The question “What’s the mortgage rate today?” is more than just a search query; it is a pulse check on the global economy and a critical data point for millions of households. Whether you are a first-time homebuyer, a seasoned real estate investor, or a homeowner considering a refinance, the daily fluctuations in interest rates can represent a difference of hundreds of dollars in monthly payments and tens of thousands of dollars over the life of a loan.

In the current economic climate, mortgage rates have moved from the historical lows of the early 2020s into a more volatile, elevated territory. Understanding what drives these numbers is essential for making informed financial decisions. This article explores the mechanics of mortgage rates, the macroeconomic forces that dictate their movement, and the personal financial strategies you can use to secure the best possible terms.

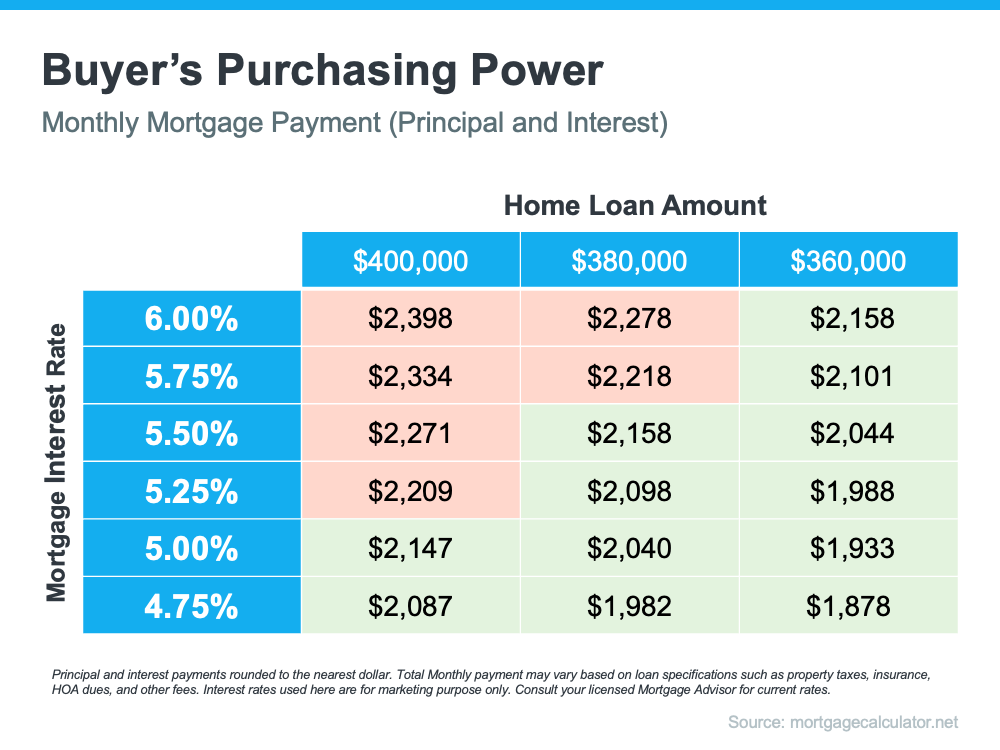

Understanding the Current Landscape of Mortgage Rates

When you see a mortgage rate quoted in the news or on a lender’s website, it is typically an average based on a specific set of criteria—usually a borrower with excellent credit and a 20% down payment. However, “the rate” is not a monolith. It varies significantly based on the type of loan product and the current appetite of the secondary bond market.

The Difference Between the Federal Funds Rate and Mortgage Rates

A common misconception in personal finance is that the Federal Reserve “sets” mortgage rates. While the Fed’s actions certainly influence them, the relationship is indirect. The Federal Funds Rate is the interest rate at which commercial banks borrow and lend to each other overnight. When the Fed raises this rate to combat inflation, it increases the cost of borrowing across the board. However, long-term mortgage rates are more closely tied to the yield on the 10-year Treasury note. If investors anticipate high inflation or economic growth, they demand higher yields, which in turn pushes mortgage rates higher.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

Today’s borrowers generally choose between two primary structures. The 30-year fixed-rate mortgage remains the gold standard for stability, locking in an interest rate for three decades. This is the most sensitive to long-term economic forecasts. On the other hand, Adjustable-Rate Mortgages (ARMs) often offer a lower “teaser” rate for an initial period (such as five or seven years) before adjusting annually based on market indices. In a high-rate environment, ARMs become increasingly popular as borrowers gamble that rates will drop before their adjustment period begins.

Key Factors Influencing Today’s Mortgage Rates

Mortgage rates do not exist in a vacuum. They are the result of a complex interplay between government policy, investor sentiment, and global economic health. To understand why rates are high or low today, one must look at the broader financial horizon.

