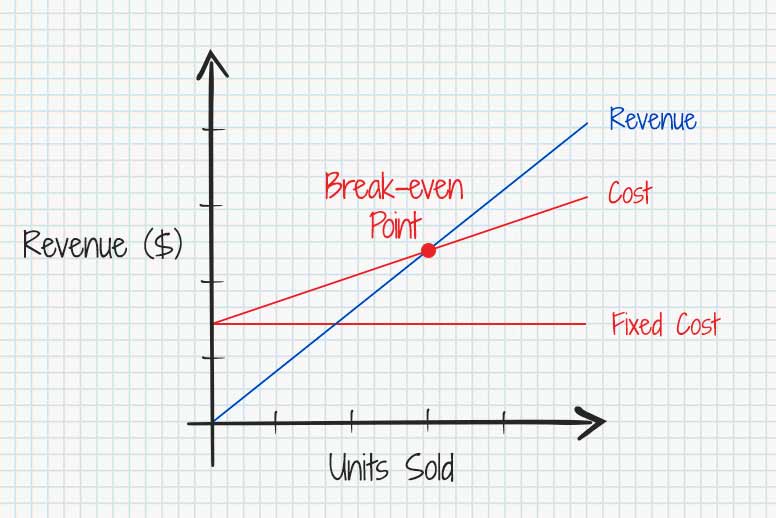

The breakeven point is a fundamental concept in business finance, representing the critical juncture where a company’s total revenues precisely equal its total costs. It’s not a measure of profitability, but rather a threshold of operational viability. Understanding and accurately calculating this point is paramount for any business, from a fledgling startup to an established corporation, as it provides invaluable insights into pricing strategies, cost management, sales targets, and overall financial health.

At its core, the breakeven point answers a simple yet vital question: how much do we need to sell to cover all our expenses? Reaching this point signifies that the business is no longer incurring losses, but it also means it hasn’t yet generated any profit. Every sale made beyond the breakeven point contributes directly to the company’s bottom line. Consequently, mastering the breakeven analysis allows businesses to make informed decisions, set realistic goals, and navigate the complexities of the market with greater confidence.

Understanding the Components: Fixed vs. Variable Costs

To truly grasp the breakeven point, it’s essential to dissect its foundational elements: fixed costs and variable costs. These two categories encompass all the expenses a business incurs, and their distinction is crucial for accurate calculation and strategic planning.

Fixed Costs: The Unwavering Expenses

Fixed costs are those expenses that remain constant regardless of the volume of goods or services produced or sold. They are the bedrock of your operational expenses, typically incurred on a regular basis, such as monthly or annually. Even if your business experiences zero sales in a given period, these costs will still need to be paid. Think of them as the essential infrastructure that keeps your business running, whether it’s busy or slow.

Examples of common fixed costs include:

- Rent or Mortgage Payments: The cost of your physical location, whether it’s an office, retail space, or manufacturing facility, is usually a fixed monthly expense.

- Salaries of Permanent Staff: The wages of employees who are not directly tied to production output, such as administrative personnel, management, and core sales teams, are generally fixed.

- Insurance Premiums: Business insurance, liability insurance, and property insurance typically involve fixed premiums paid periodically.

- Loan Payments: Repayments on business loans, including interest, are often scheduled fixed payments.

- Depreciation: The accounting method of spreading the cost of an asset over its useful life is a non-cash fixed expense.

- Software Subscriptions: Many business software solutions, like CRM systems or accounting software, come with fixed monthly or annual subscription fees.

- Utilities (Base Charges): While some utility costs fluctuate with usage, there are often base charges that remain constant.

The predictability of fixed costs is a double-edged sword. On one hand, it simplifies forecasting. On the other hand, it means that during periods of low sales, fixed costs can exert significant pressure on profitability, as they must be covered before any profit can be realized. Businesses with high fixed costs are said to have high operating leverage, meaning that a small change in sales can lead to a proportionally larger change in operating income.

Variable Costs: The Fluctuating Expenses

Variable costs, in direct contrast to fixed costs, are expenses that fluctuate directly with the level of production or sales volume. As a business produces more units or serves more customers, its variable costs will increase. Conversely, if sales decline, variable costs will decrease. These costs are directly linked to the creation or delivery of your product or service.

