For many professionals moving from a traditional W-2 employment structure to the world of freelancing, entrepreneurship, or independent contracting, the shift in financial responsibility can be jarring. One of the most significant changes is the transition from automatic tax withholding to the system of quarterly estimated tax payments. While the annual tax deadline in April is a household date, the four interim deadlines throughout the year are equally critical for maintaining financial health and staying compliant with the Internal Revenue Service (IRS).

Understanding how to pay taxes quarterly is not merely a matter of administrative compliance; it is a fundamental pillar of sophisticated business finance. Failing to navigate this system correctly can lead to underpayment penalties, unexpected liquidity crises, and unnecessary stress. This guide provides a deep dive into the mechanics of quarterly taxes, offering a roadmap for managing your personal and business finances with precision.

1. Determining Your Liability: Who Must Pay Quarterly?

The United States tax system is a “pay-as-you-go” system. This means the government expects to receive tax revenue as you earn or receive income throughout the year, rather than in one lump sum at the end. For employees, this is handled via payroll withholding. For those in the “Money” niche—investors, business owners, and freelancers—this responsibility falls directly on the individual.

The $1,000 Threshold and the Self-Employed

Generally, if you expect to owe at least $1,000 in tax for the current year after subtracting your withholding and transferable credits, you are likely required to make estimated tax payments. This applies to sole proprietors, partners, and S-corporation shareholders. If your income comes from 1099-NEC or 1099-MISC forms, or if you have significant income from dividends, interest, or capital gains that aren’t subject to withholding, you fall into this category.

The Safe Harbor Rule

One of the most important concepts in personal finance is the “Safe Harbor” rule, which protects taxpayers from underpayment penalties. To qualify, you must generally pay at least 90% of the tax you owe for the current year or 100% of the tax shown on your return for the prior year (110% if your adjusted gross income was more than $150,000). Understanding these benchmarks allows you to budget effectively without over-leveraging your cash reserves.

Corporate and High-Net-Worth Obligations

It isn’t just freelancers who need to worry about quarterly payments. Corporations generally have to make estimated tax payments if they expect to owe tax of $500 or more. Furthermore, high-net-worth individuals who receive substantial passive income from real estate or private equity must also integrate quarterly estimates into their broader wealth management strategy to avoid eroding their returns through avoidable IRS penalties.

2. Calculating Your Estimated Tax Obligations

The most daunting aspect of quarterly taxes is the calculation. Because you are paying based on projections rather than finalized year-end figures, precision is key to ensuring you don’t overpay (which hurts your current cash flow) or underpay (which leads to penalties).

Estimating Adjusted Gross Income (AGI)

To start, you must project your total expected income for the year. This includes all sources of revenue minus “above-the-line” deductions. For a business owner, this means calculating your gross receipts and subtracting necessary business expenses such as equipment, marketing, and professional services. The resulting figure is your net profit, which forms the basis of your taxable income.

Factoring in Self-Employment Tax

A common mistake in personal finance is forgetting that self-employed individuals must pay both the employer and employee portions of Social Security and Medicare taxes. This is known as the Self-Employment (SE) tax, which currently sits at 15.3%. When calculating your quarterly payments, you must account for this SE tax in addition to your standard income tax bracket rates.

Utilizing IRS Form 1040-ES

The IRS provides a specific worksheet, Form 1040-ES (Estimated Tax for Individuals), to help taxpayers navigate these calculations. This form guides you through your expected AGI, taxes, deductions, and credits. While it may seem cumbersome, it is an invaluable financial tool. Many professionals also use the “Effective Tax Rate” method—taking the percentage of tax paid the previous year and applying it to current quarterly earnings—to simplify the process.

3. The Mechanics of Payment: Methods and Platforms

Once you have calculated your liability, the next step is the actual transfer of funds. The modern financial landscape offers several digital avenues to ensure your payments are timely and documented.

IRS Direct Pay and EFTPS

The most direct method is using IRS Direct Pay, which allows you to pay directly from your checking or savings account without any fees. For business owners with higher volume or more complex needs, the Electronic Federal Tax Payment System (EFTPS) is a free service provided by the U.S. Department of the Treasury. EFTPS is highly recommended for those who want to track their payment history over several years and schedule payments in advance, which is a hallmark of disciplined financial planning.

