In the world of finance, value is rarely a static number. Whether you are purchasing a first home, refinancing a mortgage, or preparing to sell a mid-sized corporation, the “appraisal” is the ultimate gatekeeper of the transaction. For many, the process feels like a black box—a mysterious expert enters the property or examines the books, and a week later, a number emerges that can either greenlight a dream or halt a deal in its tracks.

Understanding what an appraiser looks at is essential for anyone navigating the “Money” niche, from personal finance enthusiasts to seasoned investors. An appraisal is not merely an opinion; it is a rigorous, data-backed analysis intended to mitigate risk for lenders and ensure fair market value for buyers and sellers. By pulling back the curtain on this process, you can better prepare your assets for scrutiny and maximize their financial potential.

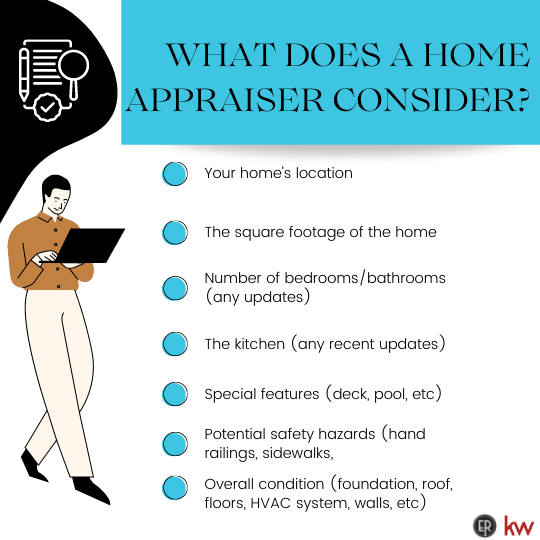

The Anatomy of a Home Appraisal: Physical and Market Factors

In personal finance, your home is likely your largest asset. When a bank prepares to issue a loan, they need to ensure the collateral (the house) is worth the investment. Real estate appraisers follow a standardized protocol to determine this value, focusing on three primary pillars: physical condition, functional utility, and external market influences.

Interior Condition and Structural Integrity

The appraiser begins with the “bones” of the property. They are not looking at your furniture or your choice of paint color, but rather the quality of the construction and the state of the home’s systems. They will inspect the foundation for cracks, the roof for signs of aging, and the attic for proper insulation.

Crucially, they look at the “big ticket” items: the HVAC system, plumbing, and electrical panels. A home with a brand-new energy-efficient furnace will be valued higher than one with a 30-year-old unit on its last legs. Furthermore, they evaluate the materials used—hardwood floors generally hold more value than laminate, and quartz countertops are weighed more heavily than formica. They also check for safety compliance, such as functioning smoke detectors and the absence of lead-based paint or asbestos in older structures.

The Power of Comparable Sales (The “Comps”)

No property exists in a vacuum. One of the most critical things an appraiser looks at is what similar properties in your immediate area have sold for in the last six months. This is known as the Sales Comparison Approach.

The appraiser selects 3–5 “comps”—homes of similar square footage, age, and style within a tight radius (usually one mile). They then make “adjustments” based on differences. If a neighbor’s house sold for $500,000 but had a finished basement and yours does not, the appraiser will subtract the estimated value of a finished basement from your home’s valuation. Understanding this helps homeowners realize that over-improving a house beyond the neighborhood standard often yields a poor return on investment.

Location and Neighborhood Trends

In real estate, the adage “location, location, location” is quantified by the appraiser. They look at the proximity to “nuisances” versus “amenities.” Is the house backed up against a loud highway or a serene public park? Is it within a high-ranking school district?

They also analyze broader economic trends. Is the neighborhood experiencing a revitalization with new businesses moving in, or is there a high rate of foreclosure and abandoned properties? These external factors can create a “valuation ceiling” that even the most beautiful interior renovations cannot break.

Beyond the Building: What Appraisers Look for in Business Valuation

While real estate appraisals are common, business appraisals are the cornerstone of corporate finance and entrepreneurship. Whether for a merger, acquisition, or partnership buyout, a business appraiser looks at a company’s ability to generate future wealth. This is far more complex than counting desks and computers; it involves a deep dive into the “intangibles” of the entity.

Financial Statements and Cash Flow

The first things a business appraiser looks at are the historical financial statements—specifically the Balance Sheet, Income Statement, and Cash Flow Statement for the last three to five years. They are looking for consistency and “quality of earnings.”