Common examples of variable costs include:

- Raw Materials: The cost of materials used in the manufacturing of a product is a prime example of a variable cost. More products manufactured mean more raw materials purchased.

- Direct Labor: Wages paid to production line workers or service providers whose work is directly tied to the output of each unit or service. If you produce 100 widgets, you’ll need labor for those 100 widgets; if you produce 1,000, you’ll need more labor.

- Sales Commissions: Commissions paid to sales representatives are typically a percentage of sales revenue, making them a variable cost.

- Packaging Costs: The cost of packaging each individual product sold is directly proportional to the number of units sold.

- Shipping and Delivery Costs: The expense of shipping products to customers will increase with the number of orders.

- Transaction Fees: Payment processing fees, which are often a percentage of each transaction, are variable costs.

Understanding variable costs is crucial for setting appropriate pricing. The selling price of a product or service must, at a minimum, cover its variable costs to avoid losing money on each individual sale. Once variable costs are covered, any revenue remaining contributes towards covering fixed costs and then generating profit.

Calculating the Breakeven Point: Formulas and Methods

The breakeven point can be calculated in two primary ways: in units and in sales dollars. Both methods provide valuable perspectives, and using them in conjunction offers a more comprehensive understanding of a business’s financial performance.

Breakeven Point in Units: How Many to Sell?

The breakeven point in units tells you the exact number of products or services you need to sell to cover all your costs. This metric is particularly useful for businesses that produce a single type of product or have a relatively homogenous product mix.

The formula for breakeven point in units is:

Breakeven Point (Units) = Total Fixed Costs / (Selling Price Per Unit – Variable Cost Per Unit)

Let’s break down this formula:

- Total Fixed Costs: This is the sum of all your fixed expenses over a specific period.

- Selling Price Per Unit: This is the price at which you sell one unit of your product or service.

- Variable Cost Per Unit: This is the total variable cost incurred for producing or delivering one unit.

The term (Selling Price Per Unit – Variable Cost Per Unit) is also known as the Contribution Margin Per Unit. The contribution margin represents the amount of revenue from each sale that contributes towards covering fixed costs and generating profit.

Example:

Suppose a company has fixed costs of $10,000 per month. They sell a product for $50 per unit, and the variable cost per unit is $30.

Contribution Margin Per Unit = $50 – $30 = $20

Breakeven Point (Units) = $10,000 / $20 = 500 units

This means the company needs to sell 500 units each month to cover all its expenses.

Breakeven Point in Sales Dollars: What Revenue is Needed?

The breakeven point in sales dollars indicates the total revenue a business needs to generate to cover all its costs. This is often more practical for businesses with multiple products or services, as it provides a top-line revenue target.

There are a couple of ways to calculate this:

Method 1: Using the Contribution Margin Ratio

Breakeven Point (Sales Dollars) = Total Fixed Costs / Contribution Margin Ratio

To use this formula, you first need to calculate the contribution margin ratio:

Contribution Margin Ratio = (Selling Price Per Unit – Variable Cost Per Unit) / Selling Price Per Unit

Or, more broadly:

Contribution Margin Ratio = Total Sales Revenue – Total Variable Costs / Total Sales Revenue

This ratio represents the percentage of each sales dollar that contributes to covering fixed costs and generating profit.

Example (Continuing from above):

Selling Price Per Unit = $50

Variable Cost Per Unit = $30

Contribution Margin Per Unit = $20

Contribution Margin Ratio = $20 / $50 = 0.40 or 40%

Breakeven Point (Sales Dollars) = $10,000 / 0.40 = $25,000

This means the company needs to generate $25,000 in sales revenue to break even.

Method 2: Using the Breakeven Point in Units

If you’ve already calculated the breakeven point in units, you can easily convert it to sales dollars:

Breakeven Point (Sales Dollars) = Breakeven Point (Units) * Selling Price Per Unit

Example (Continuing from above):

Breakeven Point (Units) = 500 units

Selling Price Per Unit = $50

Breakeven Point (Sales Dollars) = 500 * $50 = $25,000

Both methods yield the same result, providing a clear revenue target.

