Understanding Provisions: A Cornerstone of Prudent Financial Reporting

In the realm of accounting, the concept of provisioning is fundamental to presenting a true and fair view of a company’s financial position. It’s a critical process that deals with potential future liabilities or expenses that are uncertain in timing or amount, but where the outflow of economic resources is probable. Unlike actual expenses that have already been incurred and can be precisely measured, provisions are estimates based on the best available information at the reporting date. They represent a proactive approach to financial management, ensuring that a company anticipates and accounts for potential future financial drains. This article delves into the intricacies of provisioning in accounting, exploring its definition, purpose, recognition criteria, types, and its significant implications for businesses.

The Genesis and Purpose of Accounting Provisions

The core principle behind provisioning lies in the accrual basis of accounting. This accounting method recognizes revenues and expenses as they are earned or incurred, regardless of when cash is actually exchanged. Provisions are a direct manifestation of this principle, requiring companies to recognize anticipated future obligations even if no invoice has been received or no direct cash payment has been made yet.

The Principle of Prudence

At its heart, provisioning embodies the accounting principle of prudence, also known as conservatism. This principle dictates that when faced with uncertainty, accountants should err on the side of caution. This means anticipating potential losses or expenses and recognizing them in the financial statements, while deferring the recognition of potential gains until they are virtually certain. In the context of provisions, this translates to acknowledging probable outflows of resources rather than waiting for them to materialize. Without provisioning, financial statements could present an overly optimistic picture of a company’s financial health, potentially misleading stakeholders.

Matching Principle and Accurate Financial Picture

Furthermore, provisioning is intrinsically linked to the matching principle. This principle requires that expenses be matched with the revenues they help to generate in the same accounting period. If a company is aware of a future expense that relates to its current operations or past activities, it’s crucial to recognize that expense in the period it relates to, even if the cash payment is due later. For instance, if a company sells a product with a warranty, the expected cost of fulfilling that warranty should be recognized as an expense in the same period the product is sold, not when a customer actually claims the warranty. Provisions ensure that the income statement accurately reflects the true cost of doing business and that the balance sheet provides a more realistic portrayal of liabilities.

Enhancing Stakeholder Confidence

By acknowledging and quantifying potential future outflows, provisions significantly enhance the reliability and transparency of financial reporting. Investors, creditors, and other stakeholders rely on financial statements to make informed decisions. Provisions demonstrate a company’s commitment to forthright financial disclosure, building trust and confidence in its management and its ability to navigate financial uncertainties. This proactive approach can also signal strong internal controls and a forward-thinking financial strategy.

