Navigating the complexities of the Internal Revenue Service (IRS) is a fundamental aspect of personal finance that many individuals find daunting. Whether you are a salaried employee, a freelancer, or a small business owner, the question “How do I know if I owe the IRS?” is one that carries significant weight. Uncertainty regarding tax debt can lead to unnecessary anxiety, financial penalties, and long-term credit issues. In the modern financial landscape, the IRS has streamlined its processes, providing several digital and traditional avenues for taxpayers to verify their status. Understanding these tools and the formal communication channels used by the government is the first step toward achieving financial peace of mind and maintaining a healthy personal balance sheet.

Leveraging Digital Tools: The IRS Online Account and Transcripts

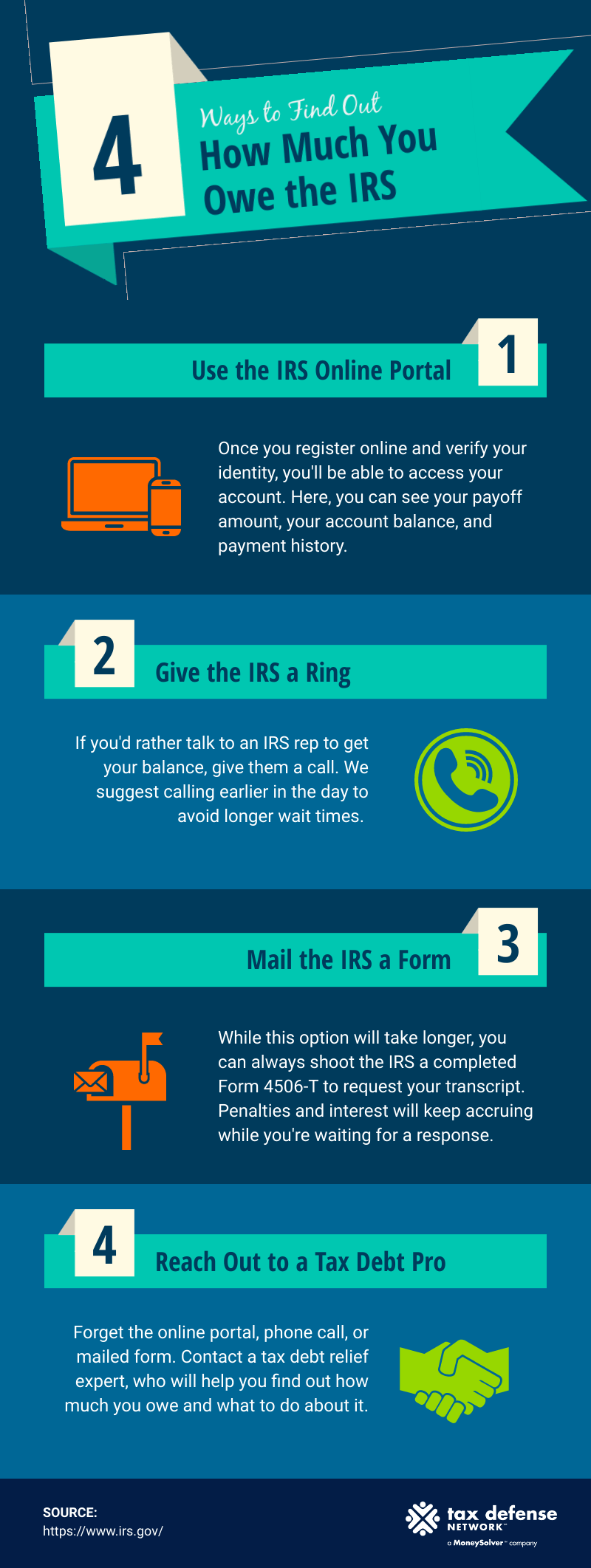

In an era defined by digital transformation, the most efficient way to determine if you have an outstanding balance is through the IRS’s official online portal. Over the past few years, the agency has invested heavily in its digital infrastructure, allowing taxpayers to access real-time data regarding their accounts.

Setting Up and Navigating Your Online Account

The IRS Online Account is a secure gateway that provides a snapshot of your federal tax status. To access this, you must verify your identity through ID.me, a third-party service that ensures your sensitive financial data remains protected. Once logged in, you can view the total amount owed, including a breakdown by tax year. This dashboard also displays your payment history, any scheduled payments, and key information from your most recent tax return. For anyone managing their personal finances, checking this portal at least once a quarter is a prudent habit to ensure no surprises arise during the peak of tax season.

Understanding Tax Transcripts

If the online dashboard shows a balance but you are unsure of the origin, requesting a tax transcript is the logical next step. There are several types of transcripts, but the “Account Transcript” is the most useful for identifying debt. It provides a chronological record of your account, showing the original tax assessed, any subsequent adjustments made by the IRS, payments made, and accrued interest or penalties. By reviewing this document, you can trace exactly when a liability was triggered—whether it was due to an underpayment of estimated taxes or a math error on a previous filing.

Monitoring Withholding and Estimated Payments

For those with fluctuating incomes, such as gig workers or independent contractors, owing money often stems from insufficient withholding. The IRS Online Account allows you to cross-reference what you have paid against what you project to owe. By using these digital tools in conjunction with a tax calculator, you can proactively adjust your financial strategy mid-year, ensuring that you aren’t met with an unexpected bill when you file your annual return.

Deciphering Official Correspondence and IRS Notices

While digital tools are proactive, the IRS remains a traditional institution that primarily communicates through the United States Postal Service. If you owe money, the IRS is legally obligated to notify you via written correspondence. Understanding how to read these notices is vital for your financial security.