A business that shows a steady 10% growth year-over-year is often more valuable than one that had a single massive spike followed by a slump. The appraiser will “normalize” the earnings, removing one-time expenses (like a legal settlement) or discretionary spending by the owner (like a company-funded luxury car) to see the true operating profit of the business. This “Sellers Discretionary Earnings” (SDE) or EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) serves as the baseline for the valuation.

Intangible Assets and Intellectual Property

In the modern economy, a company’s physical assets (machinery, inventory) often represent only a fraction of its total value. Appraisers look closely at “Goodwill” and intellectual property. This includes proprietary software, trademarks, patents, and, most importantly, brand recognition.

They also evaluate the “customer concentration” risk. If a business has $10 million in revenue but 80% of that comes from a single client, the appraiser will apply a heavy discount because the risk of financial collapse is high if that client leaves. Conversely, a diversified, loyal customer base and a strong, recurring subscription model significantly drive up the appraisal value.

Industry Outlook and Competitive Moat

The appraiser acts as a market analyst, looking at the industry’s lifecycle. Is the business in a sunset industry (like traditional print media) or a sunrise industry (like renewable energy)? They look for the “competitive moat”—the unique advantage that protects the business from competitors. This could be a strategic location, a secret recipe, or a specialized workforce with high barriers to entry. A business that is easy to replicate will always receive a lower valuation than one with a “protected” market position.

Methodology and the “Why” Behind the Numbers

To maintain professional integrity and satisfy financial regulators, appraisers don’t just pick a number; they follow specific mathematical methodologies. Understanding these frameworks helps you see the logic behind their final report.

The Three Common Approaches to Value

Appraisers generally utilize one of three frameworks, or a combination thereof, to reach a conclusion:

- The Cost Approach: This calculates how much it would cost to replace the asset from scratch today, minus depreciation. This is often used for unique properties or new constructions where “comps” are unavailable.

- The Income Approach: Primarily used for investment properties and businesses, this calculates value based on the net income the asset generates. It uses a “capitalization rate” to convert future income into a present-day lump sum.

- The Market Approach: As discussed with “comps,” this relies on the principle of substitution—that a buyer will not pay more for an asset than the cost of an equivalent substitute in the open market.

Objectivity and Compliance Standards

In the United States, appraisers must adhere to the Uniform Standards of Professional Appraisal Practice (USPAP). This is a critical point for anyone in the money niche to understand: the appraiser is a neutral third party. They do not work for the buyer or the seller; they work for the “transaction.”

When an appraiser looks at an asset, they are looking for “Market Value,” which is defined as the most probable price an asset should bring in a competitive and open market under all conditions requisite to a fair sale. They must remain unbiased by the emotional attachments of the seller or the high-pressure timelines of a mortgage broker.

How to Maximize the Outcome of an Appraisal

If you are on the selling or borrowing side of an appraisal, you are not a passive observer. While you cannot (and should not) influence the appraiser’s professional judgment, you can ensure they have the most accurate and positive data set to work with.

Documenting Improvements and Maintenance

One of the biggest mistakes people make is assuming the appraiser will “see” all the hard work put into an asset. Whether it’s a home or a business, you should provide a comprehensive “Portfolio of Value.” For a home, this includes a list of all capital improvements (new roof, upgraded electrical, landscaping) with dates and receipts. For a business, this includes documented SOPs (Standard Operating Procedures), updated equipment lists, and proof of a clean environmental or legal record. Providing this documentation ensures the appraiser doesn’t overlook hidden value.

Presenting Clean and Transparent Financials

In business and investment property appraisals, “opacity is the enemy of value.” If your books are a mess or your rental income is “under the table,” an appraiser cannot include that income in their valuation. To get the highest appraisal, your financial records should be audited or at least professionally reviewed. Clear, transparent reporting reduces the “risk premium” an appraiser might otherwise apply, directly resulting in a higher valuation.

Conclusion

Whether it is the bricks and mortar of a family home or the complex cash flows of a global enterprise, the question of “what does an appraiser look at” boils down to three things: Risk, Utility, and Comparison.

An appraiser looks for anything that threatens the longevity of the asset (risk), the benefits the asset provides to its owner (utility), and how the asset stacks up against the rest of the world (comparison). By understanding these financial levers, you can make smarter investment decisions, prepare your assets for the market, and navigate the complex world of personal and business finance with confidence. In the end, a high appraisal isn’t just about the number—it’s a validation of sound financial management and strategic growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.