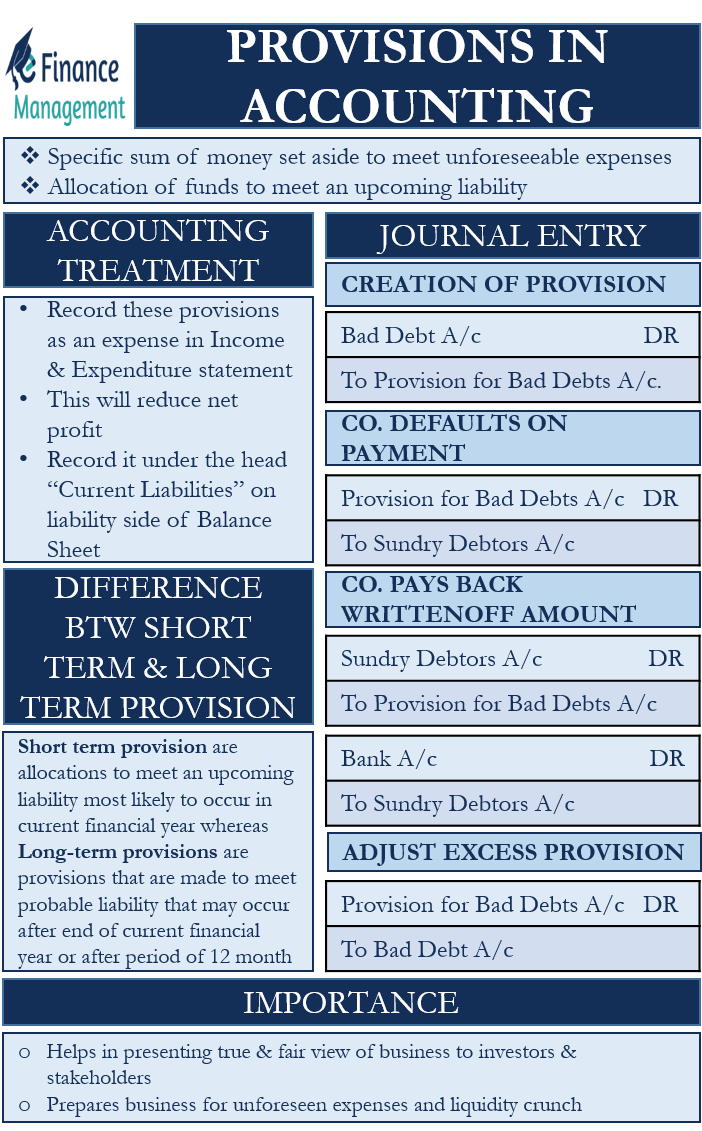

Criteria for Recognizing a Provision

The recognition of a provision is not arbitrary; it’s governed by specific criteria that ensure consistency and prevent the manipulation of financial statements. Generally, for a provision to be recognized, three conditions must be met:

1. Present Obligation

There must be a present obligation, either legal or constructive, arising from past events.

- Legal Obligation: This arises from a contract, statute, or operation of law. For example, a company might have a legal obligation to pay damages in a lawsuit that is currently ongoing and where the outcome is highly likely to result in a financial penalty.

- Constructive Obligation: This arises from a company’s actions, where its past practice, published policies, or specific statements have created a valid expectation in others that it will discharge its responsibilities. For instance, a company that has a consistent policy of offering refunds for faulty products creates a constructive obligation to do so for future sales, even if no formal legal contract mandates it. The key here is the creation of a legitimate expectation in third parties.

2. Probable Outflow of Resources

It must be probable that an outflow of resources embodying economic benefits will be required to settle the obligation. “Probable” is typically interpreted as more likely than not, often meaning a probability of greater than 50%. This is where the estimation and judgment of management come into play. Accountants will assess all available evidence, including expert opinions, historical data, and industry trends, to determine the likelihood of an outflow. If the outflow is only possible or remote, a provision is generally not recognized.

3. Reliable Estimate of the Amount

The amount of the obligation can be measured reliably. This doesn’t mean the amount has to be exact, but it must be possible to make a reasonable estimate. If a reliable estimate cannot be made, the obligation may not meet the recognition criteria for a provision, although it might still need to be disclosed as a contingent liability if it meets certain disclosure thresholds. The reliability of the estimate is crucial for ensuring the accuracy of the financial statements.

Common Types of Provisions in Accounting

Provisions manifest in various forms across different industries and business activities. Understanding these common types provides practical insight into the application of provisioning principles.

Warranty Provisions

When a company sells a product, it often offers a warranty to the customer, promising to repair or replace the product if it proves defective within a specified period. The cost of fulfilling these warranty obligations is an expense that relates to the sale of the product in the current period. Therefore, companies will estimate the likely cost of future warranty claims based on historical data, product defect rates, and the terms of the warranty. This estimated future cost is recognized as a provision for warranties at the time of sale.

Restructuring Provisions

Restructuring provisions are recognized when a company commits to a detailed formal plan for restructuring and has raised a valid expectation that the restructuring will take place by announcing it to those affected. Restructuring can involve activities such as closing down a business unit, relocating operations, or terminating employees. The provision would typically cover costs such as redundancy payments, lease termination penalties, and costs associated with retraining or relocating employees.

Litigation Provisions

Companies are often involved in legal disputes. If a company is a defendant in a lawsuit and, based on the advice of legal counsel, it is probable that the company will have to pay damages, a provision for litigation may be recognized. The amount of the provision would be the best estimate of the damages that will be incurred. This requires careful assessment of the legal case, the likelihood of a loss, and the potential financial impact.

