The dream of a 4% mortgage rate has become a focal point for aspiring homebuyers and existing homeowners alike, especially after a period of historically low rates followed by a sharp surge. The notion of securing a mortgage at such an appealing rate conjures images of reduced monthly payments, increased purchasing power, and greater financial stability. However, the path to 4% is paved with complex economic indicators, Federal Reserve policies, and global market dynamics. Understanding these forces is crucial for anyone hoping to navigate the future of the housing market.

For much of the 2010s and into the early 2020s, borrowers grew accustomed to a low-rate environment, with mortgage rates often hovering around or even dipping below 4%. The COVID-19 pandemic further pushed rates to historic lows as central banks implemented aggressive monetary easing to stimulate economies. This era, however, proved to be an anomaly rather than a new normal. As inflation soared in 2021 and 2022, the Federal Reserve embarked on an aggressive campaign of interest rate hikes, pulling mortgage rates—which are closely tied to the 10-year Treasury yield and reflect broader market expectations for inflation and economic growth—significantly higher, often into the 6% to 8% range.

This shift has understandably left many in a holding pattern, with prospective buyers delaying purchases and current homeowners contemplating whether to refinance. The question “When will mortgage rates go down to 4%?” isn’t merely about a number; it represents a yearning for greater affordability and a return to what many perceived as a more “normal” housing market. This article will delve into the economic conditions that typically drive mortgage rates, assess the likelihood and timeline for a return to 4%, and offer strategies for consumers to navigate this dynamic financial landscape.

The Economic Levers Pulling Mortgage Rates

Mortgage rates are not set in a vacuum; they are a complex interplay of several powerful economic forces. While the Federal Reserve’s actions are often highlighted, they are part of a larger ecosystem that determines borrowing costs. Understanding these fundamental drivers is the first step toward deciphering the future trajectory of rates.

The Federal Reserve and Monetary Policy

The Federal Reserve directly influences short-term interest rates through the federal funds rate, which is the target rate for overnight lending between banks. While mortgage rates are long-term rates and not directly pegged to the federal funds rate, changes in the Fed’s policy profoundly impact them. When the Fed raises its benchmark rate to combat inflation, it signals a broader tightening of monetary policy. This tightening increases the cost of borrowing across the economy, including for banks, which then pass these higher costs on to consumers in the form of higher mortgage rates. Conversely, when the Fed cuts rates, it aims to stimulate economic activity, typically leading to lower borrowing costs.

Beyond the federal funds rate, the Fed’s stance on quantitative easing (QE) or quantitative tightening (QT) also plays a significant role. During QE, the Fed buys large quantities of government bonds and mortgage-backed securities, injecting liquidity into the market and putting downward pressure on long-term rates. QT involves the Fed shrinking its balance sheet by allowing these assets to mature without reinvestment, effectively removing liquidity and contributing to higher rates.

Inflation Expectations

Perhaps the most critical driver of long-term interest rates, including mortgages, is inflation. Lenders demand a return that not only covers their operational costs and desired profit margin but also compensates them for the erosion of their money’s purchasing power due to inflation over the loan’s term. If lenders expect high inflation in the future, they will demand higher interest rates to ensure the real value of their return isn’t diminished. This is why the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index are closely watched economic indicators. A sustained return to the Fed’s 2% inflation target is widely considered a prerequisite for significantly lower mortgage rates.

The 10-Year Treasury Yield

Mortgage rates, particularly for 30-year fixed-rate mortgages, are highly correlated with the yield on the 10-year U.S. Treasury bond. The 10-year Treasury is considered a benchmark for long-term borrowing costs, reflecting investor expectations about future inflation, economic growth, and the Fed’s monetary policy over the next decade. When the yield on the 10-year Treasury rises, mortgage rates typically follow suit, and vice versa. Factors influencing the 10-year Treasury yield include government borrowing, global economic stability, and investor demand for safe assets.

Economic Growth and Labor Market Data

A strong economy, characterized by robust GDP growth and a tight labor market with low unemployment and rising wages, can put upward pressure on inflation and, consequently, on interest rates. A booming economy might lead the Fed to keep rates higher to prevent overheating. Conversely, signs of economic slowdown or a recession can prompt the Fed to consider rate cuts to stimulate activity, which tends to push long-term rates lower. The monthly jobs report, retail sales figures, and manufacturing indices are all indicators that provide clues about the economy’s health and its potential impact on rates.

