Securing a mortgage loan is often the most significant financial undertaking for individuals and families, representing the gateway to homeownership. It’s a multi-faceted process that can seem daunting, but with a clear understanding of the steps involved, careful preparation, and the right guidance, it becomes an achievable goal. This comprehensive guide will demystify the journey, offering practical advice from initial financial assessment to the final closing, ensuring you’re well-equipped to navigate the complexities of obtaining a home loan.

Understanding the Mortgage Landscape

Before embarking on your home buying journey, it’s crucial to grasp the fundamental concepts and players within the mortgage industry. A solid foundation of knowledge will empower you to make informed decisions and better understand the advice you receive from financial professionals.

What is a Mortgage?

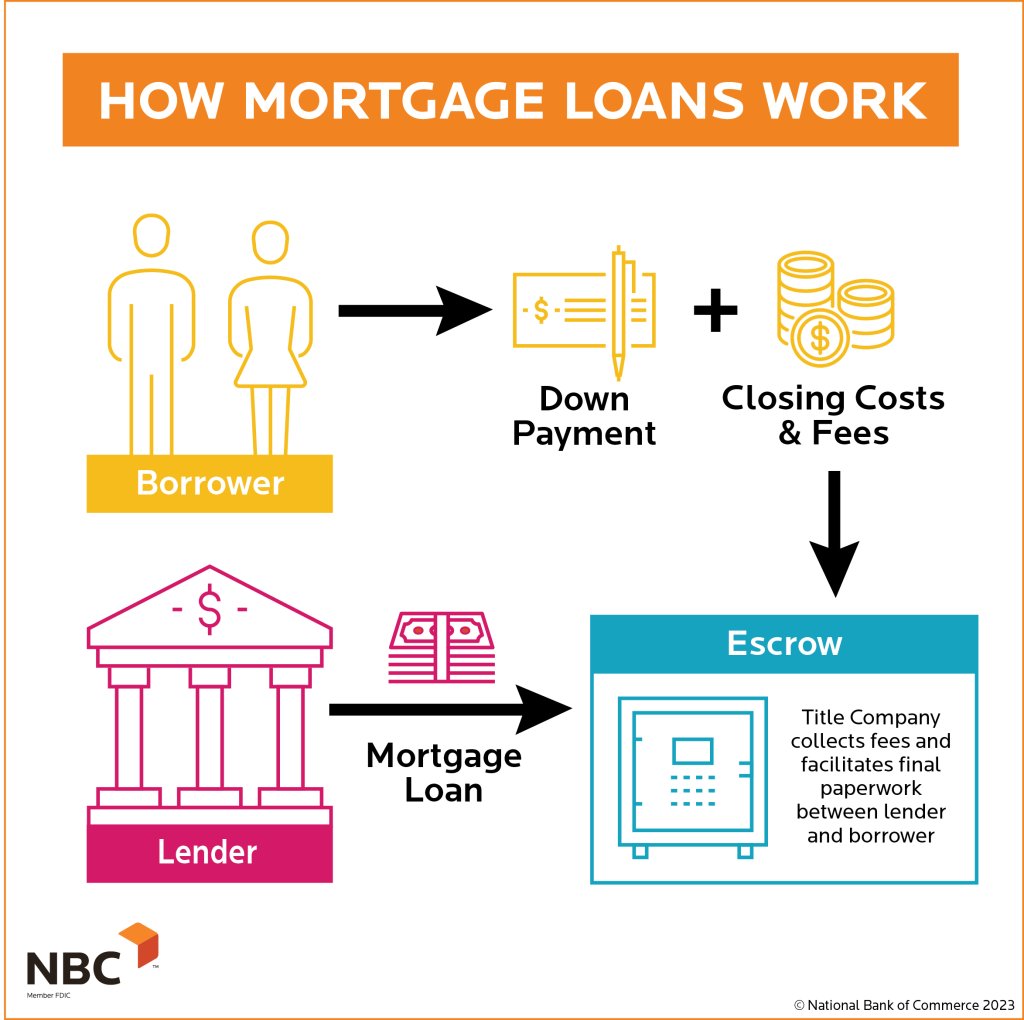

At its core, a mortgage is a loan specifically used to purchase real estate. Unlike other types of loans, a mortgage is secured by the property itself, meaning if you fail to repay the loan, the lender has the right to repossess the property (foreclosure). Mortgages typically involve large sums of money, lengthy repayment periods (commonly 15 or 30 years), and come with interest, which is the cost of borrowing the money. Your monthly payment will usually include principal (the amount borrowed), interest, property taxes, and homeowner’s insurance (often held in an escrow account).

