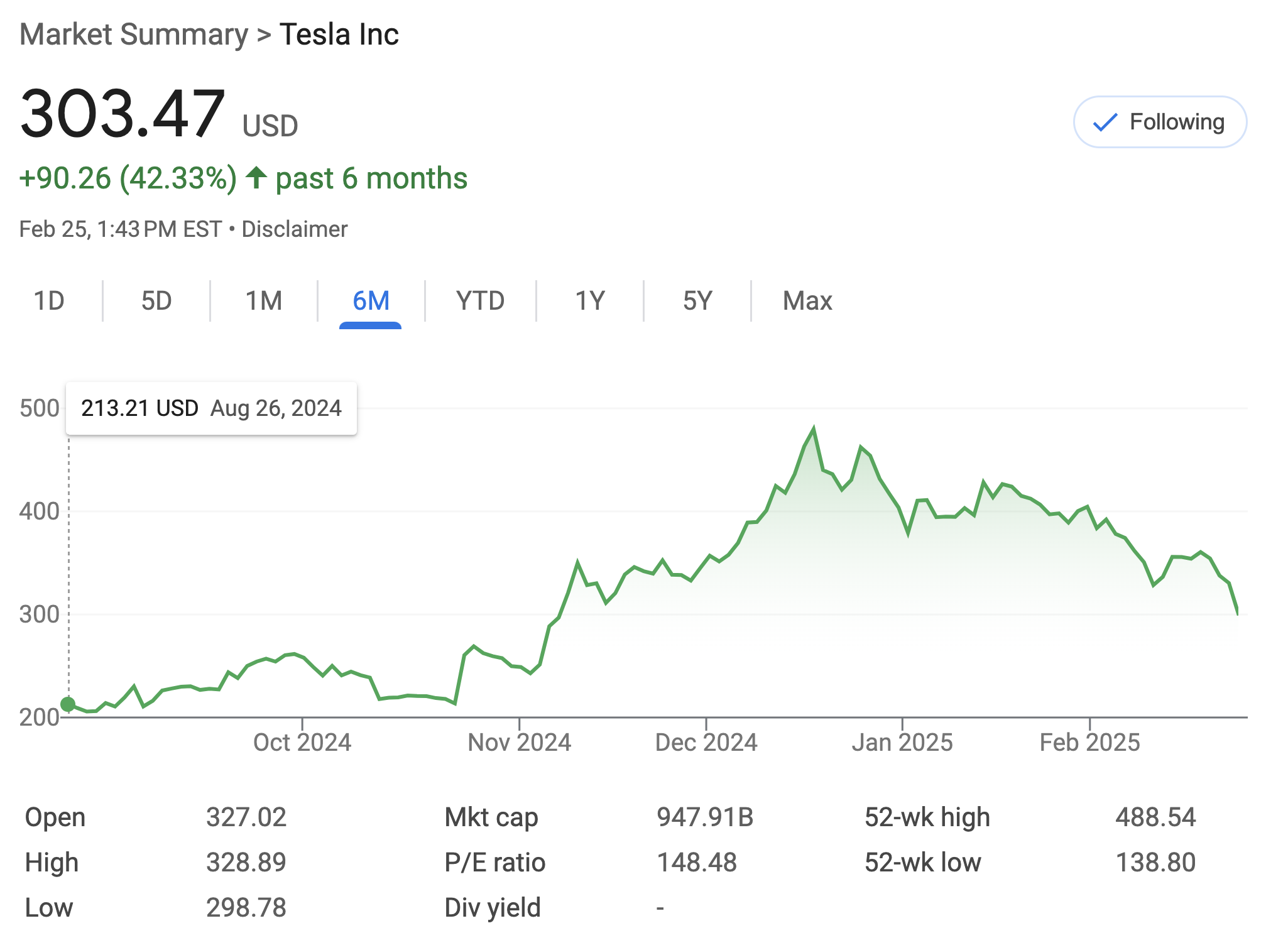

Tesla, Inc. (TSLA) has long been the poster child for the modern growth stock. For years, it defied the gravity of traditional automotive valuations, trading more like a high-growth software company than a manufacturer of heavy machinery. However, the market’s relationship with Tesla has entered a more cynical phase. When investors ask “why is Tesla stock down today,” the answer is rarely a single event. Instead, it is typically a confluence of macroeconomic pressures, fundamental shifts in the electric vehicle (EV) landscape, and a re-evaluation of the “Elon Musk premium.”

To understand the downward pressure on Tesla’s share price, one must look past the daily tickers and analyze the underlying financial mechanics that drive institutional and retail selling.

Macroeconomic Pressures and the High-Interest Rate Environment

The most pervasive headwind facing Tesla today is not unique to the company, but it affects Tesla more acutely than most. As a high-beta growth stock, Tesla’s valuation is heavily dependent on future cash flows. When interest rates are high, the “discount rate” applied to those future earnings increases, making the stock less valuable in the present day.

The Impact of Federal Reserve Policy

The Federal Reserve’s “higher-for-longer” stance on interest rates has a dual-edged effect on Tesla. First, there is the valuation compression mentioned above. Second, there is the practical impact on the consumer. The vast majority of vehicles are purchased via financing. As interest rates rise, the monthly payment for a Model 3 or Model Y increases significantly, even if the sticker price remains the same. To maintain demand, Tesla has been forced to slash prices, which directly eats into the company’s once-envied operating margins. Investors hate seeing margins contract, as it signals that the company is losing its “price-setting” power.

