In the intricate world of business finance, few terms are as fundamental yet frequently misunderstood as “gross payroll.” For business owners, it represents the single largest line item on the balance sheet. For employees, it is the figure that defines their market value, even if it isn’t the amount that ultimately hits their bank account. Understanding gross payroll is not merely an exercise in accounting; it is a critical component of fiscal health, tax compliance, and strategic financial planning.

At its core, gross payroll is the total amount of money a company owes its employees before any deductions, taxes, or withholdings are taken out. It is the starting point of the compensation cycle and the baseline for calculating a company’s true labor costs. To manage a business effectively—or to manage one’s personal finances as an employee—one must master the nuances of how this figure is derived, reported, and utilized.

Defining Gross Payroll: The Foundation of Business Compensation

Gross payroll serves as the “raw” total of employee compensation. It is the cumulative sum of all wages, salaries, and additional earnings processed through the payroll system during a specific pay period. While it is often discussed in terms of individual “gross pay,” for a business, gross payroll is the aggregate figure that reflects the organization’s total commitment to its workforce.

The Difference Between Gross Pay and Net Pay

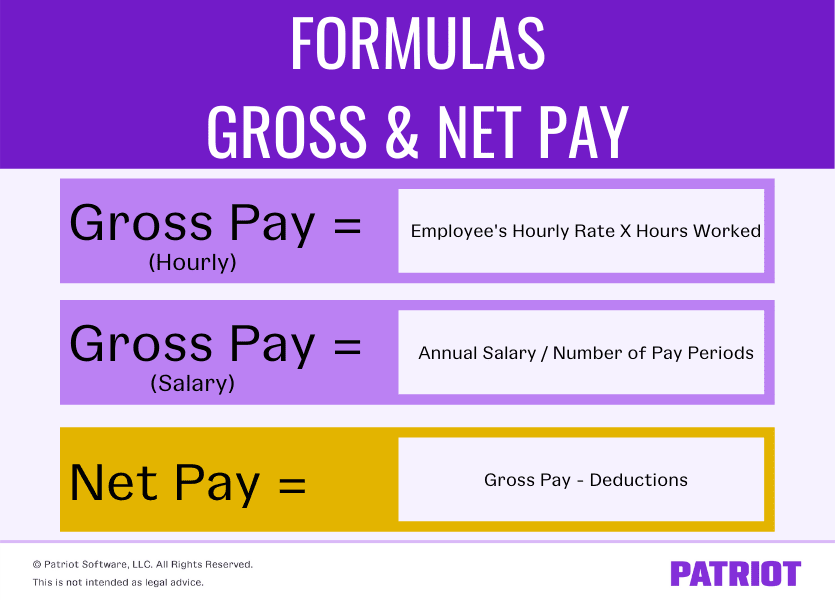

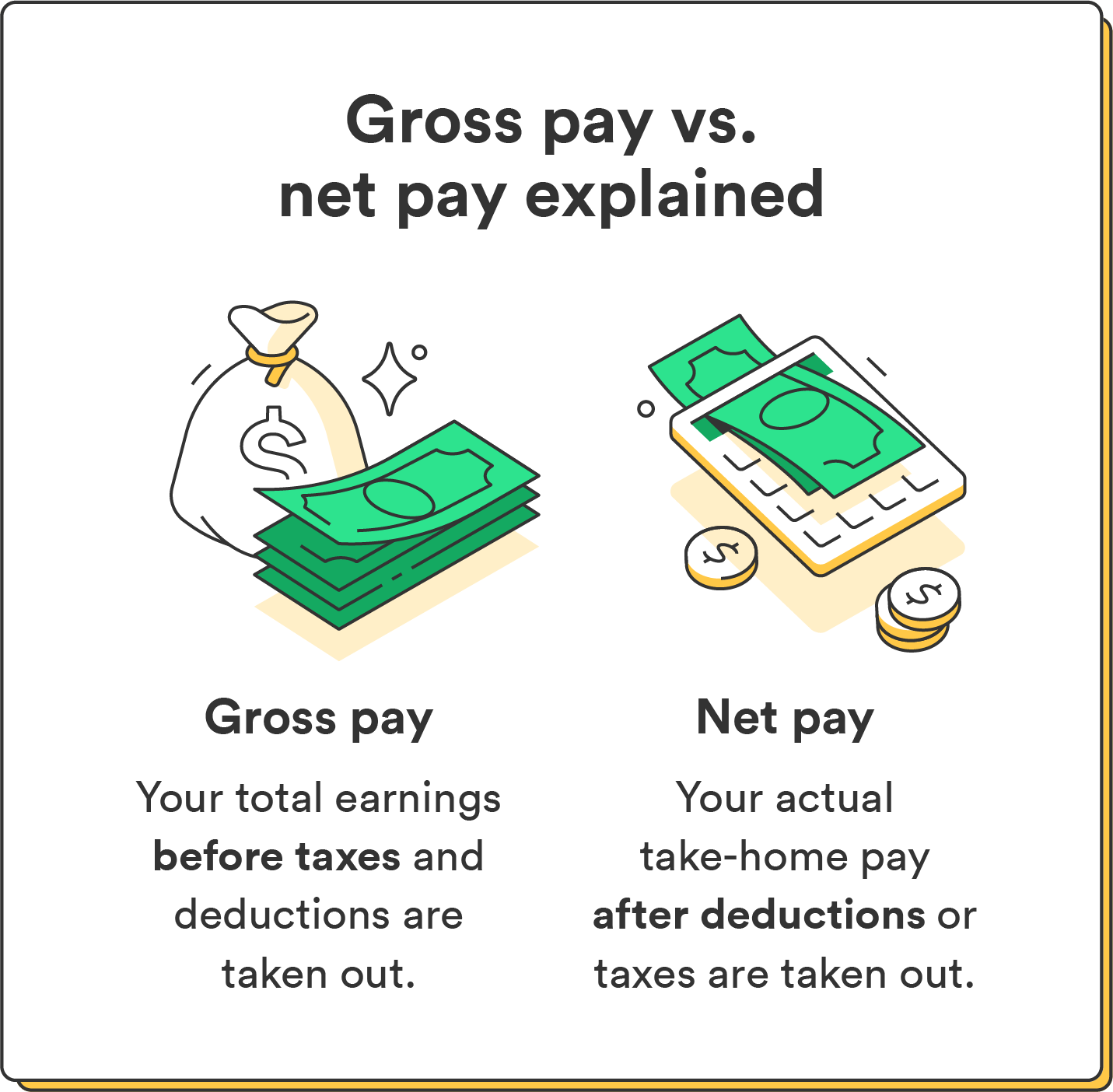

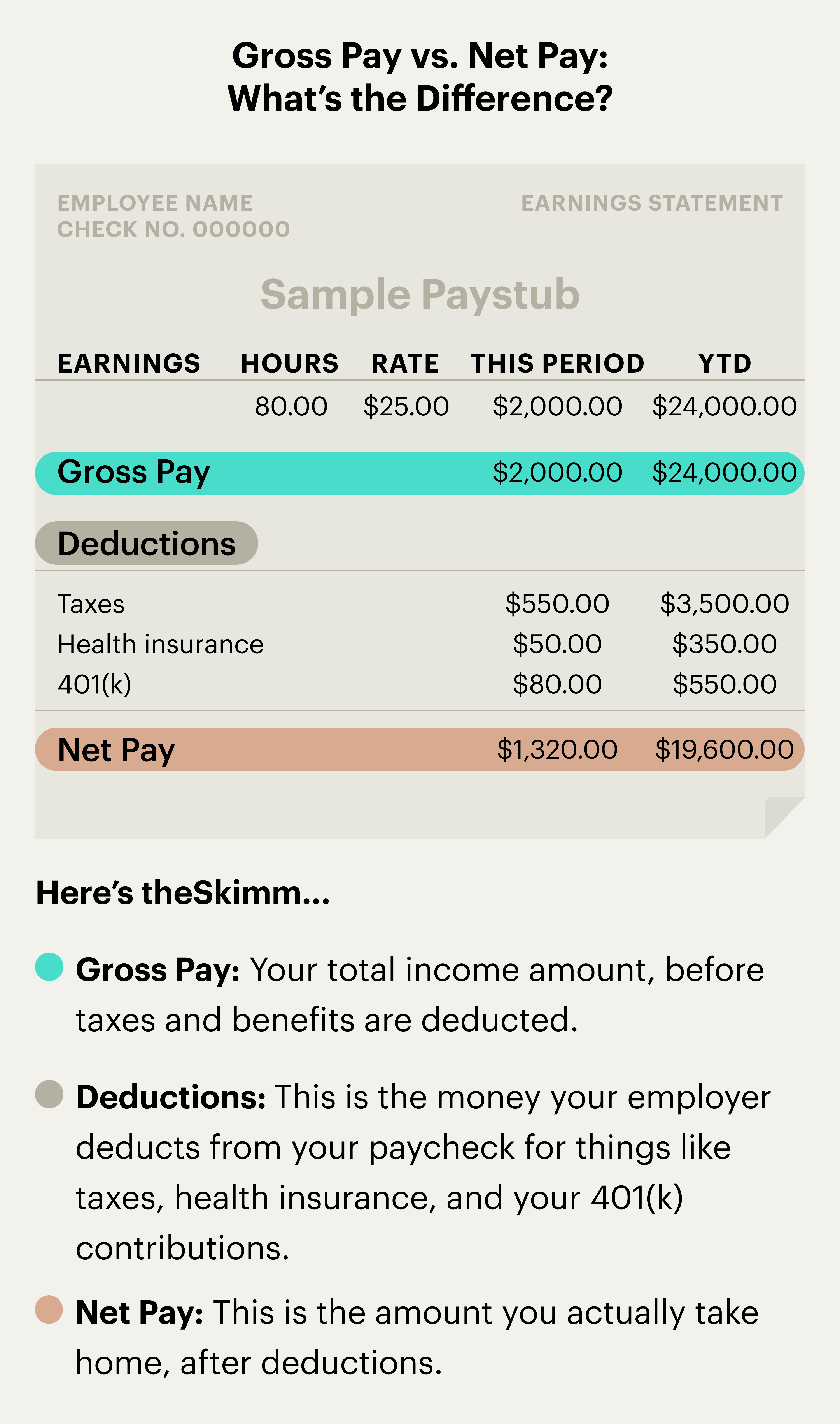

The most common point of confusion for those new to finance is the distinction between gross pay and net pay. Gross pay is the “top-line” number—the amount agreed upon in an employment contract or offer letter. Net pay, conversely, is the “bottom-line” number, or “take-home pay.”

