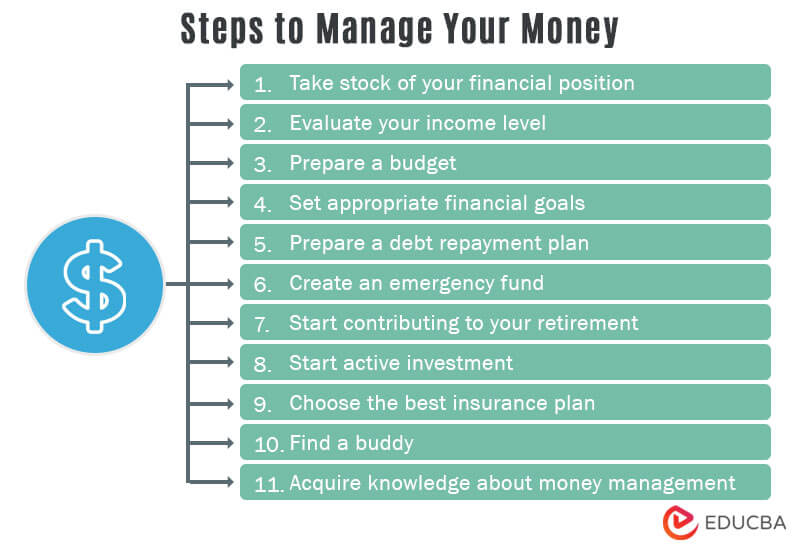

Managing money is often perceived as a daunting task involving complex spreadsheets and restrictive sacrifices. However, at its core, effective financial management is less about rigid mathematics and more about intentional behavior and strategic planning. Whether you are looking to crawl out of debt, build a robust investment portfolio, or simply gain peace of mind regarding your monthly expenses, understanding the mechanics of money is the first step toward true financial independence.

In today’s volatile economic landscape, the ability to manage your capital is a vital life skill. It requires a balance between living for today and securing your tomorrow. This guide explores the foundational pillars of personal finance, providing a roadmap to transform your relationship with money from one of stress to one of empowerment.