Shifting Capital from Growth to Value

In periods of economic uncertainty, institutional investors often rotate out of high-multiple stocks like Tesla and into defensive sectors or “Value” plays. For much of the last decade, there was “No Alternative” (TINA) to stocks for generating returns. Today, with Treasury bonds offering meaningful yields, the risk-reward profile of holding a volatile stock like Tesla—which trades at a significantly higher Price-to-Earnings (P/E) ratio than the rest of the auto industry—becomes harder for fund managers to justify.

Fundamental Headwinds: Margins, Competition, and Delivery Misses

For a long time, the narrative surrounding Tesla was one of infinite demand and limited supply. That narrative has flipped. Today, the primary concern for the “Money” side of the house is whether Tesla can continue to grow its volume without destroying its profitability.

The EV Pricing War and Eroding Profitability

Tesla’s decision to engage in a global price war has been a major catalyst for recent stock declines. While the strategy aims to stifle competitors and gain market share, it has resulted in a “race to the bottom” for margins. In previous years, Tesla boasted industry-leading automotive gross margins of over 25%. Recent quarterly reports have shown these margins dipping toward the mid-teens. When a company’s fundamental profitability narrative changes from “tech-like margins” to “auto-like margins,” the stock price inevitably undergoes a painful correction to reflect that new reality.

Global Competition: The Rise of BYD and Legacy Automakers

The “moat” around Tesla is being tested. In China, the world’s largest EV market, domestic players like BYD, Li Auto, and Xiaomi are producing high-quality vehicles at price points that Tesla struggles to match. BYD, in particular, has challenged Tesla for the title of the world’s top EV seller. Meanwhile, in the West, legacy automakers like Hyundai, Kia, and even Ford have narrowed the technological gap. As consumers have more choices, Tesla’s “cool factor” is no longer enough to sustain a monopoly-like market share, leading to delivery misses that spook the street.

The “Elon Musk Premium” and Key Person Risk

Investing in Tesla has always been, in large part, an investment in Elon Musk. This “Key Person” risk is a significant factor in the stock’s daily volatility. While Musk’s vision built the company, his external activities and governance demands often create friction with the financial community.

Governance Concerns and Distractions

The acquisition of X (formerly Twitter) remains a point of contention for Tesla shareholders. Many institutional investors argue that Musk is distracted, leading to a “governance vacuum” at Tesla. Furthermore, Musk’s public demand for 25% voting control of the company—threatening to build AI and robotics products elsewhere if his demands aren’t met—has introduced a new layer of political and legal risk. For a fiduciary, this kind of unpredictability is a red flag, often leading to “derisking” (selling shares) to avoid potential chaos.

Retail Investor Fatigue

Tesla has historically been supported by an incredibly loyal base of retail investors. However, as the stock has underperformed the broader S&P 500 and the “Magnificent Seven” tech peers over certain stretches, that loyalty is being tested. Retail “fatigue” occurs when the news cycle becomes consistently negative, and the “diamond hands” mentality gives way to capital preservation. When the retail bid disappears, the stock loses its floor, making it more susceptible to short-selling and algorithmic downward pressure.

Technical Analysis and Market Psychology

Beyond the balance sheets and the CEO’s tweets, the stock market is a function of supply and demand. Tesla’s stock often falls because it breaks through critical “support levels” that trigger automated selling.

Support Levels and Momentum Indicators

Technical analysts look at moving averages (like the 50-day and 200-day lines) to determine the health of a stock. When Tesla’s price falls below these key psychological levels, it often triggers “stop-loss” orders from both retail traders and institutional algorithms. This creates a cascading effect: the lower the stock goes, the more “sell” signals are generated, leading to the rapid intraday drops that leave investors asking “why is this happening?”

Institutional Rebalancing and the AI Narrative Shift

There is also the matter of “narrative shift.” For several years, Tesla was valued as an AI and robotics company that just happened to sell cars. However, when the broader market began rallying on AI (driven by NVIDIA and Microsoft), Tesla was often left behind. This is because Wall Street started demanding “AI receipts”—tangible proof of AI revenue. While Tesla’s Full Self-Driving (FSD) and Optimus robot projects hold immense potential, they are still speculative “moonshots” compared to the immediate hardware sales of other AI giants. As capital moves toward companies with immediate AI earnings, Tesla loses its status as the preferred AI play, leading to institutional rebalancing.

Long-Term Outlook: Should Investors Stay the Course?

When Tesla stock is down, it forces a moment of reckoning for every investor: Is this a buying opportunity or a structural decline? To answer this, one must weigh the current financial friction against the long-term potential of the company’s ecosystem.

Tesla is currently in a “transitional year.” The company is moving between two major growth waves: the first was the global expansion of the Model 3/Y platform, and the second is expected to be the next-generation low-cost vehicle and the commercialization of autonomous driving. In the “Money” world, these gaps between growth cycles are known as “dead zones,” where the stock may languish or decline until the next catalyst becomes clear.

For the value-conscious investor, the decline in Tesla’s P/E ratio makes the entry point more attractive than it has been in years. However, for the risk-averse, the combination of narrowing margins, fierce Chinese competition, and the unpredictable nature of its leadership suggests that the volatility is far from over.

In conclusion, Tesla stock is down today not because the company is failing, but because it is maturing. It is transitioning from a speculative hyper-growth story into a massive industrial entity that must now face the same economic gravity as every other Fortune 500 company. For those managing their personal portfolios, the key is to look past the daily noise and decide whether Tesla’s long-term “terminal value” justifies the bumpy ride of the present.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.