Digital Wallets and Credit Cards

In recent years, the IRS has expanded payment options to include debit cards, credit cards, and digital wallets like PayPal or Click to Pay. While these offer convenience, they often come with processing fees charged by third-party providers. From an investment perspective, using a credit card to pay taxes only makes sense if the rewards or points earned significantly outweigh the processing fee, or if you are using it as a short-term liquidity bridge.

Managing State and Local Obligations

It is vital to remember that the IRS only handles federal taxes. Most states also require quarterly estimated payments if you live in a state with income tax. Each state has its own portal and specific deadlines (though they usually mirror the federal ones). Neglecting state payments is a common oversight that can lead to aggressive collection efforts and high-interest penalties at the state level.

4. Strategic Cash Flow Management for Tax Compliance

Paying taxes quarterly is as much about psychological discipline as it is about accounting. Professionals who succeed in the long term treat their tax obligation as a non-negotiable business expense that is “escrowed” in real-time.

The Percentage Method

A gold-standard practice in business finance is to set aside a fixed percentage of every dollar that enters your account. Depending on your income level and state of residence, this usually ranges from 25% to 35%. By moving this money into a separate, dedicated “Tax” account the moment an invoice is paid, you ensure that you are never “spending the government’s money.”

Leveraging High-Yield Savings Accounts (HYSA)

Because you only pay the IRS four times a year, you may be holding significant sums of tax money for months at a time. Rather than letting this capital sit idle in a standard checking account, savvy financial managers place these funds in a High-Yield Savings Account. This allows you to earn 4-5% interest on the money before it is sent to the IRS, effectively turning your tax liability into a small source of passive income.

The Role of Modern Bookkeeping Tools

In the “Money” niche, efficiency is profit. Utilizing financial tools like QuickBooks, FreshBooks, or specialized tax software for freelancers can automate the tracking of expenses and income. These tools often provide real-time estimates of what you owe, taking the guesswork out of the quarterly cycle. Integrating these tools with your bank accounts ensures that your records are always “audit-ready.”

5. Deadlines, Records, and Avoiding Penalties

Consistency is the final piece of the quarterly tax puzzle. The IRS operates on a specific calendar that does not perfectly align with standard three-month quarters, making it essential to mark your calendar in advance.

