Navigating the landscape of personal finance often requires learning a new language. Among the most common yet frequently misunderstood terms in the world of revolving credit are “current balance” and “statement balance.” While they may appear similar at a glance, the distinction between these two figures is the cornerstone of effective debt management, interest avoidance, and credit score optimization.

Understanding what your current balance represents is not merely an academic exercise; it is a practical necessity for anyone looking to maintain financial health. In this guide, we will break down the mechanics of the current balance, explore its impact on your financial standing, and provide strategies for managing your credit card accounts with professional precision.

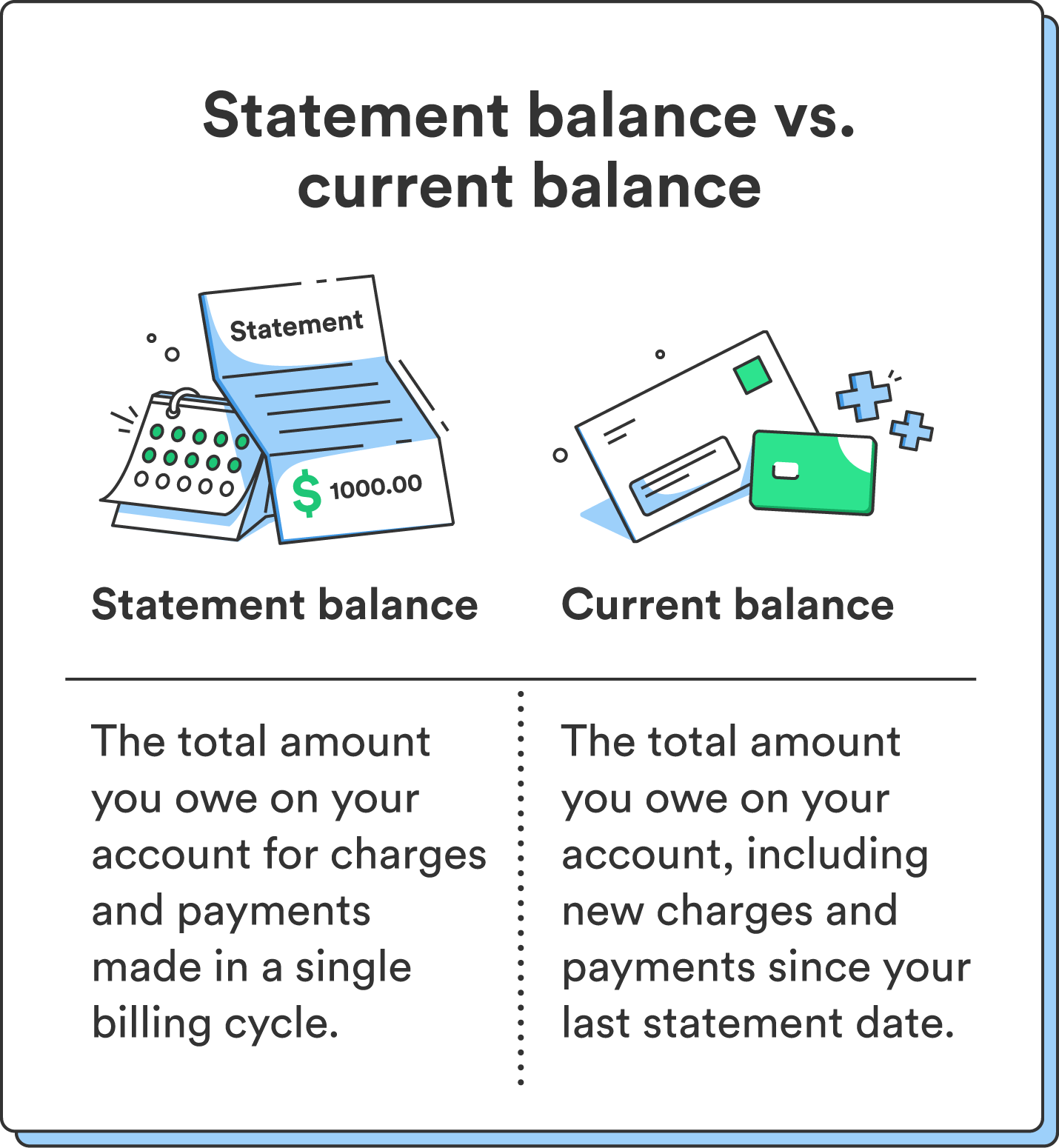

Decoding the Difference: Current Balance vs. Statement Balance

At its simplest, your credit card balance represents the total amount of money you owe the card issuer at any given moment. However, because credit cards are dynamic accounts with transactions occurring daily, lenders use different “snapshots” of this debt for different purposes.

Defining the Current Balance

The current balance is a real-time (or near real-time) reflection of your total indebtedness to the credit card company. It includes every transaction that has been fully processed and posted to your account up to the present second. This includes purchases, balance transfers, cash advances, interest charges, and fees, minus any payments or credits you have made.

If you were to decide today that you wanted to pay off your credit card in its entirety to stop using it, the current balance is the number you would look at. It is the “living” total of your debt.

