Understanding the intricacies of credit card balances is fundamental to effective personal finance management. It’s a concept that, while seemingly straightforward, carries significant implications for your financial health, creditworthiness, and overall spending power. A credit card balance represents the amount of money you owe to the credit card issuer for purchases, cash advances, balance transfers, and any associated fees or interest that have accumulated. It’s the running total of your financial obligations that must be repaid.

The Anatomy of a Credit Card Balance

Delving deeper, a credit card balance isn’t a static figure. It’s a dynamic representation of your financial activity over a billing cycle. Several components contribute to its calculation and fluctuation.

Current Balance vs. Statement Balance

It’s crucial to distinguish between your current balance and your statement balance.

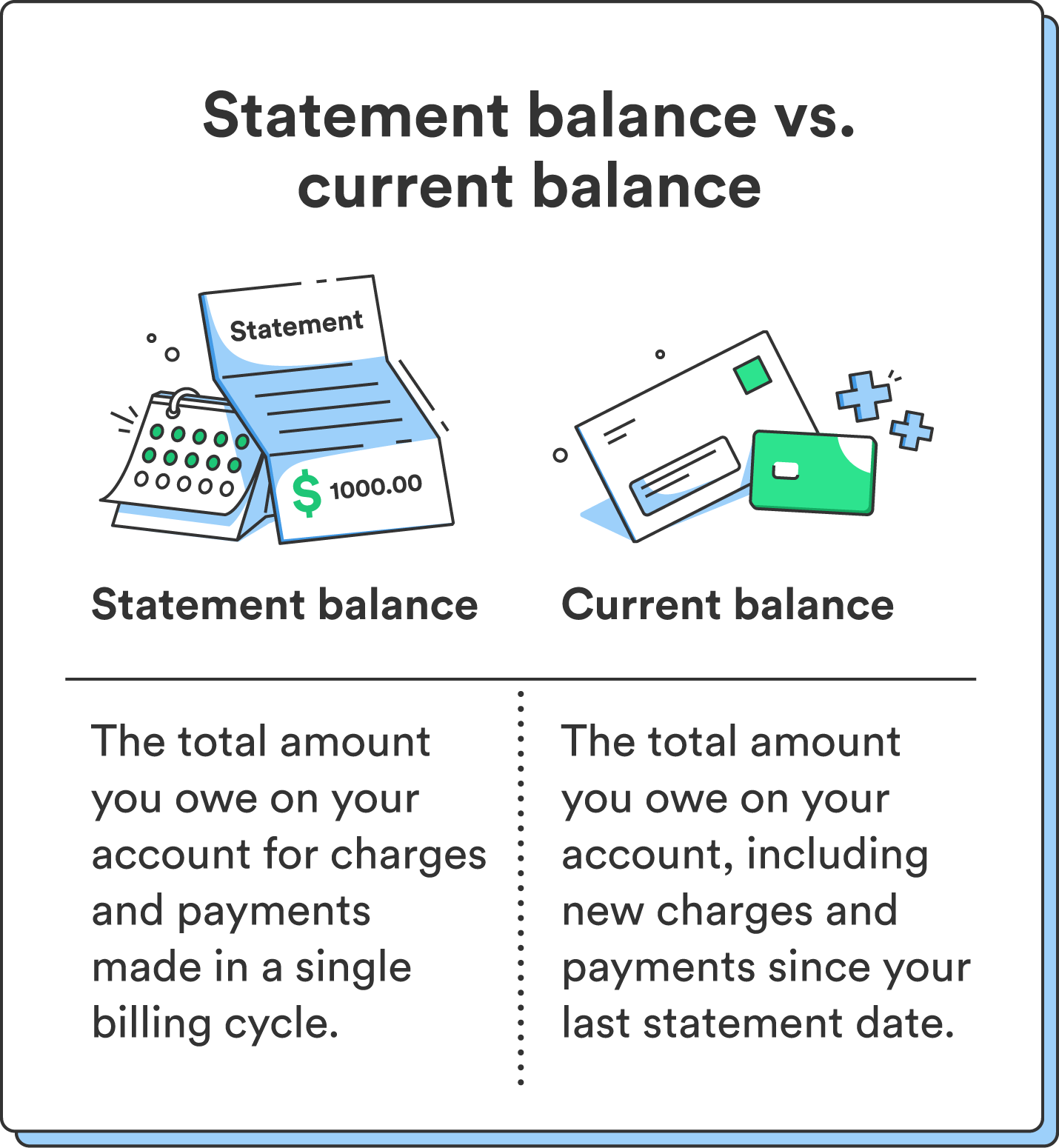

Current Balance

Your current balance, often referred to as your “real-time” or “pending” balance, reflects all transactions that have been posted to your account since your last statement was generated. This includes new purchases, payments made, and any pending authorizations. This figure is constantly updating and provides an immediate snapshot of your outstanding debt. It’s particularly important to monitor your current balance to stay within your credit limit and avoid potential over-limit fees. While helpful for tracking immediate spending, it’s not the balance you are legally obligated to pay by a specific due date.