Economic Indicators and Inflation Data

Inflation is the greatest enemy of fixed-income investments like mortgages. When inflation is high, the purchasing power of the future interest payments a lender receives is eroded. Consequently, when the Consumer Price Index (CPI) or Personal Consumption Expenditures (PCE) reports show rising prices, mortgage rates almost inevitably climb. Lenders must charge more today to offset the devalued dollars they will be paid back tomorrow. Conversely, signs of a “cooling” economy often lead to a stabilization or decrease in rates as the threat of inflation recedes.

The Role of the 10-Year Treasury Yield

Investors often look at the 10-year Treasury yield as a benchmark for mortgage pricing. Historically, there is a “spread” or gap between the 10-year Treasury yield and the average 30-year mortgage rate, typically around 1.5 to 2 percentage points. This spread accounts for the risks associated with mortgages, such as the risk of default or the risk that the borrower will prepay the loan (refinance) when rates drop. In times of economic uncertainty or high volatility, this spread can widen, meaning mortgage rates may stay high even if Treasury yields begin to fall.

Global Geopolitical Stability

The financial markets are global. In times of international conflict or economic instability abroad, investors often seek “safe-haven” assets. U.S. Treasuries are considered among the safest assets in the world. When global demand for Treasuries increases, their prices go up and their yields go down. Because mortgage rates track these yields, geopolitical turmoil can ironically lead to a temporary dip in mortgage rates in the United States, as a flood of global capital enters the American bond market.

How Personal Financial Health Affects the Rate You Are Offered

While the “market rate” provides a baseline, your personal financial profile determines the “effective rate” a lender will actually offer you. In the world of money and lending, risk is priced into every contract.

The Power of the Credit Score

Your credit score is perhaps the single most influential factor in the mortgage application process. Lenders use FICO scores to categorize borrowers into risk tiers. A borrower with a score above 760 will likely receive the lowest available market rate. However, a borrower with a score in the mid-600s might face a rate that is 1% to 1.5% higher. Over a 30-year loan on a $400,000 home, that 1% difference can cost the borrower over $100,000 in additional interest. Maintaining a clean credit history and low credit utilization is the most effective way to “buy down” your rate without spending a dime.

Debt-to-Income (DTI) Ratios and Down Payments

Lenders also look closely at your Debt-to-Income ratio—the percentage of your gross monthly income that goes toward paying debts. A lower DTI suggests you have the financial “breathing room” to handle a mortgage payment, making you a lower-risk borrower. Similarly, the size of your down payment changes the Loan-to-Value (LTV) ratio. A 20% down payment removes the need for Private Mortgage Insurance (PMI) and signals to the lender that you have significant “skin in the game,” which can often lead to more favorable interest rate pricing.

Strategies for Timing Your Mortgage and Securing the Best Deal

Because mortgage rates can change multiple times in a single day, the strategy you employ during the “lock-in” phase of your home purchase is vital.

To Lock or to Float?

Once you have an accepted offer on a home, you face a choice: lock in the current rate or “float” it. A rate lock guarantees your interest rate for a specific period (usually 30 to 60 days) while your loan is processed. If rates rise during that time, you are protected. If you choose to float, you are betting that rates will decrease before you close. Given the current volatility in the bond market, most financial advisors recommend locking in a rate as soon as you are comfortable with the monthly payment, as the risk of a sudden spike often outweighs the potential benefit of a minor dip.

The Importance of Shopping Around and Comparing Loan Estimates

Many borrowers make the mistake of only checking with their primary bank. However, mortgage pricing is highly competitive. Different institutions—credit unions, national banks, and independent mortgage brokers—have different overhead costs and “appetites” for new loans. By obtaining a Loan Estimate (a standardized three-page document) from at least three different lenders, you can compare not only the interest rate but also the closing costs and origination fees. Small differences in these fees can significantly impact the “Annual Percentage Rate” (APR), which represents the true cost of the loan.

Long-Term Outlook: What to Expect from the Housing Market

Looking toward the future, the “normal” for mortgage rates is being redefined. For nearly a decade following the 2008 financial crisis, the world experienced artificially low rates. As we move further into the mid-2020s, the “Money” niche suggests a return to historical averages, which typically hover between 5% and 7%.

For prospective buyers, the strategy should shift from “waiting for 3% rates” to “buying when the math works.” Real estate is a long-term investment. If you purchase a home at a 7% rate and rates eventually drop to 5%, you can refinance and lower your payment. If rates continue to climb to 9%, you will be glad you secured 7%.

In conclusion, while the answer to “what’s the mortgage rate today” is a moving target, your ability to navigate it depends on your understanding of the broader economy and your preparation as a borrower. By monitoring inflation data, maintaining an elite credit score, and shopping aggressively among lenders, you can ensure that you are not just a passenger in the market, but an active participant in your own financial future. High rates may change the “how” of home buying, but they don’t change the “why”—building equity and securing a foundation for personal wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.