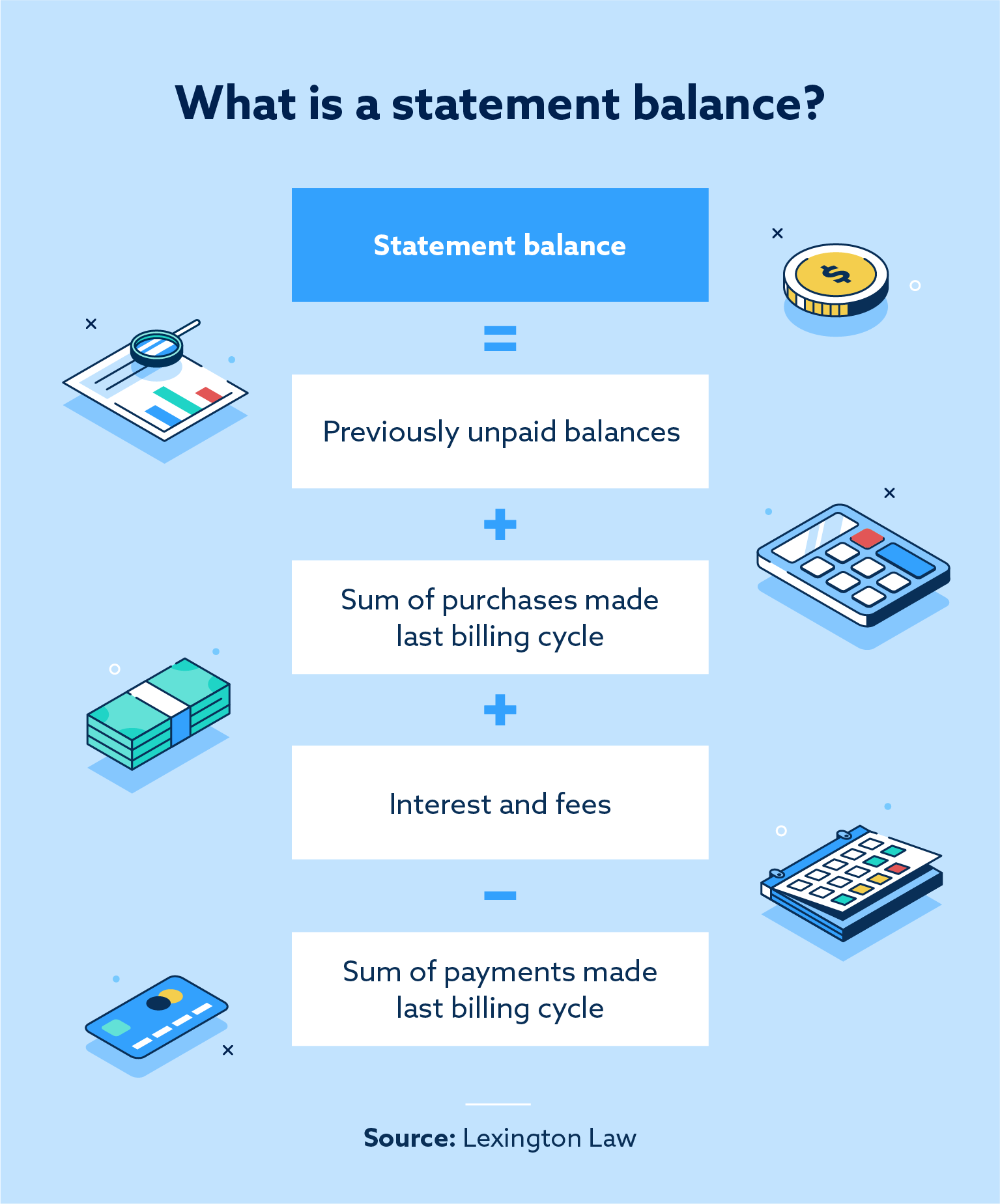

Understanding the Statement Balance

In contrast, the statement balance is a “frozen” snapshot of what you owed at the end of your last billing cycle. A billing cycle usually lasts between 28 and 31 days. When the cycle ends, the issuer totals all the activity and generates a statement.

The statement balance is the figure used to calculate your minimum payment and the amount you must pay to avoid interest charges. It does not change until the next billing cycle ends, regardless of how much you spend in the interim.

Why the Two Numbers Rarely Match

For the active credit card user, the current balance and the statement balance are rarely the same. If you have made even a single purchase since your last statement was generated, your current balance will be higher than your statement balance. Conversely, if you made a significant payment after the statement date, your current balance might be lower.

Understanding this discrepancy is vital. Many consumers become alarmed when they see a “Current Balance” that is higher than the “Statement Balance” they just paid off, fearing a mistake or fraud. In reality, it is usually just the result of ongoing spending in the new billing cycle.

How Current Balance Affects Your Credit Score

While your statement balance is what you see on your monthly bill, your current balance—specifically the balance reported to credit bureaus—has a massive impact on your FICO and VantageScore credit scores.

The Critical Role of Credit Utilization

Credit utilization is the ratio of your outstanding credit card balances to your total available credit limits. It accounts for roughly 30% of your FICO score, making it the second most important factor after payment history.