Statement Balance

The statement balance is the total amount you owe on your credit card as of the closing date of your billing statement. This is the figure that is officially reported to credit bureaus and is the basis for your minimum payment and the amount due by your payment due date. It includes all transactions that posted during that specific billing cycle and any unpaid balance carried over from previous cycles. Understanding your statement balance is paramount as it dictates your repayment obligations and influences your credit utilization ratio.

Key Components Contributing to the Balance

Several elements can contribute to the overall balance on your credit card, making it imperative to be aware of each.

Purchases

The most common component of a credit card balance is the accumulated cost of goods and services you’ve purchased using the card. Every swipe, tap, or online transaction adds to this figure. The aggregate of these transactions, minus any returns or credits, forms a significant portion of your balance.

Cash Advances

Taking out cash using your credit card is known as a cash advance. These transactions typically come with higher interest rates than regular purchases and often accrue interest immediately, with no grace period. Furthermore, a cash advance fee is usually applied. These factors can significantly inflate your balance quickly.

Balance Transfers

A balance transfer involves moving the outstanding debt from one credit card to another, often to take advantage of a lower introductory interest rate or a promotional offer. While this can be a strategic financial move, the transferred amount becomes part of the balance on the new card and will be subject to its terms and conditions. If the introductory period ends without the balance being fully paid off, the standard APR for that card will apply, potentially increasing the overall cost.

Fees

Various fees can be added to your credit card balance. These can include:

- Annual fees: Some credit cards charge a fee for the privilege of using the card.

- Late payment fees: If you fail to make at least the minimum payment by the due date, a late fee will be assessed.

- Over-limit fees: If your spending exceeds your credit limit, some issuers may charge a fee (though many now require opt-in for this).

- Foreign transaction fees: When you make purchases in a foreign currency or from a merchant outside your home country, a percentage of the transaction amount might be added as a fee.

- Balance transfer fees: A fee is typically charged for initiating a balance transfer, usually a percentage of the amount transferred.

Interest Charges

This is perhaps the most significant factor that can inflate your credit card balance if not managed carefully. Interest is the cost of borrowing money. If you don’t pay your statement balance in full by the due date, interest will be charged on the remaining unpaid amount. This interest accrues daily and is added to your balance, leading to a snowball effect if not addressed. The Annual Percentage Rate (APR) dictates how much interest you’ll be charged.

The Significance of Your Credit Card Balance

Your credit card balance is more than just a number; it’s a critical metric that impacts your financial well-being in several ways. Understanding its implications can empower you to make smarter financial decisions.

Impact on Credit Utilization Ratio

One of the most direct impacts of your credit card balance is on your credit utilization ratio. This ratio is calculated by dividing the total amount of credit you are currently using by your total available credit. For example, if you have a credit card with a $10,000 limit and a balance of $3,000, your utilization ratio for that card is 30%. Credit utilization is a major factor in credit scoring models, with a lower ratio generally being more favorable.

Maintaining a Healthy Credit Utilization Ratio

Experts generally recommend keeping your credit utilization ratio below 30% for each card and in total. A ratio above this threshold can negatively affect your credit score, signaling to lenders that you may be overextended or a higher credit risk. High utilization can also lead to higher interest charges, as lenders may perceive you as more likely to carry a balance. By actively managing your balances and paying down debt, you can improve your credit utilization and, consequently, your credit score.

Influence on Credit Score

Your credit card balance directly influences your credit score through several mechanisms, primarily credit utilization and payment history.

Payment History

The most significant factor in your credit score is your payment history. If your credit card balance is too high, it can make it difficult to meet your minimum payment obligations. Consistently paying late or missing payments will severely damage your credit score. Conversely, making timely payments on your credit card balances demonstrates responsible credit management.

Credit Utilization

As discussed, a high credit utilization ratio negatively impacts your credit score. Lenders see a consistently high balance as a sign of potential financial distress. Keeping your balances low relative to your credit limits signals to credit bureaus and potential lenders that you are a responsible borrower who manages their credit effectively.

Affecting Your Financial Flexibility

A substantial credit card balance can significantly curtail your financial flexibility, limiting your ability to handle unexpected expenses or pursue financial goals.

