When the news cycle begins to buzz with reports of central banks cutting interest rates, most homeowners immediately check their mortgage statements. However, for the millions of people currently financing a vehicle, the question is equally pressing: what happens to my car loan if interest rates drop?

In the world of personal finance, interest rates are the “price” of money. When that price falls, it creates a ripple effect across all credit products. Understanding how these macroeconomic shifts translate to your monthly car payment—and your overall financial health—is essential for any savvy borrower. While a drop in market rates does not always result in an automatic reduction in your debt, it opens a window of opportunity to optimize your liabilities and potentially save thousands of dollars over the life of your loan.

Understanding the Impact of Interest Rate Fluctuations on Existing Loans

The immediate impact of a rate drop depends entirely on the structure of the contract you signed when you drove your car off the lot. Most consumers assume that a “market rate” drop applies to all debt instantly, but the reality is governed by the specific terms of your promissory note.

Fixed-Rate vs. Variable-Rate Car Loans

The vast majority of automotive loans in the current market are fixed-rate loans. As the name suggests, a fixed-rate loan locks in your interest rate for the entire duration of the term—whether that is 36, 60, or 72 months. If you have a fixed-rate loan and market interest rates drop, nothing happens to your current loan automatically. You will continue to pay the same interest rate and the same monthly payment as before.

In contrast, variable-rate car loans (though less common) are tied to a benchmark index, such as the Prime Rate. If market rates decline, the interest rate on a variable loan will decrease accordingly, leading to either a lower monthly payment or a faster reduction in your principal balance. While these offer immediate benefits in a falling-rate environment, they also carry the risk of increasing your costs when rates rise.

Why Your Monthly Payment Might Not Change Automatically

If you are holding a fixed-rate loan, your lender is under no legal obligation to lower your rate just because the central bank adjusted its policy. From the lender’s perspective, they have already secured the capital to fund your loan at a specific cost. For the borrower, this means that capitalizing on a rate drop requires proactive action rather than passive waiting. To benefit from lower rates, you generally have to “replace” your old, expensive debt with new, cheaper debt—a process known as refinancing.

The Strategic Opportunity for Refinancing

Refinancing is the primary mechanism through which car owners can take advantage of a cooling interest rate environment. By taking out a new loan with a lower interest rate to pay off the existing one, you essentially “re-buy” your car debt at a discount.

When Does Refinancing Make Financial Sense?

Not every rate drop justifies the paperwork of a refinance. Financial experts generally suggest that a drop of at least 1% to 2% in the interest rate is the threshold where refinancing becomes highly beneficial. However, other factors must be considered. If you are in the final year of a five-year loan, most of your payments are currently going toward the principal rather than interest; in this case, the savings from a lower rate might be negligible compared to any loan origination fees.

Calculating the Break-Even Point

Before proceeding with a refinance, it is vital to calculate the break-even point. This involve comparing the total interest remaining on your current loan against the total interest and fees associated with the new loan. If the new lender charges a high application fee or if your current lender has a “prepayment penalty” (though rare in modern consumer auto loans), these costs could eat into your savings. A successful refinance should either lower your monthly payment or significantly reduce the total interest paid over the life of the loan.