Lenders generally report your account information to the credit bureaus once a month, usually on your statement closing date. The “current balance” at the exact moment the report is generated becomes the balance that appears on your credit report. If your current balance is high relative to your limit (for example, using $900 of a $1,000 limit), your utilization is 90%, which can significantly lower your credit score—even if you plan to pay the bill in full by the due date.

Timing Your Payments for Maximum Score Impact

Strategic spenders often practice “balance shedding” or “AZEO” (All Zero Except One) strategies. This involves paying down the current balance before the statement closing date. By doing this, you ensure that the current balance reported to the bureaus is low, keeping your utilization ratio in the ideal range (typically under 10% for high-achievers).

If you wait until the due date (which is usually 21–25 days after the statement closes), the high balance has already been reported, and the temporary dip in your credit score has already occurred.

The “Pending Transactions” Factor

It is important to note that the current balance usually does not include “pending” transactions. When you swipe your card, the merchant places an authorization hold on the funds. This reduces your “available credit” immediately, but the amount doesn’t move into the “current balance” until the merchant finalizes the sale, which can take 24 to 72 hours. When monitoring your current balance for credit score purposes, always account for these “invisible” pending charges.

Managing Your Cash Flow and Interest Charges

The current balance is the ultimate indicator of your “debt trajectory.” By monitoring it closely, you can make better decisions regarding your monthly cash flow and avoid the trap of high-interest debt.

Avoiding Interest by Paying the Right Amount

To avoid paying interest on most credit cards, you only need to pay the statement balance in full by the due date. You do not necessarily need to pay the current balance in full every month.