Types of Mortgage Loans

The mortgage market offers a variety of loan products, each designed to meet different financial situations and needs. Understanding these types is key to selecting the right one for you:

- Conventional Loans: These are loans not backed by a government agency. They often require a good credit score and a down payment of at least 3-5%, though 20% is ideal to avoid Private Mortgage Insurance (PMI). They are typically more flexible for those with strong financial profiles.

- Fixed-Rate Mortgages (FRM): The interest rate remains constant for the entire life of the loan. This provides predictable monthly payments, making budgeting easier and protecting against rising interest rates.

- Adjustable-Rate Mortgages (ARM): The interest rate is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a market index. ARMs typically start with lower interest rates than FRMs but carry the risk of higher payments if rates increase.

- FHA Loans: Insured by the Federal Housing Administration (FHA), these loans are popular for first-time homebuyers or those with lower credit scores. They allow for a down payment as low as 3.5% and have more lenient credit requirements, though they require Mortgage Insurance Premiums (MIP) for the life of the loan.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs (VA), these loans are available to eligible veterans, active-duty service members, and surviving spouses. They offer significant benefits, including no down payment requirements and no private mortgage insurance.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans help low-to-moderate-income individuals purchase homes in eligible rural areas. They also offer zero-down payment options for qualified borrowers.

Key Players in the Mortgage Process

Navigating the mortgage process involves interaction with several professionals:

- Lenders: Financial institutions (banks, credit unions, online lenders) that provide the loan. They set the terms, rates, and approval criteria.

- Mortgage Brokers: Intermediaries who work with multiple lenders to help you find the best loan product and rate for your situation. They can simplify the shopping process but charge a fee.

- Loan Officers: Representatives of a specific lender who guide you through their institution’s loan options and application process.

- Underwriters: The professionals who review your application, financial documents, and the property appraisal to assess risk and make the final approval decision.

