this often manifests as supporting family-run businesses or investing in community-based initiatives that reflect the values they’ve held since the 1940s.

Financial Lessons for Younger Generations from the 1940 Perspective

There is much that modern investors can learn from the “Silent” approach to money. While the economic tools have changed—moving from ledgers to AI-driven trading apps—the underlying principles of the 1940 cohort remain timeless.

Resilience and Long-Term Value Investing

The 1940 cohort understands that markets move in cycles. They have lived through the Cold War, the oil shocks, the dot-com bubble, and the COVID-19 pandemic. Their “quiet” approach to investing usually involves a “buy and hold” strategy rather than chasing the latest crypto trend or meme stock. This patience is a financial superpower. By staying the course over several decades, they have allowed the power of compound interest to work its magic, proving that time in the market is almost always superior to timing the market.

The Importance of Diversification in a Volatile Market

Finally, the 1940 generation teaches us the value of true diversification. Their portfolios often include a mix of blue-chip stocks, government bonds, real estate, and sometimes even physical gold—assets that provide stability when one sector fails. In an era where digital assets and high-growth tech stocks often dominate the conversation, the diversified, “all-weather” portfolio of a typical 1940-born investor serves as a masterclass in risk management.

In conclusion, “what generation is 1940” is more than just a chronological question; it is an inquiry into a specific type of financial legacy. The Silent Generation’s 1940 cohort represents a bridge between the old world of pensions and the new world of self-directed investing. By studying their habits of discipline, their strategic use of real estate, and their current approach to estate planning, we gain valuable insights into how to build and preserve wealth across a lifetime.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.