For example, if your statement balance is $500 but your current balance is $800 (because you spent $300 after the statement was issued), paying $500 will satisfy the requirement to avoid interest. However, if you are trying to get out of debt or control your spending, paying the current balance in full ensures you are starting the next month with a “clean slate.”

Impact on Minimum Monthly Payments

Your minimum monthly payment is typically calculated as a percentage of your statement balance. However, if your current balance exceeds your credit limit due to overspending, many issuers will add the over-limit amount to your minimum payment. Monitoring your current balance helps you stay within your limits, preventing unexpected spikes in your required monthly output.

Strategies for Real-Time Expense Tracking

In the digital age, waiting for a monthly statement is an outdated way to manage money. Looking at your current balance several times a week provides a “reality check.” It prevents “lifestyle creep” and helps you identify if your spending is outstripping your income before you reach the end of the month. Treating your credit card like a debit card—where you pay off the current balance every few days—is a hallmark of sophisticated financial management.

Advanced Financial Tools and Integration

In modern personal finance, the current balance is a data point that can be leveraged through various financial technologies to streamline your wealth-building efforts.

Using Mobile Apps for Real-Time Monitoring

Most major banks now offer robust mobile applications that provide push notifications for every transaction. These apps allow you to see your current balance updated in real-time. By enabling these notifications, you create a feedback loop that makes spending money feel more “real,” which can help curb impulsive purchases.

Setting Up Smart Alerts and Autopay

While autopay is usually linked to the statement balance, some advanced banking portals allow you to set alerts based on the current balance. For instance, you can set a notification to alert you if your current balance exceeds a specific threshold (e.g., $1,000). This acts as a circuit breaker for your spending, forcing you to re-evaluate your budget for the remainder of the month.

Integrating Credit Data into Personal Budgeting Software

Budgeting tools like YNAB (You Need A Budget) or Monarch Money sync with your credit card accounts to pull in the current balance. These tools categorize your spending, allowing you to see exactly which habits are contributing to your debt. By looking at the current balance through the lens of a budget, you transition from being a reactive spender to a proactive wealth manager.

Common Misconceptions and Troubleshooting

Even for experienced users, certain scenarios regarding the current balance can be confusing. Clearing up these misconceptions is essential for maintaining a transparent relationship with your finances.

Does a $0 Current Balance Mean No Debt?

Not necessarily. Due to the way interest is calculated (daily average balance), you might encounter something called “trailing interest” or “residual interest.” If you carried a balance last month and then paid your current balance in full today, you might still see a small charge on your next statement. This is the interest that accrued between the time your last statement was printed and the day you made your payment. Always check the following month’s statement to ensure the balance is truly zero.

Handling Discrepancies and Potential Fraud

The current balance is often the first place you will spot unauthorized activity. If you notice your current balance is significantly higher than your mental tally of your spending, it is time to review your transaction history.

Occasionally, merchants may accidentally double-charge a transaction, or a subscription you thought you canceled might have renewed. Because the current balance updates frequently, identifying these issues early—rather than waiting for a statement—makes the dispute process much smoother with the credit card issuer.

The Psychology of the “Available Credit”

It is a common psychological pitfall to look at “Available Credit” rather than “Current Balance.” If you have a $10,000 limit and a $2,000 current balance, seeing “$8,000 Available” can create a false sense of wealth. Professional financial management dictates focusing on the current balance (what you owe) as a subtraction from your net worth, rather than seeing available credit as an extension of your income.

Conclusion: Mastering the Current Balance

The current balance is more than just a number on a screen; it is a vital sign of your financial health. By understanding that it represents your total, real-time debt, you can better navigate the complexities of credit utilization, interest charges, and monthly budgeting.

To manage credit like a pro, shift your focus from the “due date” to the “current status.” By monitoring this figure regularly, paying it down strategically to optimize your credit score, and using it as a guide for your daily spending, you transform the credit card from a potential debt trap into a powerful tool for financial growth. Knowledge of your current balance is, ultimately, the power to control your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.