To arrive at net pay, several layers of subtractions must occur. These include mandatory statutory deductions such as federal, state, and local income taxes, as well as Social Security and Medicare contributions (FICA). Furthermore, voluntary deductions—such as premiums for health insurance, contributions to 401(k) plans, or life insurance—are subtracted from the gross amount. Understanding this gap is essential for employees budgeting their monthly expenses and for employers explaining compensation packages to their staff.

Why Understanding Gross Payroll Matters for Employers

For an employer, gross payroll is the metric used to determine several critical financial obligations. Most business taxes are calculated as a percentage of gross payroll. If an employer miscalculates the gross amount, every subsequent calculation—including tax remittances to the IRS—will be incorrect, potentially leading to audits and heavy penalties.

Moreover, gross payroll is a key indicator of a company’s “burn rate” and operational efficiency. In many industries, particularly service-based sectors, gross payroll should ideally sit within a specific percentage of total revenue. Monitoring this figure allows business owners to make informed decisions about hiring, scaling, or implementing cost-saving measures.

Components of Gross Payroll: More Than Just a Base Salary

A common misconception is that gross payroll only includes an employee’s base salary or hourly rate. In reality, gross payroll is a comprehensive “bucket” that holds various forms of compensation. To maintain accurate books, a business must account for every dollar of value provided to the employee.

Hourly Wages and Salaried Compensation