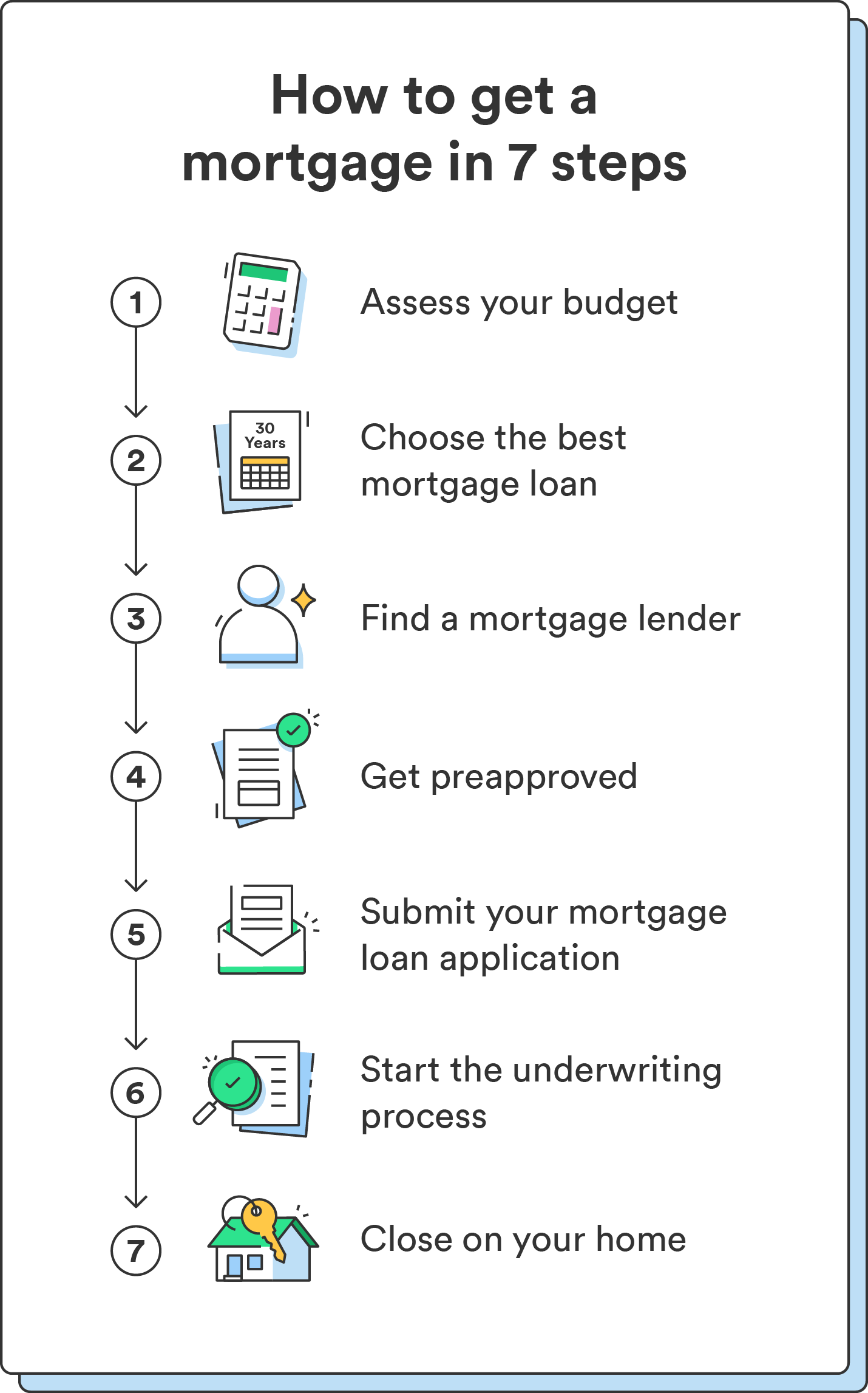

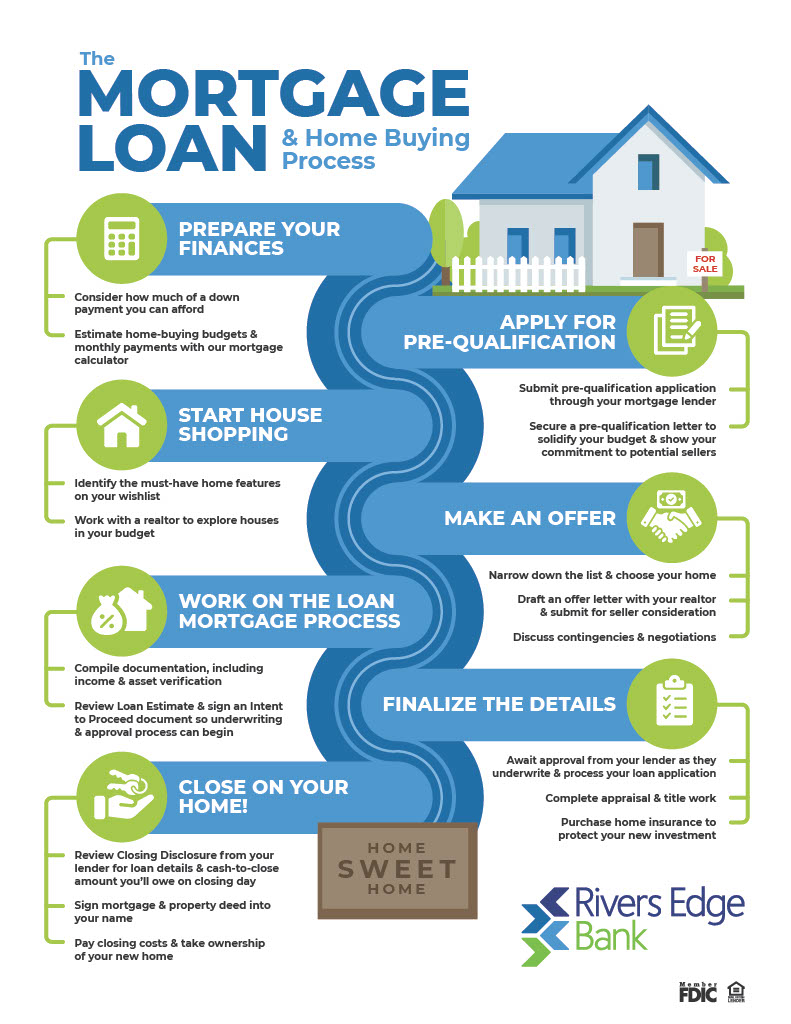

Preparing for Your Mortgage Application

Preparation is paramount when seeking a mortgage. Lenders scrutinize your financial history and current standing to determine your eligibility and the terms they’re willing to offer. The more diligently you prepare, the smoother your application process will be and the better rates you’re likely to secure.