How Refinancing Can Shorten Your Loan Term

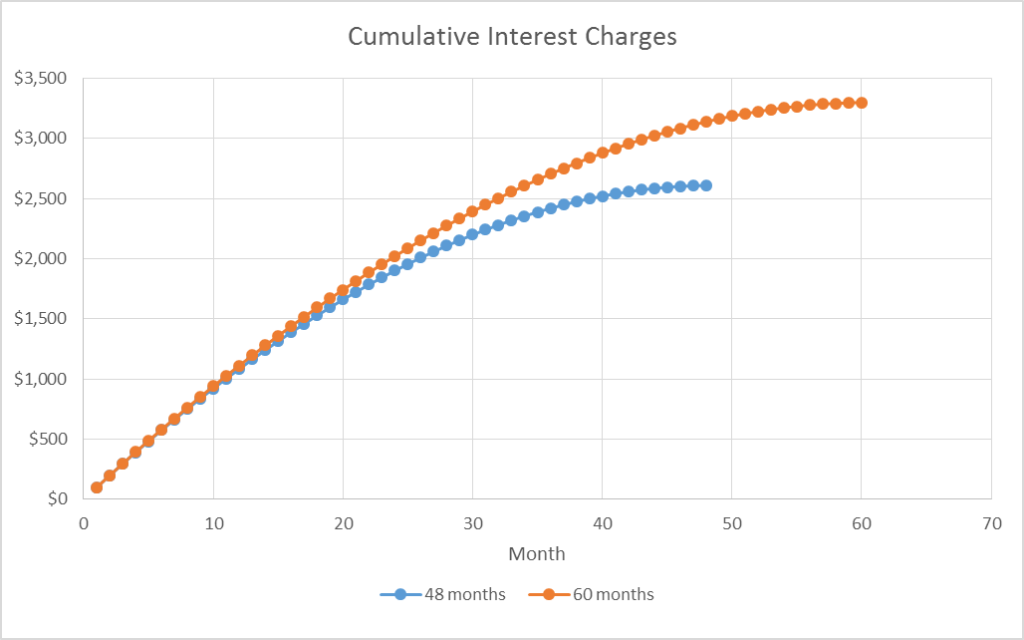

One of the most overlooked benefits of falling rates is the ability to shorten your loan term without increasing your monthly outflow. If rates drop significantly, you may find that you can move from a 60-month loan to a 36-month loan while keeping your payment roughly the same. This allows you to build equity in the vehicle much faster and eliminates debt sooner, freeing up cash flow for other investments or savings goals.

Strategic Moves to Maximize Financial Savings

Beyond simply watching the market, there are several ways to leverage a low-rate environment to improve your overall financial position. Lower rates act as a catalyst, but your personal financial profile remains the most important factor in the deals you can secure.

Leveraging Improved Credit Scores Alongside Lower Rates

If interest rates are dropping at the same time your credit score has improved—perhaps due to a history of on-time car payments or the reduction of credit card debt—you are in a “double-win” situation. Lenders reserve their best rates for those with “prime” or “super-prime” credit scores. Combining a macroeconomic rate cut with an improved personal credit tier can lead to dramatic savings, sometimes cutting an interest rate in half.

Renegotiating with Your Current Lender

While not always successful, it is sometimes possible to renegotiate with your current financial institution. Banks and credit unions are often keen to retain customers rather than losing them to a competitor through a refinance. By presenting them with a lower-rate offer from another bank, you may be able to convince your current lender to modify your existing terms. This “loan modification” can save you the hassle of a full re-titling process while still capturing the benefits of lower market rates.

Using Rate Drops to Pay Down Principal Faster

If market rates drop and you successfully refinance to a lower monthly payment, a disciplined financial strategy is to continue paying the original, higher amount. By paying more than the minimum required on the new, lower-interest loan, the entirety of that “extra” money goes directly toward the principal. This creates a compounding effect of savings, as you are reducing the base amount upon which future interest is calculated.

Market Dynamics and the Psychology of Borrowing

Understanding why rates drop can help you predict how long the window of opportunity will remain open. Interest rates are often adjusted by central banks to stimulate economic growth. When it becomes cheaper to borrow, consumers are more likely to buy cars, homes, and goods.

How Central Bank Decisions Trickle Down to Auto Lenders

When the Federal Reserve or a similar central body lowers the federal funds rate, it lowers the cost for commercial banks to borrow money. These banks, in turn, lower the rates they charge consumers to stay competitive. However, auto loan rates are also influenced by the bond market and the “yield curve.” Sometimes, auto lenders may be slower to drop their rates than mortgage lenders, or they may tighten their lending standards if they believe a rate drop is a sign of a looming recession.

Avoid the Trap: Lower Rates Doesn’t Mean You Should Buy “More Car”

A common psychological pitfall in a low-interest-rate environment is the “payment-focused” trap. When rates drop, a $500 monthly payment can suddenly finance a $40,000 car instead of a $35,000 car. Many consumers use rate drops as an excuse to upgrade to a more expensive vehicle rather than using the savings to improve their balance sheet. From a wealth-building perspective, the goal should be to pay the least amount of interest possible for the utility of the vehicle, rather than maximizing the luxury of the vehicle for a fixed monthly cost.

The Step-by-Step Guide to Responding to Rate Cuts

If you believe the current economic climate is favorable for your car loan, you should follow a structured approach to ensure you aren’t leaving money on the table.

Step 1: Monitor the Market and Your Current Terms

Always keep a copy of your current loan agreement handy. You need to know your current APR (Annual Percentage Rate), your remaining balance, and how many months are left. Use online financial tools and calculators to track “average auto loan rates” for your credit tier. When the gap between your rate and the market rate exceeds 1%, it is time to act.

Step 2: Evaluate Your Current Equity

Before applying for a new loan, determine if you are “upside down” (owing more than the car is worth). Lenders are often hesitant to refinance a vehicle with negative equity unless you can pay the difference upfront. Check valuation sites like Kelley Blue Book or Edmunds to see where your car stands. If you have positive equity, you are a much more attractive candidate for a low-rate refinance.

Step 3: Compare Offers and Watch the Fees

Don’t just go to your local bank. Check credit unions, which often offer the most competitive rates on auto loans because they are member-owned. Compare the “Effective Interest Rate,” which includes any fees. Once you find a deal that lowers your total cost of ownership, lock it in. In a fluctuating economy, the “best” rate is often a moving target; when the math works in your favor, it is better to execute the plan than to wait for a hypothetical bottom that may never come.

By staying informed and being proactive, a drop in interest rates becomes more than just a headline—it becomes a strategic tool to reduce your debt and accelerate your journey toward financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.