The two primary building blocks of gross payroll are hourly wages and salaries.

- Salaried Employees: These individuals are typically paid a fixed annual amount divided by the number of pay periods in a year. Their gross pay remains consistent regardless of the number of hours worked, provided they meet the criteria for “exempt” status under labor laws.

- Hourly Employees: Their gross pay is calculated by multiplying the total hours worked during the pay period by their agreed-upon hourly rate. This requires meticulous time-tracking to ensure accuracy.

Overtime, Bonuses, and Commissions

Beyond the base pay, gross payroll includes supplemental income.

- Overtime: Under the Fair Labor Standards Act (FLSA), non-exempt employees must be paid time-and-a-half for any hours worked over 40 in a workweek. These overtime premiums are a significant component of gross payroll in industries like manufacturing or healthcare.

- Bonuses: Whether it is a holiday bonus, a performance-based incentive, or a signing bonus, these are all considered taxable income and must be included in the gross payroll total.

- Commissions: For sales-driven organizations, commissions form a substantial portion of the gross payroll. These are often variable and must be calculated based on specific sales targets achieved during the period.

Fringe Benefits and Reimbursements

Certain benefits are also factored into gross payroll if they are considered “taxable fringes.” This might include the value of a company car used for personal travel or certain types of educational assistance. However, it is important to distinguish these from non-taxable reimbursements (like travel expenses), which are generally not included in gross payroll because they are not considered earned income.