Assessing Your Financial Health

Before approaching any lender, take a hard look at your own financial situation. This self-assessment will help you understand where you stand and what areas might need improvement:

- Credit Score: Your credit score is a numerical representation of your creditworthiness. Lenders use it to gauge your reliability in repaying debts. Generally, a higher score (e.g., 740 and above) qualifies you for the best interest rates. Review your credit reports from all three major bureaus (Equifax, Experian, TransUnion) for accuracy and dispute any errors.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments (credit cards, car loans, student loans, etc.) to your gross monthly income. Most lenders prefer a DTI ratio below 43%, though some government-backed loans might allow for higher. A lower DTI indicates you have more disposable income to cover mortgage payments.

- Savings and Down Payment: Having a substantial down payment reduces the loan amount and can often lead to better interest rates. While some loans allow for low or no down payments, a larger down payment demonstrates financial stability and reduces your monthly principal and interest payments. Beyond the down payment, ensure you have sufficient savings for closing costs (typically 2-5% of the loan amount) and an emergency fund.

Gathering Essential Documents

The mortgage application requires a substantial amount of documentation to verify your income, assets, and liabilities. Proactively collecting these items will streamline your application:

- Proof of Income: Pay stubs (last 30-60 days), W-2 forms (past two years), and if self-employed, tax returns (past two years) and profit & loss statements.

- Asset Information: Bank statements (last two months) for checking and savings accounts, investment account statements, and retirement account statements.

- Debt Information: Statements for credit cards, auto loans, student loans, and any other outstanding debts.

- Identification: Government-issued photo ID (driver’s license, passport) and Social Security card.

- Housing History: Current lease agreement, names and contact information for landlords (if renting), or mortgage statements (if you currently own).

Pre-Approval vs. Pre-Qualification

These terms are often used interchangeably but have distinct meanings:

- Pre-qualification: A preliminary estimate of how much you might be able to borrow. It’s based on a brief review of your finances, often without pulling a credit report, and offers a general idea of affordability. It’s a useful starting point but not a commitment from a lender.

- Pre-approval: A much more robust process where a lender performs a thorough review of your financial information, including a hard credit check, and issues a conditional commitment to lend you a specific amount. A pre-approval letter strengthens your offer to sellers, showing you’re a serious and qualified buyer. Always aim for pre-approval before seriously house hunting.

Navigating the Application and Approval Process

Once you’re pre-approved and have a strong understanding of your financial standing, the real work of finding a lender and securing your loan begins. This phase involves meticulous comparisons, careful submission, and a period of detailed scrutiny by the lender.

Shopping for Lenders and Comparing Offers

Do not settle for the first offer you receive. Interest rates and fees can vary significantly between lenders, potentially saving you tens of thousands of dollars over the life of the loan.

- Gather Quotes: Contact at least three to five different lenders (banks, credit unions, mortgage brokers, online lenders). Provide them with the same information to ensure an apples-to-apples comparison.

- Compare Loan Estimates: Lenders are required to provide a “Loan Estimate” form within three business days of receiving your application. This document details the interest rate, monthly payment, closing costs, and other loan terms. Pay close attention to the Annual Percentage Rate (APR), which includes the interest rate plus certain fees, giving a more complete picture of the loan’s cost.

- Ask Questions: Don’t hesitate to ask about origination fees, discount points, prepayment penalties, and any other charges. Understand what happens if interest rates change before closing (locking in a rate).

- Consider a Mortgage Broker: If you find the comparison process overwhelming, a reputable mortgage broker can shop on your behalf and present you with various options.

Submitting Your Application

Once you’ve chosen a lender, you’ll formally submit your full mortgage application. This involves filling out detailed forms and submitting all the previously gathered documentation. Ensure all information is accurate and complete to avoid delays. The lender will then initiate a “hard inquiry” on your credit report, which will temporarily lower your score by a few points.

The Underwriting Stage

This is where the lender thoroughly vets your application. The underwriter’s job is to assess the risk of lending to you. They will:

- Verify Information: Cross-reference all your submitted documents—income, assets, debts, and credit history—to ensure consistency and accuracy.

- Assess Risk: Evaluate your ability to repay the loan based on your DTI, credit score, employment stability, and cash reserves.

- Review Property Details: Ensure the property itself meets lending standards.

This stage can involve requests for additional documents or clarifications, so be responsive to your lender’s inquiries.