The Architectural Blueprint: Building a Sustainable Budget

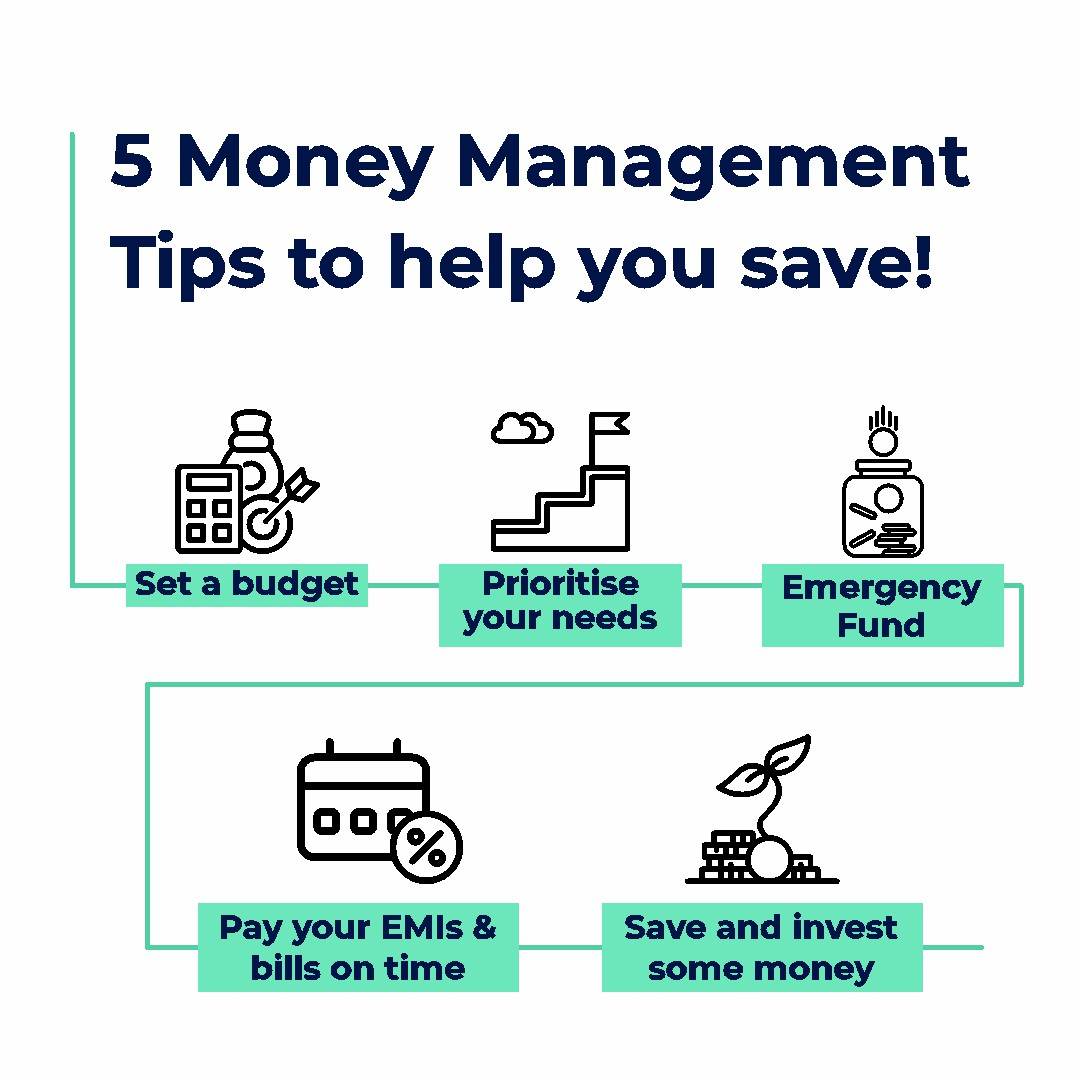

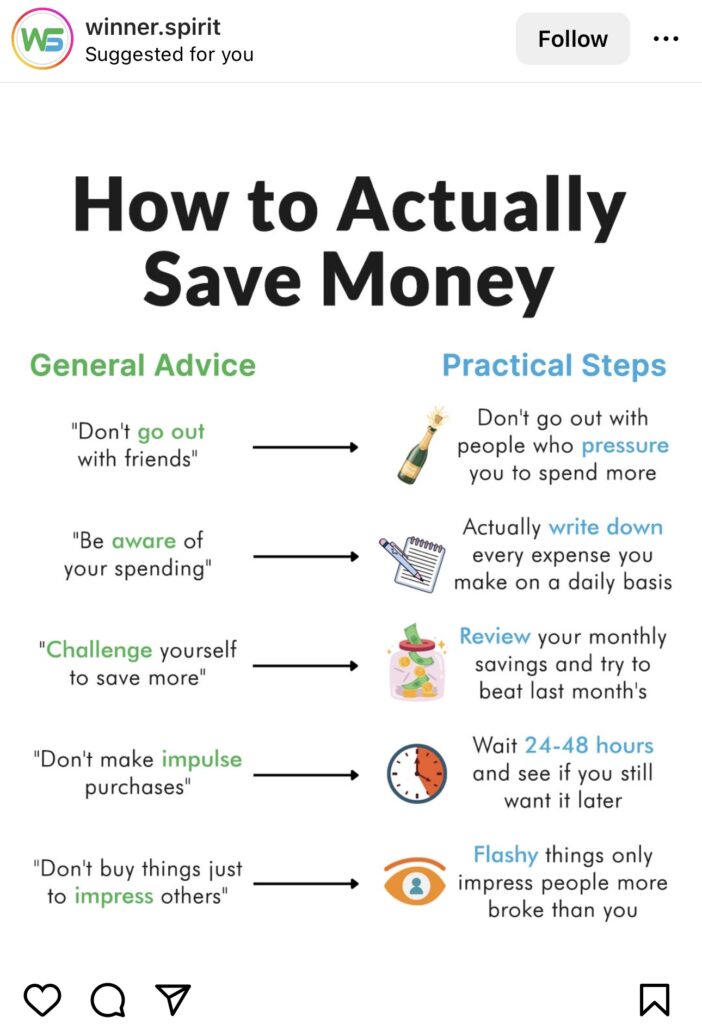

The foundation of any successful financial plan is the budget. Many people view a budget as a “financial diet” that limits their freedom, but in reality, a budget is a tool that gives you permission to spend on the things that truly matter to you. Without a map, you are likely to drift into impulse purchases and “lifestyle creep,” where your expenses rise to meet every salary increase.

Choosing the Right Budgeting Framework

There is no one-size-fits-all approach to budgeting. The key is to find a system that aligns with your personality. One of the most popular and effective methods is the 50/30/20 Rule. Under this framework, 50% of your after-tax income goes toward “Needs” (housing, utilities, groceries), 30% toward “Wants” (dining out, hobbies, streaming services), and 20% toward “Financial Goals” (debt repayment and savings).

For those who prefer a more granular approach, Zero-Based Budgeting is highly effective. This method requires you to “give every dollar a job” before the month begins. If you earn $4,000, your expenses, savings, and debt payments must equal exactly $4,000. This ensures that no money is “leaked” through mindless spending.

Leveraging Financial Tools for Tracking

Manual tracking is a noble endeavor, but technology has made it easier than ever to maintain oversight. Utilizing financial management software or apps allows you to sync your bank accounts and categorize transactions in real-time. By reviewing these categories monthly, you can identify “spending leaks”—those small, recurring subscriptions or habits that seem insignificant individually but aggregate into substantial annual costs. The goal is not to eliminate joy, but to ensure that your spending reflects your actual priorities.

Defensive Strategies: Debt Management and Emergency Funds

Before you can focus on offensive moves like investing, you must secure your defensive line. Financial stability is built on the ability to weather storms without falling into high-interest debt. This requires a two-pronged approach: eliminating existing high-cost liabilities and creating a buffer for the future.