The Path to 4%: Conditions and Timelines

Achieving a 4% mortgage rate isn’t a simple matter of time; it requires a specific confluence of economic conditions. While predicting exact timelines is notoriously difficult, we can outline what needs to happen for such a rate to become a widespread reality once again.

Sustained Disinflation Towards the 2% Target

The primary condition for mortgage rates to fall to 4% is a clear and sustained return of inflation to the Federal Reserve’s 2% target. This means not just a few months of declining inflation figures but a consistent trend that convinces the Fed and the markets that inflation is under control and likely to remain so. Once inflation expectations are firmly anchored at a lower level, the “inflation premium” built into long-term rates can begin to shrink. This process is often gradual, and the Fed is unlikely to declare victory prematurely.

Federal Reserve Rate Cuts

Once inflation is demonstrably under control, the Federal Reserve will likely begin to cut the federal funds rate. These cuts signal to the market that the era of tight monetary policy is ending and that the cost of borrowing throughout the economy will decrease. Mortgage rates typically anticipate these cuts, beginning to decline as the market perceives that rate cuts are imminent. However, for rates to drop to 4%, a significant number of rate cuts would be required, suggesting the federal funds rate would need to return to a more “neutral” or even accommodative stance. This could mean several percentage points of cuts from peak rates.

A Cooling, But Not Collapsing, Economy

Paradoxically, some economic softening is often necessary for rates to fall. A moderately slower economy can help curb demand and reduce inflationary pressures. However, a severe recession could also trigger lower rates, as investors flock to safe-haven assets like Treasury bonds, driving their yields down. But a deep recession comes with its own set of economic challenges, including job losses and decreased consumer confidence, which can make homebuying less appealing despite lower rates. The ideal scenario for 4% rates would involve a “soft landing”—where the economy slows enough to tame inflation without entering a severe downturn.

Geopolitical Stability and Market Sentiment

Global events and geopolitical stability also play a role. Major international conflicts or economic crises can lead to a flight to safety, where investors pour money into U.S. Treasury bonds, which can temporarily push down yields and, consequently, mortgage rates. However, prolonged instability can also create uncertainty, making lenders more cautious and potentially keeping rates elevated. Positive market sentiment, driven by confidence in economic policy and future growth, can help stabilize rates and allow them to trend lower in line with fundamentals.

Why 4% Might Be a Distant Horizon (or a Near-Term Possibility)

The question of when 4% rates will return is not just about if but also about the pace and sustainability of such a decline. Different economic philosophies and emerging trends suggest various possibilities.

The “Higher for Longer” Debate

Many economists and Fed officials now believe that the era of ultra-low rates (below 4%) was a unique period unlikely to be replicated soon. They argue that structural shifts in the global economy, such as deglobalization, increased government spending, and the green energy transition, could inherently lead to higher baseline inflation and, consequently, higher “neutral” interest rates. If the neutral federal funds rate is indeed higher than pre-pandemic, then a 4% mortgage rate might require the Fed to cut rates into territory considered “accommodative,” which it would only do during a significant economic downturn. This perspective suggests that average mortgage rates could settle in a 5-6% range rather than returning to 4%.

