Deciding on the “right” mortgage amount is one of the most critical financial decisions you’ll ever make. It’s not just about what a lender is willing to offer; it’s about what you can comfortably afford, not just now, but for the foreseeable future. A mortgage is a long-term commitment, often spanning 15, 20, or even 30 years, and it will be the largest regular expense for most homeowners. Overextending yourself can lead to financial stress, limit your ability to save, invest, or enjoy other life experiences, and even put your homeownership at risk. Conversely, being too conservative might mean missing out on a suitable property or desirable neighborhood. This guide will walk you through the essential considerations, metrics, and strategies to help you determine an optimal mortgage amount that aligns with your financial health and lifestyle aspirations.

Understanding the Foundations of Mortgage Affordability

Before diving into complex calculations, it’s crucial to establish a solid understanding of your current financial landscape and broader life goals. This foundational step helps differentiate between what you could technically borrow and what you should realistically commit to.

Differentiating Between “Can Afford” and “Should Afford”

Lenders assess your borrowing capacity primarily based on your income, credit score, and existing debts. Their primary concern is whether you’ll be able to make your monthly payments, ensuring their investment is secure. However, what a lender approves you for might push you to the very limits of your financial capacity. “Should afford,” on the other hand, factors in your lifestyle, savings goals, discretionary spending, and unexpected expenses. It’s about maintaining a comfortable financial life after your mortgage payment, rather than living paycheck to paycheck for the sake of homeownership. This distinction is paramount for long-term financial well-being.

The Importance of a Comprehensive Budget Analysis

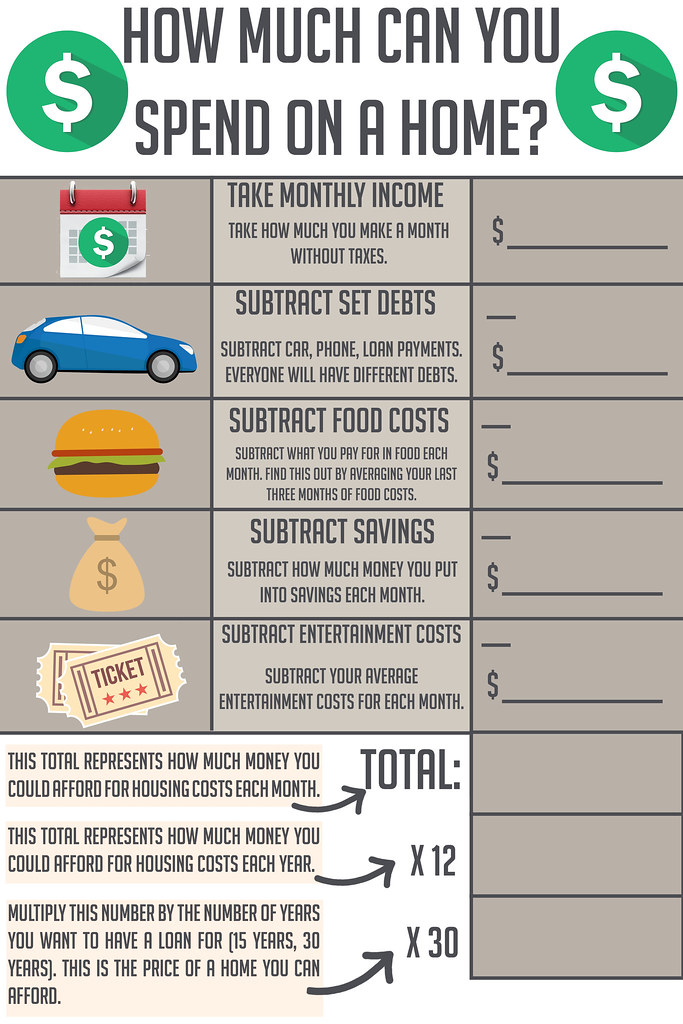

The cornerstone of determining your ideal mortgage amount is a meticulous budget analysis. Before even speaking to a lender, you need a clear picture of your monthly income versus your monthly expenses.

- Income: Detail all sources of stable, verifiable income.

- Fixed Expenses: List recurring, non-negotiable costs like existing loan payments (car loans, student loans), insurance premiums, utilities, and subscriptions.

- Variable Expenses: Track flexible spending like groceries, dining out, entertainment, and personal care.

- Savings: Don’t forget to factor in your current savings contributions for retirement, emergencies, or other goals.

A thorough budget will reveal your true discretionary income – the amount genuinely available for a mortgage payment without compromising other financial priorities or leading to excessive belt-tightening. This exercise should be rigorous, perhaps even tracking every dollar spent for a month or two to uncover hidden spending patterns.