Calculating Gross Payroll: A Step-by-Step Financial Process

Calculating gross payroll requires a systematic approach to ensure that both the employee is paid fairly and the government receives the correct tax data. While modern software automates much of this, understanding the manual calculation is vital for auditing purposes.

The Standard Calculation Formula

For an hourly employee, the formula is:

(Regular Hours × Hourly Rate) + (Overtime Hours × Overtime Rate) + Bonuses + Commissions = Gross Pay.

For a salaried employee, the formula is:

(Annual Salary / Number of Pay Periods) + Bonuses + Commissions = Gross Pay.

By aggregating these individual totals, a business arrives at its total gross payroll for the period.

Handling Deductions and Withholdings

Once the gross payroll is established, the process of “withholding” begins. This is where the employer acts as an agent for the government. They must calculate the correct amount of federal income tax based on the employee’s W-4 form, along with state and local taxes. Additionally, the employee’s share of FICA (7.65% for Social Security and Medicare) is withheld from the gross pay.

It is a common error to think these deductions reduce the employer’s gross payroll expense; they do not. The employer is still paying the full gross amount; they are simply diverting a portion of it to the tax authorities on the employee’s behalf.

Employer-Side Payroll Taxes (FICA, FUTA, and SUTA)

A critical distinction in business finance is the difference between “Gross Payroll” and “Total Labor Burden.” While gross payroll is the amount paid to or on behalf of the employee, the employer has additional costs.

Employers must match the employee’s FICA contribution (an additional 7.65%). They must also pay Federal Unemployment Tax (FUTA) and State Unemployment Tax (SUTA). When a business owner looks at their gross payroll, they must remember that their actual cash outflow will be roughly 10% to 20% higher once these employer-side taxes and benefits are included.

The Strategic Importance of Gross Payroll in Business Finance

Gross payroll is not just a backward-looking reporting figure; it is a forward-looking strategic tool. In the realm of personal finance and business management, these numbers dictate the viability of the enterprise.

Budgeting and Cash Flow Management

For most small to medium-sized enterprises (SMEs), payroll is the largest recurring cash outflow. By analyzing historical gross payroll data, a CFO or business owner can forecast future cash flow needs. This is particularly important for seasonal businesses that may need to increase their gross payroll during peak months. Understanding the “gross” figure allows for more accurate budgeting than looking at “net” figures, as the gross figure represents the total liability.

Compliance, Auditing, and Reporting

The IRS and state tax agencies view gross payroll as the definitive record of a company’s tax liability. Inaccurate reporting of gross payroll is a primary trigger for corporate audits. Furthermore, workers’ compensation insurance premiums are often calculated based on a percentage of the total gross payroll. If a business underreports its gross payroll, it may find itself underinsured or facing massive “true-up” premiums at the end of the year.

Using Payroll Software to Automate Calculations

In the modern financial landscape, manual payroll calculation is increasingly rare and risky. Using specialized financial tools and payroll software ensures that the transition from gross pay to net pay is handled with mathematical precision. These tools automatically update for changes in tax laws, calculate complex overtime across different jurisdictions, and generate the necessary reports for tax filing, thereby protecting the business’s financial integrity.

Common Challenges and Best Practices in Payroll Management

Managing gross payroll is fraught with potential pitfalls, ranging from simple clerical errors to complex legal misclassifications. Mastering this area requires a commitment to detail and an understanding of labor law.

Avoiding Costly Misclassification Errors

One of the most expensive mistakes a business can make is misclassifying an employee as an independent contractor. Independent contractors are not part of gross payroll; they are paid gross amounts via 1099, and the business does not withhold taxes. However, if the IRS determines these individuals should have been classified as employees, the business may be held liable for all back taxes, interest, and penalties based on what the gross payroll should have been.

Staying Current with Changing Tax Laws

Tax thresholds, Social Security wage caps, and state unemployment rates change frequently. A professional approach to business finance requires staying informed about these shifts. For instance, the Social Security wage base limit—the maximum amount of gross pay subject to the tax—is adjusted annually. High-earning employees may hit this cap mid-year, which changes the calculation of their deductions for the remainder of the fiscal year.

In conclusion, gross payroll is the heartbeat of a company’s financial operations. It is the starting point for employee satisfaction, the baseline for tax compliance, and a primary indicator of organizational health. By understanding the components, calculations, and strategic implications of gross payroll, business owners can ensure their enterprise remains solvent, compliant, and poised for growth in an ever-evolving economic landscape.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.