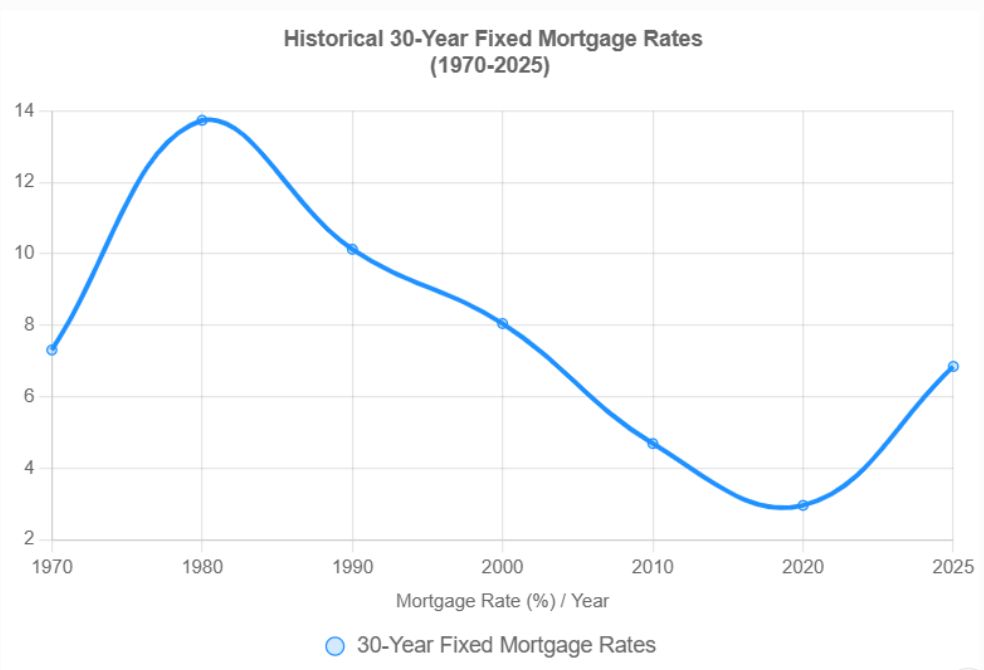

Historical Context and New Normals

Looking at historical data, mortgage rates below 5% were relatively uncommon before the 2008 financial crisis. The period from 2009 to 2021 was an outlier, influenced by massive quantitative easing and an extended period of low inflation and slow growth. It’s plausible that a “new normal” for mortgage rates could be in the 5% to 6.5% range, reflecting a more balanced economic environment where inflation is managed but not completely absent, and growth is steady. Reaching 4% would therefore require either a more severe economic contraction than currently anticipated or a prolonged period of extremely low inflation, perhaps even deflationary pressures, which central banks typically try to avoid.

The Black Swan Event

Of course, unforeseen “black swan” events—such as a new global financial crisis, a severe pandemic, or a significant technological disruption leading to massive productivity gains without inflation—could rapidly alter the economic landscape and force central banks to implement aggressive easing measures, potentially pushing rates down to 4% or even lower. However, these events are by definition unpredictable and often come with significant societal costs.

Strategies for Homebuyers and Homeowners in a Dynamic Market

Given the uncertainties surrounding the return to 4% mortgage rates, what should individuals do today? The best strategy involves focusing on what you can control and making informed financial decisions.

Don’t Try to Time the Market

Attempting to perfectly time the peak of mortgage rates or waiting for an elusive 4% can be a costly mistake. Housing prices, while influenced by rates, also depend on supply, demand, and local market conditions. Waiting indefinitely might mean missing out on opportunities, as even if rates eventually fall, home prices might continue to appreciate, eroding any savings from a lower interest rate. Focus on what is affordable for your current financial situation, rather than gambling on future rate movements.

Focus on Affordability and Financial Health

The most crucial aspect of homeownership is affordability. Assess your budget, calculate what monthly payment you can comfortably afford, and stick to it. Work to improve your credit score, reduce debt, and build a substantial down payment. These actions will not only help you qualify for the best possible rates available at any given time but also build financial resilience regardless of market fluctuations. A lower interest rate is only beneficial if the overall home purchase aligns with your long-term financial goals.

Exploring Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate

In an environment where fixed rates are high but expected to fall, some borrowers consider Adjustable-Rate Mortgages (ARMs). An ARM typically offers a lower initial interest rate for a fixed period (e.g., 5, 7, or 10 years) before adjusting periodically based on an index. If you plan to sell or refinance before the fixed period ends, or if you are confident that rates will drop significantly, an ARM might offer lower initial payments. However, ARMs come with the risk that rates could rise, leading to higher payments later. Carefully weigh the risks and benefits with a mortgage professional.

The Power of Refinancing When Rates Drop

If you purchase a home at a higher fixed rate and rates eventually fall significantly (perhaps even to 4%), refinancing becomes a powerful tool. Refinancing allows you to replace your existing mortgage with a new one at a lower interest rate, reducing your monthly payments and overall interest paid over the life of the loan. Many homeowners adopt a “buy now, refinance later” strategy, securing a home they want and then optimizing their financing when conditions improve. Be mindful of closing costs associated with refinancing, which need to be weighed against the savings.

Working with a Trusted Mortgage Professional

The mortgage market is complex and constantly evolving. Engaging with a knowledgeable and trustworthy mortgage broker or lender is invaluable. They can help you understand the current market, explore different loan products, assess your eligibility, and advise on the best strategy for your unique financial circumstances. They can also keep you informed about potential rate drops and opportunities to refinance.

In conclusion, while the allure of a 4% mortgage rate is strong, its return is contingent upon a specific set of economic conditions, primarily a sustained moderation of inflation and subsequent Federal Reserve rate cuts. The timeline is uncertain, and structural economic shifts might mean that average rates settle higher than the pre-pandemic era. Rather than passively waiting for an ideal rate, a proactive approach focusing on personal financial health, affordability, and strategic planning remains the most prudent course for homebuyers and homeowners alike.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.