Identifying Common IRS Notices

The most common notice sent to taxpayers who owe a balance is the CP14. This is the initial notice stating that you have unpaid taxes. If this goes unaddressed, you may receive a CP501 or CP504, which act as reminders and notices of intent to levy. Another critical document is the CP2000, which is issued when the information reported on your tax return does not match the information the IRS received from third parties (like your employer’s W-2 or a bank’s 1099). A CP2000 is not a bill, but a “proposal” to change your tax liability. Ignoring these documents is a critical financial mistake, as interest begins accruing from the original due date of the return.

Distinguishing Official Mail from Scams

In the realm of personal finance, security is paramount. A major concern for many taxpayers is the prevalence of tax-related identity theft and phishing scams. It is important to remember that the IRS does not initiate contact via email, text message, or social media to request personal or financial information. Furthermore, the IRS will never demand immediate payment over the phone using specific methods like gift cards, wire transfers, or prepaid debit cards. Official notices will always arrive in an envelope with the Department of the Treasury seal and will provide clear instructions on how to dispute the findings or pay through official government channels.

The Importance of the “Certified Mail” Response

When you receive a notice stating you owe money, your response time is often limited to 30 or 60 days. From a financial management perspective, it is best practice to respond via certified mail with a return receipt requested. This provides you with a paper trail proving you addressed the matter within the legal timeframe. Whether you agree with the debt or intend to dispute it, maintaining organized records of all correspondence is essential for protecting your rights and your credit score.

![]()

Alternative Methods for Verifying Tax Debt

While online accounts and mail are the primary channels, there are alternative methods to confirm your standing with the IRS, especially if you suspect you have missed mail or cannot access digital tools due to technical issues.

Utilizing the IRS Toll-Free Telephone Lines

For individuals who prefer verbal confirmation, the IRS maintains several toll-free lines. While wait times can be significant—especially during the spring—speaking with a representative allows you to ask specific questions about the nature of your debt. Before calling, you should have your Social Security Number, date of birth, and previous year’s tax return ready. The representative can provide a “payoff amount,” which includes the base tax plus interest calculated to a specific date. This is a critical figure if you are looking to clear your debt in a single lump sum.

Requesting Information via Form 4506-T

If you are unable to use the online “Get Transcript” tool, you can submit Form 4506-T (Request for Transcript of Tax Return) by mail. This is a more formal and slower process, but it is a reliable way to get a hard copy of your tax records. Many financial institutions require these transcripts when you are applying for a mortgage or a large business loan, making it a valuable tool for broader financial planning. Knowing your debt status through this form ensures that your debt-to-income ratio calculations are accurate before you approach a lender.

Consulting Financial Professionals

Sometimes, the reason you owe money is complex, involving capital gains, foreign assets, or intricate business expenses. In these cases, the best way to know if you owe the IRS—and how much you truly should be paying—is to hire a Certified Public Accountant (CPA) or an Enrolled Agent (EA). These professionals have the authority to represent you before the IRS. They can perform a “tax check-up” by pulling your transcripts through their professional software and identifying if you qualify for any credits or deductions that could offset your debt. This is often an investment that pays for itself by reducing your overall liability.

Strategies for Managing and Resolving Unpaid Tax Debt

Once you have confirmed that you owe the IRS, the focus must shift from discovery to resolution. The IRS is one of the world’s most powerful creditors, but they also offer several programs designed to help taxpayers settle their debts without falling into financial ruin.

Exploring Installment Agreements

If you cannot pay your tax debt in full, an Installment Agreement (IA) is the most common financial tool used to manage the liability. A “Short-Term Payment Plan” gives you up to 180 days to pay the balance in full, often with lower fees. For larger debts that require more time, a “Long-Term Payment Plan” (Direct Debit Installment Agreement) allows you to make monthly payments over several years. Setting up these plans is a vital step in personal finance because it stops the aggressive collection actions, such as wage garnishments or bank levies, that can devastate a household budget.

The Offer in Compromise (OIC) and Currently Not Collectible (CNC) Status

For those in genuine financial hardship, the IRS provides the Offer in Compromise program. This allows a taxpayer to settle their debt for less than the full amount owed. The IRS evaluates your “Reasonable Collection Potential” based on your income, expenses, and asset equity. While the approval rate for OICs is relatively low, it is a powerful tool for those whose liabilities far exceed their financial means. Alternatively, if paying the debt would prevent you from meeting basic living expenses, you may request “Currently Not Collectible” status. This doesn’t erase the debt, but it pauses collection activity until your financial situation improves.

Minimizing Penalties and Interest

Interest on IRS debt is compounded daily, and penalties for late payment can add up quickly. However, many taxpayers are unaware of “First-Time Abatements.” If you have a clean compliance history for the past three years, you may be eligible to have certain penalties removed. In the context of personal finance, this can save you hundreds or even thousands of dollars. Always ask a tax professional or an IRS representative if you qualify for penalty relief once you have established a plan to pay the underlying tax.

Conclusion: Proactive Financial Health

Determining if you owe the IRS is not merely a task for the month of April; it is a vital component of ongoing financial literacy. By utilizing the IRS Online Account, staying vigilant with your mail, and seeking professional guidance when necessary, you can transform a stressful uncertainty into a manageable financial plan. The key to successful wealth management is transparency. When you know exactly where you stand with the government, you can make informed decisions about investing, saving, and spending. Ultimately, the goal is to move from a state of questioning your liability to a state of total control over your financial future, ensuring that the IRS is a partner in your compliance rather than an obstacle to your prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.