In the global financial landscape, the term “Islamic Finance” is often used to describe a multi-trillion-dollar industry that operates on a unique set of ethical and legal parameters. When we ask “what does Islam mean” in the context of the money niche, we are not just discussing a religious identity, but a comprehensive economic framework designed to promote equity, risk-sharing, and social justice. For the modern investor, entrepreneur, or personal finance enthusiast, understanding these principles offers a roadmap to a resilient and ethical way of building wealth.

Unlike conventional finance, which often prioritizes profit maximization at any cost, Islamic finance views money as a tool for trade and value creation rather than a commodity in itself. This distinction changes everything—from how we save and invest to how we manage debt and run businesses.

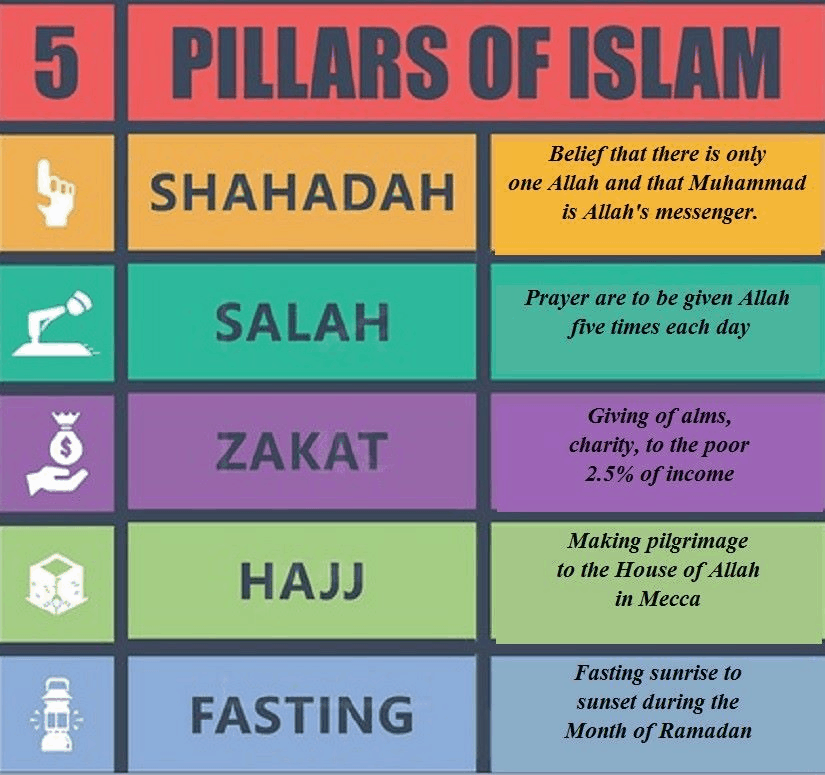

Understanding the Pillars: The Core Principles of Islamic Finance

To understand what it means to manage money under Islamic principles, one must first look at the foundational prohibitions and requirements that define the “Halal” (permissible) financial landscape. These are not merely restrictive rules; they are safeguards intended to prevent exploitation and systemic instability.

The Prohibition of Riba (Interest)

The most well-known aspect of Islamic finance is the strict prohibition of Riba, commonly translated as usury or interest. In this context, money is viewed as a medium of exchange, not an asset that can generate more money through the passage of time alone. Therefore, lending money to receive more money in return is considered exploitative. For the modern consumer, this means that traditional savings accounts that pay interest or credit cards that charge it are fundamentally incompatible with this framework. Instead, the system encourages profit-and-loss sharing (PLS) arrangements.

Avoiding Gharar (Uncertainty) and Maysir (Gambling)

Gharar refers to excessive uncertainty or deceit in a contract. In the money niche, this principle discourages “naked” short-selling, complex derivatives, and any transaction where the outcome is purely speculative or the terms are dangerously ambiguous. Similarly, Maysir (gambling) is prohibited. This extends beyond the casino floor into the financial markets, targeting speculative day trading or “get-rich-quick” schemes where wealth is acquired by chance rather than through productive economic activity.

Ethical and Social Responsibility in Asset Allocation

A major component of Islamic money management is the concept of Halal and Haram (forbidden) sectors. An investor cannot put their capital into businesses that deal in alcohol, tobacco, weapons, conventional banking, or gambling. This pre-dates the modern “ESG” (Environmental, Social, and Governance) movement but shares many of its goals. It ensures that wealth creation does not come at the expense of societal well-being.

Sharia-Compliant Investing: Building a Wealth Portfolio

For the modern investor, the question of “what does Islam mean” translates into practical screening processes. Building a portfolio that aligns with these values requires more than just avoiding “sin stocks”; it requires a deep dive into the financial health and operational nature of every company involved.