Strategic Implications and Applications of Breakeven Analysis

The breakeven point is more than just a number; it’s a powerful analytical tool with far-reaching implications for business strategy and decision-making. Its applications extend across various facets of operations, from pricing and product development to investment and risk assessment.

Pricing Strategies and Profitability Targets

One of the most immediate applications of breakeven analysis is in setting effective pricing strategies. By understanding the breakeven point, businesses can ensure their prices are not only competitive but also sufficient to cover all costs.

- Setting Minimum Prices: The breakeven point clearly indicates the minimum sales volume required at a given price to avoid losses. If a company is considering lowering prices to gain market share, they must ensure the new price still allows them to reach their breakeven point with a feasible sales volume.

- Evaluating Price Increases: If a business is contemplating a price increase, breakeven analysis can help assess the impact. A higher selling price, with other costs remaining constant, will lower the breakeven point, meaning fewer units need to be sold to achieve profitability. This can be a valuable strategy when facing rising costs or aiming to boost profit margins.

- Product Profitability: For businesses with multiple product lines, breakeven analysis can be applied to each product individually. This helps identify which products are the most efficient at covering costs and contributing to overall profitability. Products with a high contribution margin per unit are generally more desirable.

Sales Forecasting and Goal Setting

The breakeven point serves as a crucial benchmark for sales forecasting and setting realistic sales targets.

- Defining Minimum Sales Goals: The breakeven unit or dollar amount provides a non-negotiable minimum sales target for any given period. Sales teams can be motivated by this clear objective, understanding that reaching it signifies operational stability.

- Benchmarking Performance: Actual sales figures can be compared against the breakeven point to assess performance. If a business consistently falls short of its breakeven point, it signals an urgent need for strategic adjustments. Conversely, consistently exceeding the breakeven point indicates a healthy and growing operation.

- Scenario Planning: Breakeven analysis can be used to model different sales scenarios. For instance, a business can project its breakeven point under various market conditions or with different sales growth assumptions, allowing for proactive planning and risk mitigation.

Cost Management and Operational Efficiency

Understanding the interplay between fixed and variable costs is fundamental to effective cost management. Breakeven analysis highlights areas where cost reductions can have the most significant impact.

- Identifying Cost Drivers: The analysis helps pinpoint which costs are contributing most to the breakeven point. High fixed costs, for example, might necessitate a review of overhead expenses, while high variable costs might prompt an investigation into procurement or production processes.

- Optimizing Resource Allocation: By understanding the cost structure, businesses can make more informed decisions about resource allocation. For instance, if a company has a high breakeven point due to substantial fixed costs, it might prioritize efforts to increase sales volume rather than focusing solely on marginal cost reductions.

- Evaluating Operational Changes: When considering operational changes, such as investing in new technology or outsourcing certain functions, breakeven analysis can help assess the financial implications. For example, a capital investment in automation might increase fixed costs but decrease variable costs, thereby altering the breakeven point.

Investment Decisions and Business Valuation

Breakeven analysis also plays a role in evaluating investment opportunities and understanding a business’s intrinsic value.

- Assessing New Ventures: Before launching a new product or service, conducting a breakeven analysis is essential to determine its potential viability and the sales volume required for it to become profitable.

- Securing Financing: Lenders and investors often require a clear understanding of a business’s breakeven point as part of their due diligence. A low breakeven point can signal a more resilient business, capable of weathering economic downturns.

- Business Valuation: For established businesses, the breakeven point can be an indicator of operational efficiency and financial health, which can influence its valuation. A business that can break even at a relatively low sales volume is generally more attractive than one requiring extremely high sales to cover its costs.

In conclusion, the breakeven point is a foundational pillar of sound financial management. It transforms abstract financial data into actionable insights, empowering businesses to make strategic decisions, set achievable goals, and ultimately navigate the path to sustained profitability with clarity and purpose. By diligently understanding, calculating, and applying breakeven analysis, businesses can build a more robust and resilient financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.