Understanding Your Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a critical metric lenders use, but it’s equally important for your self-assessment. It represents the percentage of your gross monthly income that goes towards debt payments. There are two types:

- Front-End DTI (Housing Ratio): This calculates your proposed monthly housing costs (PITI – Principal, Interest, Taxes, and Insurance) as a percentage of your gross monthly income. Lenders typically prefer this to be no higher than 28%.

- Back-End DTI (Total Debt Ratio): This includes all your monthly debt obligations – PITI, credit card minimums, car loans, student loans, etc. – as a percentage of your gross monthly income. Most lenders look for this to be at or below 36%, though some programs may allow up to 43-50% for highly qualified borrowers.

While lenders might approve higher DTI ratios, aiming for lower percentages provides a greater buffer against financial shocks and allows for more financial flexibility. A DTI below 36% for your total obligations is generally considered a healthy target for long-term financial stability.

Key Metrics and Rules of Thumb for Mortgage Sizing

With your foundational understanding in place, you can now apply specific financial metrics and widely accepted rules of thumb to narrow down your optimal mortgage range. These guidelines offer valuable starting points but should always be considered alongside your unique circumstances.

The 28/36 Rule: A Common Guideline Explained

As introduced earlier, the 28/36 rule is a widely used benchmark in personal finance and mortgage lending. It suggests that:

- Your monthly housing expenses (including principal, interest, property taxes, and homeowner’s insurance – PITI) should not exceed 28% of your gross monthly income.

- Your total monthly debt payments (including housing expenses, credit card minimums, car loans, student loans, etc.) should not exceed 36% of your gross monthly income.

For example, if your gross monthly income is $7,000, your PITI should ideally be no more than $1,960 (28% of $7,000), and your total monthly debt payments should not exceed $2,520 (36% of $7,000). While flexible, adhering to this rule significantly reduces your risk of mortgage stress and allows room for other financial goals.

Factor in Your Down Payment: Impact on Loan Size and Equity

The size of your down payment plays a crucial role in determining your mortgage amount and overall financial picture.

- Loan-to-Value (LTV) Ratio: A larger down payment means a lower LTV ratio (the percentage of the home’s value that you’re borrowing). A lower LTV often translates to better interest rates from lenders.

- Private Mortgage Insurance (PMI): If you put down less than 20% of the home’s purchase price, most lenders will require you to pay for Private Mortgage Insurance (PMI). PMI protects the lender in case you default and adds an extra cost to your monthly payment, potentially for years. Saving for a 20% down payment, if feasible, can save you thousands over the life of the loan.

- Equity: A larger down payment immediately gives you more equity in your home, providing a stronger financial cushion from the outset.

Strategically planning your down payment can significantly influence the mortgage amount you need and the overall cost of borrowing.

Calculating Principal, Interest, Taxes, and Insurance (PITI)

Your monthly mortgage payment is not just the principal and interest (P&I) on the loan itself. It almost always includes property taxes (T) and homeowner’s insurance (I), collectively known as PITI. In some cases, especially with less than 20% down, it will also include Private Mortgage Insurance (PMI) or FHA mortgage insurance premiums (MIP).

- Principal: The portion of your payment that reduces the actual loan balance.

- Interest: The cost of borrowing money from the lender.

- Property Taxes: Taxes levied by your local government based on your home’s assessed value. These can vary significantly by location and can increase over time.

- Homeowner’s Insurance: Protects your home and belongings from damage due to fire, theft, natural disasters, etc. This is typically required by lenders.

- PMI/MIP: Additional insurance costs if your down payment is below a certain threshold.

When calculating how much you can afford, you must consider the entire PITI (and PMI/MIP) amount, not just the principal and interest portion, as this is your true monthly housing expense.

The True Cost of Homeownership Beyond the Mortgage Payment

It’s a common mistake to solely focus on the PITI payment. Homeownership comes with numerous other expenses that can quickly add up and impact your budget. These include:

- Closing Costs: Fees paid at the end of a real estate transaction, typically 2-5% of the loan amount.

- Utilities: Heating, cooling, electricity, water, sewer, internet, garbage collection.

- Maintenance and Repairs: Leaky roofs, broken appliances, plumbing issues – experts often recommend budgeting 1-3% of your home’s value annually for these costs.

- Homeowner’s Association (HOA) Fees: If applicable, these are mandatory monthly or annual fees for community amenities and maintenance in shared developments.

- Landscaping: Lawn care, gardening, snow removal.