Environmental Provisions

Businesses that engage in activities with potential environmental impacts may incur obligations for future environmental remediation or cleanup. For example, a company operating a mining facility might have a legal or constructive obligation to restore the site to its original condition after operations cease. Provisions for environmental liabilities are recognized when these obligations arise and can be reliably estimated. This often involves significant engineering and environmental assessments.

Provisions for Doubtful Debts (Allowances for Bad Debts)

While technically an allowance, the concept closely aligns with provisioning. Companies extend credit to their customers, and there’s always a risk that some customers may not pay their debts. A provision for doubtful debts (or allowance for bad debts) is established to recognize the estimated uncollectible amount of accounts receivable. This is based on historical collection patterns, aging of receivables, and specific customer creditworthiness assessments. It reduces the net realizable value of accounts receivable on the balance sheet.

Provisions for Employee Benefits

This can encompass various employee-related future obligations. For instance, companies may make provisions for anticipated bonuses that are probable and can be reliably estimated, or for long-service leave entitlements. In some jurisdictions, specific employee benefit obligations, such as pensions or post-retirement health benefits, are accounted for using complex actuarial valuations that result in provisions.

The Importance and Impact of Provisions

The effective management and reporting of provisions have far-reaching implications for a company’s financial health, strategic decision-making, and overall market perception.

Impact on Profitability

When a provision is recognized, it typically results in an expense being recorded in the income statement. This directly reduces a company’s reported profit for the period. While this might seem detrimental, it’s essential for accurate profit measurement. By recognizing these anticipated costs, companies avoid overstating profits in periods where these costs are incurred and understating them in periods where the related revenue is recognized. This leads to a more stable and predictable profit trend over time.

Influence on Financial Ratios

Provisions directly impact various financial ratios used by stakeholders to assess a company’s performance and financial standing. For example:

- Profitability Ratios: Provisions reduce net income, thereby lowering profitability ratios such as Net Profit Margin and Earnings Per Share (EPS).

- Liquidity Ratios: While provisions themselves are not cash outflows, they can impact the reported value of assets (e.g., allowance for doubtful debts) and liabilities. A higher provision for liabilities can lead to lower asset turnover ratios.

- Solvency Ratios: Provisions increase liabilities, which can lead to a higher debt-to-equity ratio, potentially signaling increased financial risk.

Understanding the magnitude and nature of provisions is crucial for correctly interpreting these financial metrics.

Strategic Implications

The process of identifying and quantifying potential future liabilities through provisioning forces management to confront future risks and uncertainties head-on. This can drive strategic decision-making in several ways:

- Risk Management: The need to make provisions encourages robust risk identification and management processes. Companies are incentivized to mitigate risks that could lead to future financial outflows.

- Resource Allocation: By recognizing anticipated future costs, companies can better plan their cash flows and allocate resources more effectively to meet these obligations.

- Operational Improvements: The identification of recurring provisioning needs, such as for product defects, can highlight areas for operational improvement to reduce future liabilities.

Transparency and Disclosure

Accounting standards, such as International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), mandate specific disclosures related to provisions. Companies are typically required to disclose:

- The nature of the provision.

- The carrying amount at the beginning and end of the period.

- Any additions made during the period.

- Any amounts utilized (written off) during the period.

- The amount of any expected reimbursement from a third party.

- Significant assumptions used in estimating the amount.

This transparency allows stakeholders to understand the basis of provisions and their potential impact on the company’s future financial performance.

In conclusion, provisioning in accounting is a vital mechanism for ensuring financial statements reflect a realistic and prudent view of a company’s financial position. It is rooted in the principles of accrual accounting and conservatism, demanding that probable future liabilities be recognized and reliably estimated. By understanding the criteria for recognition and the various types of provisions, businesses can navigate financial uncertainties more effectively, enhance stakeholder confidence, and make more informed strategic decisions. The diligent application of provisioning principles is not merely an accounting exercise; it is a hallmark of sound financial stewardship.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.