Reduced Purchasing Power

When you carry a large balance, a significant portion of your available credit is already utilized. This reduces your capacity to make new purchases, especially for larger items or during emergencies. It can also mean that you are paying more in interest than you are spending on new goods and services, effectively diminishing the value of your spending.

Increased Debt Burden

A growing credit card balance translates into a growing debt burden. This can lead to a cycle of debt where you are primarily making minimum payments that barely cover the interest, leading to the principal balance barely decreasing. This persistent debt can create significant financial stress and divert funds from other important financial goals like saving, investing, or debt reduction on other loans.

Strategies for Managing Your Credit Card Balance Effectively

Proactive and strategic management of your credit card balances is essential for maintaining financial health and achieving your financial objectives. Several proven strategies can help you stay in control.

Paying More Than the Minimum

While making only the minimum payment on your credit card statement is the easiest way to avoid late fees, it’s often the most expensive and least effective method for long-term financial health. The minimum payment is typically a small percentage of your balance, often covering mostly interest and a very small portion of the principal.

The Dangers of Minimum Payments

Carrying a balance and only paying the minimum can lead to paying significantly more in interest over the life of the debt. For example, a $5,000 balance at 18% APR, with a minimum payment of 2% of the balance, could take over 20 years to pay off and cost more than $9,000 in interest alone. This prolonged repayment period not only drains your finances but also keeps your credit utilization high, negatively impacting your credit score.

The Benefits of Paying in Full or Significantly More

The most financially beneficial strategy is to pay your statement balance in full by the due date each month. This ensures you avoid all interest charges and keep your credit utilization low. If paying in full isn’t feasible, aim to pay as much more than the minimum as you possibly can. Even an extra $50 or $100 a month can dramatically reduce the time it takes to pay off your balance and the total interest paid.

Balance Transfer Strategies

Balance transfers can be a powerful tool for managing high-interest credit card debt, but they require careful planning and execution to be truly effective.

Leveraging 0% APR Introductory Offers

Many credit card companies offer 0% introductory APR periods on balance transfers. This allows you to move a balance from a high-interest card to a new card with no interest accruing for a set period, typically 12 to 18 months. This can be an excellent opportunity to pay down the principal aggressively without the added burden of interest charges.

Considerations for Balance Transfers

While attractive, balance transfers are not without their caveats.

- Balance Transfer Fees: Most cards charge a fee for balance transfers, usually 3% to 5% of the transferred amount. Factor this fee into your decision, as it can offset some of the interest savings.

- Introductory Period Length: Be aware of how long the 0% APR period lasts. If you can’t pay off the balance before it expires, you’ll be subject to the card’s standard APR, which might be high.

- New Purchases: Some cards do not offer a 0% APR on new purchases when you have a balance transfer, or they may apply payments first to the lower-interest balance transfer. Understand the card’s specific terms and conditions regarding new purchases.

- Credit Score: You’ll need good to excellent credit to qualify for the best balance transfer offers.

Debt Snowball and Debt Avalanche Methods

These are two popular and effective debt repayment strategies that can help you tackle your credit card balances systematically.

Debt Snowball Method

The debt snowball method involves paying off your smallest balances first, regardless of interest rate, while making minimum payments on all other debts. Once the smallest debt is paid off, you add the amount you were paying towards it to the minimum payment of the next smallest debt. This creates a “snowball” effect, where the amount you’re paying off grows with each debt cleared, providing psychological wins and momentum.

Debt Avalanche Method

The debt avalanche method prioritizes paying off debts with the highest interest rates first, while making minimum payments on all other debts. Once the highest-interest debt is paid off, you redirect all the money you were paying towards it, plus its minimum payment, to the debt with the next highest interest rate. This method is mathematically superior as it saves you the most money on interest over time.

Understanding Your Credit Card Statement

Your credit card statement is a vital document that provides a detailed summary of your account activity for a specific billing period. It’s your primary source of information for understanding your credit card balance and your repayment obligations.

Key Information Found on a Statement

A typical credit card statement will contain several crucial pieces of information:

Billing Period and Due Date

The statement clearly outlines the billing period covered by the statement and the payment due date. This is the date by which you must make at least your minimum payment to avoid late fees and potential damage to your credit score.

Transaction Details

You’ll find a comprehensive list of all transactions that occurred during the billing period. This includes purchases, returns, cash advances, payments received, and any fees or interest charges. Each transaction will typically show the date, merchant name, and amount.