- Improvements and Upgrades: Desired renovations, new furniture, etc.

Failing to budget for these additional costs can quickly turn an affordable mortgage into an overwhelming financial burden. Always factor in a realistic estimate for these expenditures when determining your true affordability.

Beyond the Numbers: Holistic Factors Influencing Your Mortgage Decision

While financial metrics provide a framework, your personal circumstances, future aspirations, and tolerance for risk play an equally vital role in shaping your ideal mortgage amount. A holistic approach ensures your home serves as an asset, not an anchor.

Lifestyle Considerations and Future Financial Goals

Your mortgage should complement, not dictate, your desired lifestyle.

- Discretionary Spending: Do you value dining out, travel, hobbies, or entertainment? A high mortgage payment could severely limit these activities.

- Family Planning: Are you planning to have children, which will introduce significant new expenses?

- Education: Are you saving for your children’s college education or your own further studies?

- Retirement: A manageable mortgage allows you to consistently contribute to retirement accounts, securing your future.

Consider how a particular mortgage payment will impact your ability to enjoy life today and achieve your long-term personal and financial goals. Sacrificing all enjoyment for a larger house might lead to resentment and financial strain.

Job Stability and Income Consistency

Your employment situation is a significant factor.

- Stable Income: If you have a secure job with a consistent income, you might feel more comfortable with a slightly higher mortgage payment than someone with variable income (e.g., commission-based, freelance) or in a volatile industry.

- Career Growth: Anticipated promotions or salary increases might make a slightly stretched mortgage more palatable, but it’s risky to rely solely on future income that isn’t guaranteed. Base your current affordability on your current income.

- Potential for Layoffs/Job Changes: How would a temporary loss of income impact your ability to make payments?

Assessing your job security and income stability provides a realistic outlook on your capacity to manage a long-term debt obligation.

Emergency Savings and Financial Resilience

Having a robust emergency fund is non-negotiable, especially as a homeowner. Experts recommend having at least 3-6 months’ worth of essential living expenses (including your mortgage payment) in an easily accessible savings account.

- Unexpected Home Repairs: A new roof, a broken water heater, or unexpected plumbing issues can quickly drain savings.

- Job Loss or Income Reduction: An emergency fund provides a critical safety net during periods of unemployment or reduced income.

- Health Issues: Medical emergencies can be financially devastating without adequate savings and insurance.

Prioritize building and maintaining an emergency fund before and after purchasing a home. A mortgage that leaves no room for savings dramatically increases your financial vulnerability.

The Opportunity Cost of a Larger Mortgage

Every dollar committed to a larger mortgage payment is a dollar that cannot be used elsewhere. This is known as opportunity cost.

- Investments: A smaller mortgage payment could free up funds to invest in the stock market, real estate (other than your primary residence), or a business, potentially generating higher returns over time.

- Debt Reduction: It could be used to pay down higher-interest debts like credit cards or student loans, saving you money in interest.

- Lifestyle Enrichment: More disposable income for travel, hobbies, or experiences.

Consider whether a larger home or a faster payoff is truly the best use of your capital compared to other financial avenues that could lead to greater wealth accumulation or personal satisfaction.

Navigating the Mortgage Application Process and Lender Expectations

Once you have a clear internal assessment of what you should afford, the next step is understanding what lenders will offer and how to best position yourself during the application process.

What Lenders Look For: Credit Score, Income, and Assets

Lenders evaluate several key factors to assess your creditworthiness:

- Credit Score: A higher credit score (generally above 740) indicates a lower risk borrower, often qualifying you for the best interest rates. Lenders review your payment history, amounts owed, length of credit history, new credit, and credit mix.

- Income and Employment History: Lenders want to see a stable and consistent income that can reliably cover your mortgage payments. Typically, they require a two-year employment history.

- Assets: Your savings, checking accounts, investment portfolios, and other liquid assets demonstrate your ability to cover the down payment, closing costs, and serve as reserves after the purchase.

- Existing Debt: As discussed, your DTI ratio is a major factor. Lenders want to ensure your existing debt obligations don’t overwhelm your income.

Optimizing these areas before you apply can significantly improve your chances of approval and secure more favorable loan terms.

Pre-Approval vs. Pre-Qualification: Why It Matters

These terms are often used interchangeably, but there’s a significant difference:

- Pre-Qualification: This is an informal estimate based on self-reported financial information. It gives you a general idea of what you might qualify for but is not a commitment from the lender.

- Pre-Approval: This is a much more thorough process where the lender verifies your income, assets, and credit. It results in a conditional commitment from the lender for a specific loan amount up to a certain price, often with an interest rate lock. A pre-approval letter is highly valuable when making an offer on a home, showing sellers you are a serious and qualified buyer.