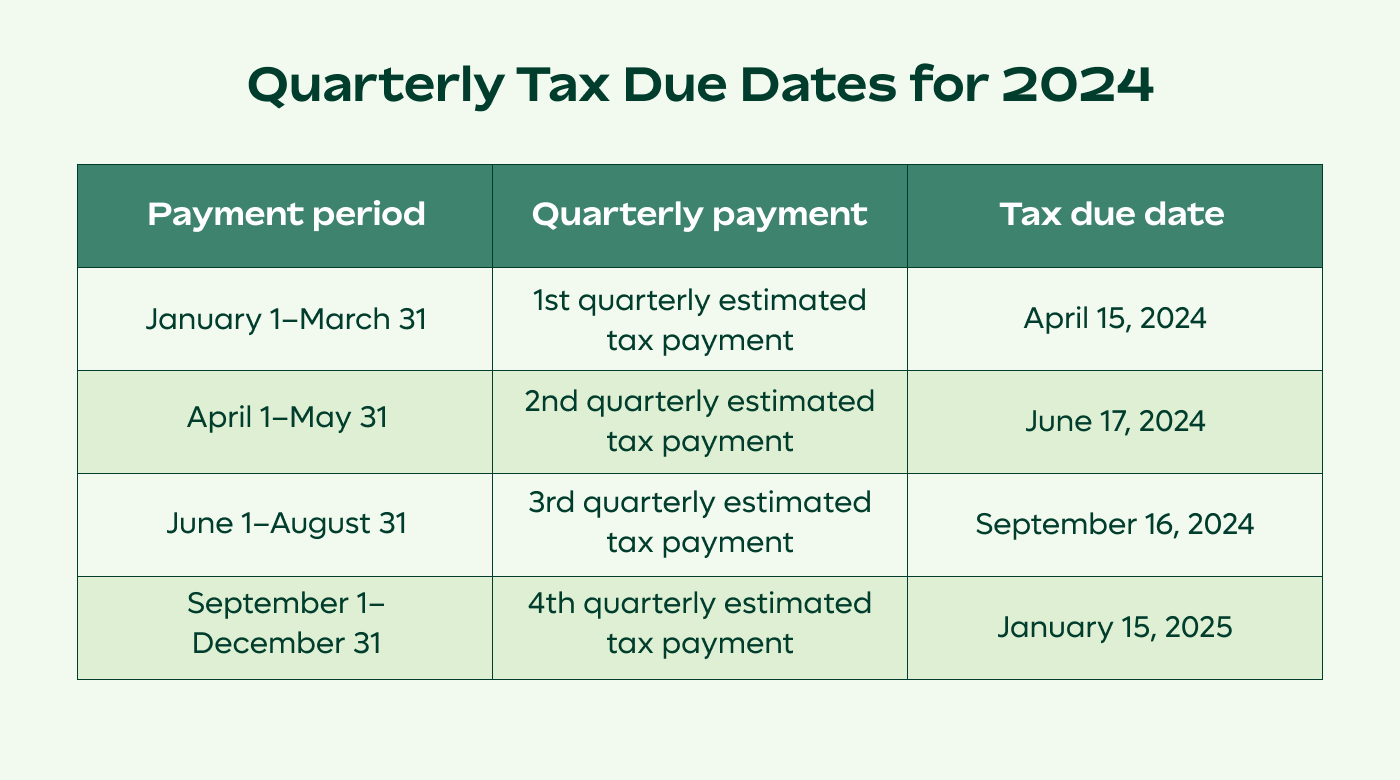

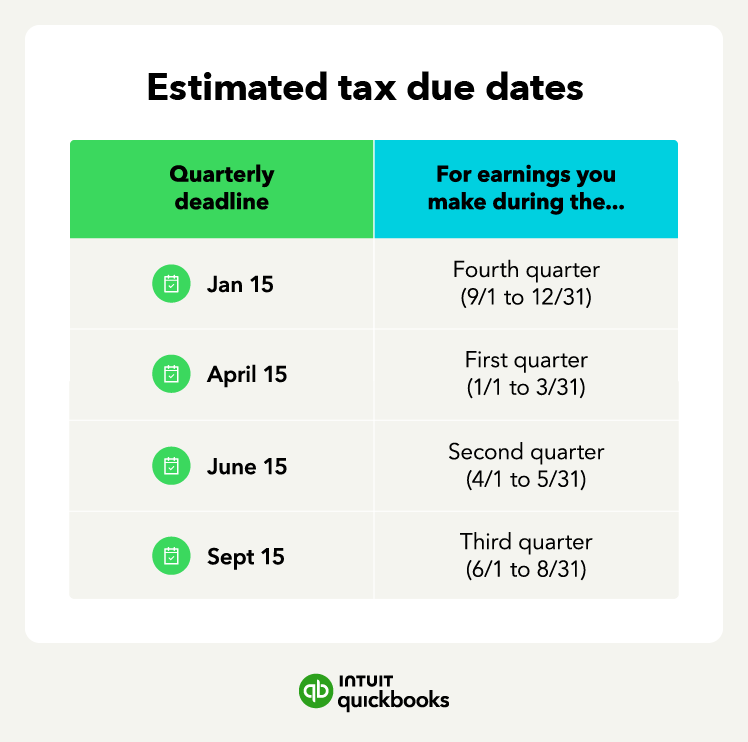

The Four Critical Deadlines

The standard deadlines for quarterly estimated payments are:

- April 15: For income earned Jan 1 – March 31.

- June 15: For income earned April 1 – May 31.

- September 15: For income earned June 1 – Aug 31.

- January 15 (of the following year): For income earned Sept 1 – Dec 31.

If these dates fall on a weekend or holiday, the deadline moves to the next business day. Missing these dates, even by a day, can trigger interest charges.

Maintaining an Impeccable Audit Trail

In the event of an IRS inquiry, your best defense is a clear paper trail. Every quarterly payment should be documented with a confirmation number and stored in a secure digital folder. Match these payments against your bank statements and your year-end 1040-ES worksheets. This level of organization not only protects you legally but also provides a clear historical view of your business’s profitability and tax efficiency over time.

Adjusting for Volatility

In many industries, income is seasonal. You might earn 70% of your income in the fourth quarter. The IRS allows for “annualized” installment methods, which let you pay less in the leaner quarters and more in the profitable ones. This prevents you from being cash-strapped during slow months. Consulting with a tax professional can help you implement this more advanced strategy to optimize your liquidity.

By mastering the rhythm of quarterly tax payments, you transform a potential financial burden into a streamlined part of your professional routine. This proactive approach ensures that when the “big” tax day arrives in April, you have already done the heavy lifting, leaving you free to focus on what matters most: growing your wealth and expanding your business.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.