Appraisal and Inspection

Parallel to underwriting, two critical evaluations of the property will take place:

- Appraisal: An independent appraiser determines the market value of the home. Lenders will typically only loan up to the appraised value, or the purchase price, whichever is lower. If the appraisal comes in lower than the agreed-upon purchase price, you may need to renegotiate with the seller or bring more cash to closing.

- Inspection: While not directly tied to the loan approval, a home inspection is crucial for your protection. A professional inspector examines the property’s structural and mechanical components for defects or potential issues. This allows you to identify significant problems before closing and potentially negotiate repairs or a price reduction with the seller.

Closing on Your Home Loan

The closing phase is the culmination of your efforts, where ownership of the home is transferred, and the mortgage loan is finalized. It’s a significant event, but understanding the final steps can help alleviate stress.

Understanding Closing Costs

Closing costs are fees associated with the mortgage transaction, distinct from your down payment. These can range from 2% to 5% of the loan amount and include:

- Lender Fees: Origination fees, underwriting fees, application fees.

- Third-Party Fees: Appraisal fees, inspection fees, title insurance, attorney fees, recording fees, survey fees.

- Prepaid Items: Escrow deposits for property taxes and homeowner’s insurance premiums for the first year.

It’s important to budget for these expenses in addition to your down payment.

The Closing Disclosure

Three business days before your closing date, your lender is legally required to provide you with a “Closing Disclosure” (CD). This document is a final breakdown of all loan terms, fees, and costs. It’s imperative to compare this CD with your initial Loan Estimate to ensure there are no unexpected changes or discrepancies. If you find any significant differences, discuss them immediately with your lender or real estate agent. This three-day window is a crucial time for review and clarification.

Final Walkthrough and Signing Day

- Final Walkthrough: Conduct a final walkthrough of the property, typically 24-48 hours before closing. This is to ensure that the home is in the agreed-upon condition, any negotiated repairs have been made, and no new damage has occurred.

- Signing Day: The closing ceremony itself involves signing a substantial stack of documents. These include the promissory note (your promise to repay the loan), the mortgage or deed of trust (giving the lender a lien on the property), and numerous disclosures. Bring a government-issued photo ID and be prepared for potential wire transfers or cashier’s checks for remaining funds. Once all documents are signed, funds are disbursed, and the deed is recorded, you officially become a homeowner!

Post-Mortgage Responsibilities

Obtaining a mortgage is a monumental achievement, but it also marks the beginning of a long-term financial commitment. Understanding your ongoing responsibilities is key to maintaining your homeownership and financial health.

Making On-Time Payments

This is the most critical responsibility. Your mortgage payment is typically due on the first of each month, with a grace period before late fees are assessed. Consistent, on-time payments are essential for maintaining a good credit score and avoiding penalties or, in severe cases, foreclosure. Many lenders offer automatic payment options, which can help ensure you never miss a payment.

Escrow Accounts and Property Taxes/Insurance

Many mortgages include an escrow account, which is a separate account managed by your lender. A portion of your monthly mortgage payment goes into this account to cover your property taxes and homeowner’s insurance premiums. The lender then pays these bills on your behalf when they are due. This simplifies budgeting for these large annual or semi-annual expenses. It’s important to understand that your escrow payment can adjust annually based on changes in your property tax assessment or insurance premiums, which can cause your total monthly payment to fluctuate.

Refinancing Considerations

As market conditions and your personal financial situation evolve, you might consider refinancing your mortgage. Refinancing involves replacing your current mortgage with a new one, often to:

- Lower Your Interest Rate: If interest rates have fallen since you took out your original loan.

- Reduce Your Monthly Payment: By extending the loan term or securing a lower rate.

- Change Loan Type: Switching from an ARM to a fixed-rate mortgage for stability.

- Cash-Out Refinance: Tapping into your home equity to fund other financial needs, such as home improvements or debt consolidation.

Refinancing involves similar application and closing processes as your original mortgage, including closing costs, so it’s essential to analyze whether the benefits outweigh the costs.

Getting a mortgage loan is a journey that demands patience, diligence, and informed decision-making. By understanding the types of loans available, preparing your finances thoroughly, diligently shopping for the best terms, and meticulously navigating the closing process, you can confidently secure the financing needed to realize your dream of homeownership. Remember, this is a long-term commitment, and ongoing financial discipline will ensure your mortgage remains a stepping stone to financial stability and wealth building.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.