Always aim for a pre-approval before seriously house hunting. It clarifies your true borrowing power and streamlines the offer process.

Understanding Loan Types and Their Implications

The type of mortgage you choose can significantly impact your monthly payments, interest rates, and overall costs.

- Conventional Loans: The most common type, often requiring good credit and a stable income. Can be fixed-rate or adjustable-rate.

- FHA Loans: Government-insured loans popular for first-time homebuyers or those with lower credit scores. They often have lower down payment requirements but mandate mortgage insurance premiums (MIP) for the life of the loan or until specific conditions are met.

- VA Loans: Offered to eligible service members, veterans, and surviving spouses. These loans often require no down payment and no private mortgage insurance.

- USDA Loans: Designed for rural homebuyers, these also offer zero-down payment options for eligible properties and borrowers.

Each loan type has specific eligibility criteria, benefits, and drawbacks. Researching and discussing these options with a qualified loan officer is crucial to finding the best fit for your financial situation.

Strategic Mortgage Management for Long-Term Financial Health

Once you’ve secured your mortgage, the journey isn’t over. Strategic management of your loan and overall finances can significantly impact your wealth accumulation and financial freedom.

The Benefits of a Smaller, More Manageable Mortgage

Opting for a mortgage that is well below your maximum approved amount offers numerous advantages:

- Reduced Financial Stress: More breathing room in your monthly budget, making it easier to handle unexpected expenses or market fluctuations.

- Increased Savings and Investments: Frees up capital to build your emergency fund, save for retirement, or invest in other opportunities.

- Greater Flexibility: Allows you to pursue career changes, take time off, or invest in education without feeling trapped by a high payment.

- Faster Equity Build-Up: While paying less principal each month, having more disposable income allows you to strategically make additional payments, accelerating equity growth.

A smaller mortgage doesn’t mean a smaller life; it often means a more secure and flexible financial life.

Strategies for Accelerating Mortgage Payoff

If you have a manageable mortgage and extra funds, consider strategies to pay it off faster, saving thousands in interest over time.

- Make Bi-Weekly Payments: Instead of one monthly payment, pay half the amount every two weeks. This results in 13 full monthly payments per year (26 half-payments) instead of 12, effectively making one extra payment annually.

- Round Up Payments: If your payment is $1,475, consider paying $1,500 and directing the extra $25 to the principal.

- Apply Windfalls: Use bonuses, tax refunds, or inheritances to make lump-sum principal payments.

- Refinance to a Shorter Term: If interest rates are favorable and your budget allows, refinancing from a 30-year to a 15-year mortgage significantly reduces total interest paid, though it increases monthly payments.

Each extra dollar directed to principal early in the loan term has a compounding effect, saving substantial interest over decades.

Refinancing: When It Makes Sense

Refinancing involves replacing your current mortgage with a new one, typically to secure a lower interest rate, change the loan term, or access home equity.

- Lower Interest Rates: If rates have dropped significantly since you originated your loan, refinancing can reduce your monthly payment or the total interest paid.

- Shorter Loan Term: As mentioned, refinancing to a 15-year mortgage from a 30-year can save substantial interest.

- Cash-Out Refinance: Allows you to borrow against your home’s equity, providing cash for home improvements, debt consolidation, or other needs. However, this increases your debt and should be approached cautiously.

- Changing Loan Type: Switching from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for stability.

Always weigh the costs of refinancing (closing costs) against the potential savings or benefits. A good rule of thumb is that if you can reduce your interest rate by at least 0.75% to 1% and plan to stay in the home long enough to recoup the closing costs, it might be a worthwhile consideration.

Maintaining Financial Flexibility Post-Purchase

The goal of determining your ideal mortgage amount is to achieve and maintain financial flexibility throughout your homeownership journey. This means:

- Regular Budget Reviews: Revisit your budget annually to account for changes in income, expenses, and financial goals.

- Continual Savings: Prioritize contributing to your emergency fund, retirement accounts, and other savings vehicles.

- Debt Management: Keep other debts (credit cards, personal loans) under control to avoid straining your overall DTI.

- Home Equity Utilization: Understand your home equity as an asset but be judicious about borrowing against it, ensuring it aligns with long-term financial plans.

By taking a thoughtful, comprehensive, and proactive approach to determining and managing your mortgage, you can ensure that your home is a source of joy and financial stability, not stress. It’s about finding that sweet spot where homeownership enriches your life without compromising your broader financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.