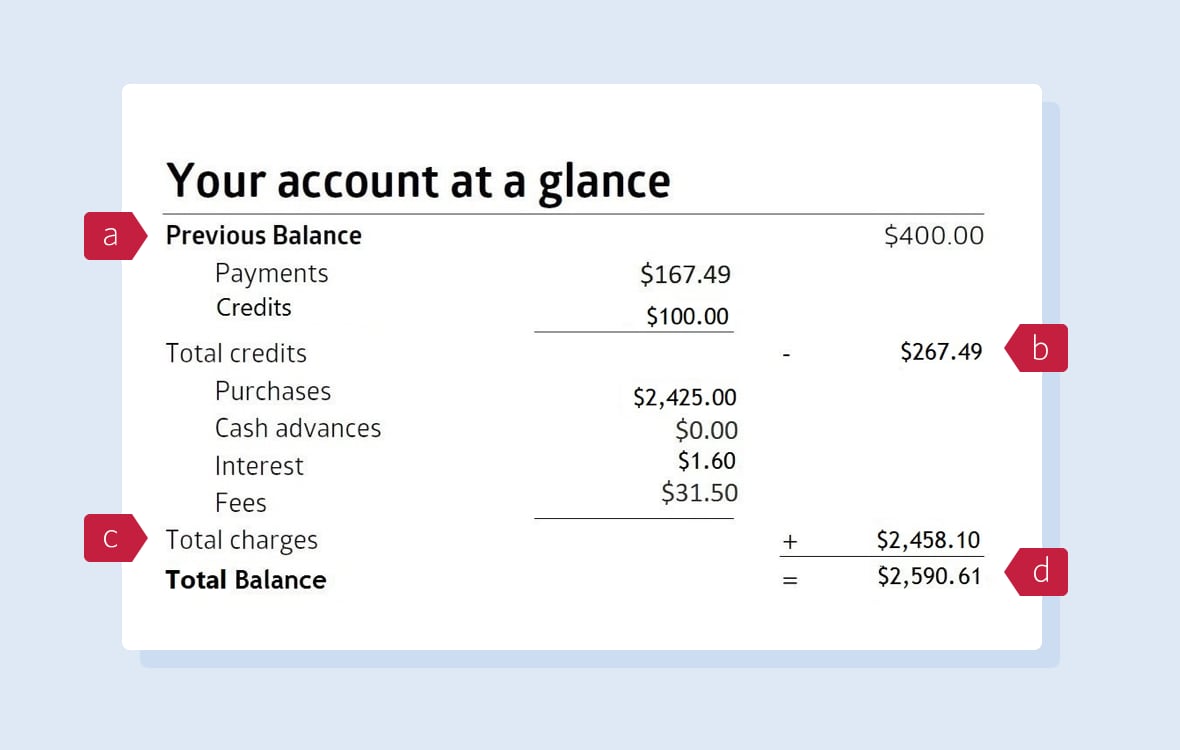

Previous Balance and Payments

Your statement will show the balance from your previous statement, along with any payments you made during the current billing period. This helps you track how your balance has changed.

New Charges

This section details all the new purchases, cash advances, and balance transfers that have been posted to your account during the current billing cycle.

Fees and Interest Charged

Any fees (annual, late, etc.) and the interest charges that have accrued during the billing period are itemized separately. Understanding these charges is crucial for managing your costs.

Statement Balance and Minimum Payment

The statement balance is the total amount you owe as of the closing date of the statement. The minimum payment required is also clearly indicated. This is the absolute least amount you need to pay by the due date.

Credit Limit and Available Credit

Your credit limit – the maximum amount you can borrow on the card – and your available credit – your credit limit minus your current balance – are typically displayed. This helps you monitor your credit utilization.

How to Read and Interpret Your Statement for Balance Management

Regularly reviewing your credit card statement is an indispensable habit for effective financial management. It allows you to:

Detect Errors and Fraud

By scrutinizing each transaction, you can quickly identify any unauthorized charges or errors made by the merchant or credit card issuer. Promptly reporting such issues can prevent financial loss and protect your credit.

Track Spending Habits

Your statement provides a clear overview of where your money is going. Analyzing your spending patterns can help you identify areas where you might be overspending and where you can make adjustments to save money or reduce your balance faster.

Monitor Interest and Fees

Understanding the interest and fees charged is crucial. If these amounts are consistently high, it’s a clear signal that you need to implement strategies to pay down your balance more aggressively or explore options to reduce your interest rates.

Plan Your Repayments

Your statement balance and minimum payment are your guideposts for planning your repayment strategy. Use this information to decide how much extra you can afford to pay beyond the minimum and to set realistic goals for paying down your debt.

In essence, a credit card balance is the monetary sum you owe to your credit card issuer. It’s a dynamic figure influenced by your spending, borrowing habits, and fees. Mastering the concept of a credit card balance, understanding its components, and implementing effective management strategies are vital steps towards achieving financial stability and making your credit cards work for you, rather than against you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.