High-Interest Debt Repayment Tactics

Not all debt is created equal. High-interest debt, particularly from credit cards, is a financial emergency. With interest rates often exceeding 20%, these balances can compound faster than your ability to pay them off.

Two primary strategies are widely recognized for debt elimination: the Debt Snowball and the Debt Avalanche. The Snowball method focuses on psychological wins by paying off the smallest balances first, creating momentum. The Avalanche method focuses on mathematical efficiency by targeting the debt with the highest interest rate first, regardless of the balance. Whichever method you choose, consistency is the determining factor in your success.

The Essential Emergency Fund

Life is unpredictable. Medical emergencies, car repairs, or sudden job losses are not “if” scenarios; they are “when” scenarios. An emergency fund acts as a financial shock absorber. Most experts recommend saving three to six months’ worth of essential living expenses in a high-yield savings account (HYSA). This liquidity ensures that when a crisis occurs, you can handle it with cash rather than resorting to credit cards, which would only exacerbate the problem.

Wealth Acceleration: The Power of Investing and Compounding

Once your high-interest debt is gone and your emergency fund is established, the focus shifts to wealth creation. Saving is defensive; investing is offensive. To keep pace with inflation and build a retirement nest egg, you must put your money to work in assets that appreciate over time.

Understanding Asset Allocation and Risk

Investing is not gambling; it is the calculated purchase of assets that have a high probability of growth. The most common vehicles are stocks, bonds, and real estate. Diversification is the golden rule here. By spreading your investments across various sectors and asset classes, you reduce the risk of a single market downturn wiping out your portfolio.

For the average individual, low-cost Index Funds or ETFs (Exchange-Traded Funds) are often the most effective route. These funds allow you to own a small piece of hundreds or thousands of companies, capturing the overall growth of the market without the high risk of picking individual stocks.

The Magic of Compounding and Time

The most powerful force in finance is compound interest. Albert Einstein famously called it the “eighth wonder of the world.” Compounding occurs when the returns on your investments begin to earn their own returns. The earlier you start, the more “heavy lifting” time does for you.

For example, an individual who starts investing $500 a month at age 25 will likely have significantly more wealth at age 65 than someone who starts investing $1,500 a month at age 45. Managing money effectively means recognizing that time is your greatest asset—an asset that cannot be replenished once spent.

Expanding the Horizon: Income Generation and Side Hustles

While cutting expenses is a vital component of money management, there is a floor to how much you can save. Conversely, there is theoretically no ceiling to how much you can earn. To accelerate your path to financial freedom, you must look at ways to increase the “top line” of your personal income statement.

Scaling Personal Expertise and Side Income

In the modern economy, the traditional 9-to-5 is often just one component of a broader income strategy. Leveraging your professional skills through freelancing or consulting can provide a significant boost to your monthly cash flow. Whether it is graphic design, writing, tutoring, or technical consulting, selling your expertise allows you to trade time for high-value compensation.

Developing Passive Income Streams

The ultimate goal of money management is to reach a point where your money earns enough to cover your lifestyle without you having to work. This is the definition of “Financial Independence.” Beyond traditional stock market dividends, other passive income streams include rental properties, peer-to-peer lending, or creating digital products like online courses or e-books. These require a significant upfront investment of either time or capital, but they provide ongoing returns that decouple your income from your hours worked.

Future-Proofing: Protection and Estate Planning

The final pillar of managing money is protection. It is not enough to build wealth; you must protect it from lawsuits, accidents, and the inevitability of death. This ensures that your financial legacy remains intact and that your loved ones are provided for.

The Role of Insurance as a Financial Safety Net

Insurance is often overlooked in discussions about “making money,” but it is a critical component of a professional financial plan. Health insurance, disability insurance, and life insurance are essential to prevent a single catastrophic event from bankrupting your household. For those with significant assets, umbrella insurance provides an extra layer of liability protection. View insurance premiums not as an expense, but as a “hedge” against the loss of your greatest asset: your ability to earn an income.

Long-Term Planning and Tax Efficiency

Finally, managing money involves looking decades ahead. This includes understanding the tax implications of your investments. Utilizing tax-advantaged accounts like a 401(k), 403(b), or an IRA (Individual Retirement Account) can save you hundreds of thousands of dollars in taxes over your lifetime.

Additionally, basic estate planning—such as creating a will or a trust—ensures that your assets are distributed according to your wishes. It minimizes the legal burden on your heirs and ensures that the wealth you worked so hard to build continues to serve a purpose long after you are gone.

Conclusion: The Journey to Financial Mastery

Managing money is a marathon, not a sprint. It is a continuous process of evaluation, adjustment, and discipline. By establishing a clear budget, eliminating high-interest debt, investing for the future, and protecting your assets, you create a fortress of financial security.

The goal of mastering your finances is not merely to accumulate digits in a bank account. Rather, it is to gain the freedom to make choices—to work a job you love, to travel, to support causes you care about, and to live a life unburdened by the weight of financial uncertainty. Start small, stay consistent, and remember that the best time to start managing your money was yesterday; the second best time is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.