Halal Stocks and the Screening Process

Since most public companies operate within the conventional interest-based system to some degree, Islamic scholars and financial bodies (like AAOIFI) have established quantitative filters. To be considered a “Halal” stock, a company must pass two tests:

- The Business Activity Screen: The primary source of revenue must not come from prohibited sectors (e.g., conventional insurance or pork production).

- The Financial Ratio Screen: This limits the amount of interest-bearing debt a company can carry and the amount of interest income it can earn. Generally, a company’s debt-to-market-capitalization ratio must remain below 33%. This encourages investing in companies with strong balance sheets and real tangible assets.

Sukuk: The Islamic Alternative to Bonds

In the conventional world, bonds are debt instruments where the issuer pays the holder interest. In Islamic finance, this is replaced by Sukuk. Rather than being a debt obligation, a Sukuk represents partial ownership in a tangible asset, project, or investment activity. The “interest” is replaced by a share of the profit generated by that asset. This links the financial return directly to the performance of the real economy, reducing the risk of “bubbles” built on paper debt.

Real Estate and Tangible Asset Management

Real estate is often the cornerstone of an Islamic financial plan because it involves tangible assets and rental income, which is considered a legitimate form of profit. Managing a real estate portfolio within this niche involves avoiding conventional mortgages. Instead, many turn to “Diminishing Musharaka” models, where the bank and the buyer co-own the property, and the buyer gradually buys out the bank’s share while paying a fee for the use of the bank’s portion of the home.

Modern Money Tools: FinTech and Islamic Banking

The rise of financial technology (FinTech) has revolutionized how we understand what Islam means for the 21st-century wallet. It has bridged the gap between ancient ethical codes and the digital-first lifestyle of modern users.

Digital Banking and Neo-Banks for the Modern Muslim

A new wave of digital-only banks—often called “Neo-Banks”—has emerged to cater specifically to the Islamic market. These apps offer interest-free spending accounts, automated “rounding up” for charity, and real-time Halal stock screening. By removing the overhead of physical branches, these tech-driven tools provide a more transparent and cost-effective way for users to keep their money separate from interest-bearing systems.

Robo-Advisors and Automated Sharia-Compliant Portfolios

For those who are not financial experts, the “Money” aspect of Islamic life has become much simpler through Robo-advisors. These AI-driven platforms automatically build and rebalance portfolios based on Sharia-compliant ETFs (Exchange-Traded Funds). They use algorithms to ensure that the debt-to-equity ratios are always within the permissible limits, allowing individuals to grow their wealth passively while remaining confident in their ethical compliance.

Personal Finance and Side Hustles: Earning a Halal Living

The niche of money isn’t just about where you store your wealth; it’s about how you earn it. Whether through a primary career or a side hustle, the Islamic framework demands integrity and value-adding activities.

Navigating the Gig Economy Ethically

In the age of freelancing and side hustles, “what does Islam mean” for an earner? It means ensuring that every contract is clear (avoiding Gharar) and that the services provided are beneficial. A Halal side hustle might involve tech consulting, e-commerce, or creative design, provided the end product is ethical. It also emphasizes the prompt payment of workers—a famous principle states that a worker should be paid before their sweat dries.

Zakat and Sadaqah: The Financial Purification Process

Personal finance in this context is never complete without discussing Zakat. This is a mandatory 2.5% annual contribution on qualifying wealth (savings, gold, investments) to be given to those in need. In the money niche, Zakat is viewed as a “purification” of capital. It ensures that wealth does not stagnate among a few individuals but circulates back into the economy to support the vulnerable. Beyond Zakat is Sadaqah (voluntary charity), which acts as a powerful tool for social impact investing.

The Future of Islamic Finance in the Global Economy

The principles of Islamic finance are increasingly being recognized as a viable alternative to the boom-and-bust cycles of the conventional financial world. Because the system prohibits excessive leverage and requires a link to real-world assets, it offers a level of stability that is attractive even to non-Muslim investors seeking “Ethical Finance.”

The convergence of Islamic money principles with modern technology and global brand strategy has created a robust ecosystem. From green Sukuk (bonds for environmental projects) to blockchain-based smart contracts that eliminate ambiguity, the niche of Islamic money is expanding rapidly.

Ultimately, what “the Islam” means in terms of money is a commitment to a higher standard of accountability. It is an acknowledgment that financial success is not measured solely by the balance in a bank account, but by the integrity of the methods used to acquire it and the positive impact that wealth has on the community at large. By prioritizing trade over usury and equity over exploitation, this financial framework offers a timeless and sustainable approach to the complexities of the modern economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.