Layaway, once a cornerstone of retail for many consumers, offers a distinct advantage in managing budgets and securing desired items without the immediate financial strain of full payment. While the digital age and the rise of buy-now-pay-later (BNPL) services have reshaped payment landscapes, layaway remains a viable and appealing option for a segment of shoppers. This article delves into the world of layaway, exploring which types of stores still offer this service, how it works, and the key considerations for consumers looking to leverage it effectively within the realm of personal finance.

Understanding Layaway: A Foundational Financial Tool

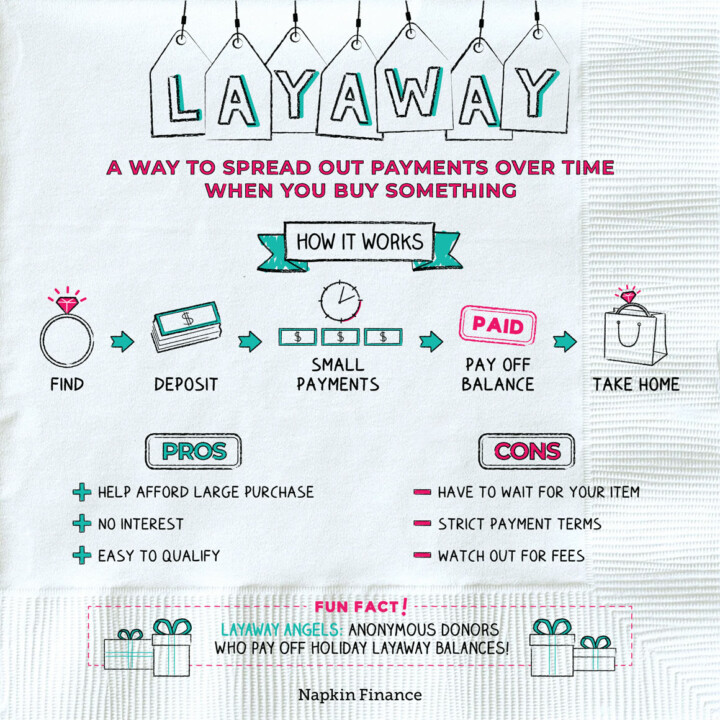

Layaway is a retail payment option where a customer selects an item, makes a deposit, and pays for it in installments over a period of time. The store holds the item until the final payment is made, at which point the customer takes possession. This model contrasts sharply with credit cards or BNPL services, which typically allow immediate possession of the item. The core appeal of layaway lies in its ability to help individuals budget for larger purchases, avoid interest charges, and prevent impulse buying by extending the decision-making process.

The Mechanics of Layaway

The process of using layaway is generally straightforward. While specific terms can vary between retailers, the fundamental steps remain consistent:

- Item Selection: A customer chooses an item eligible for layaway. Not all products may qualify, with some retailers restricting it to specific categories like electronics, furniture, or seasonal goods.

- Deposit: An initial payment, often a percentage of the total price (e.g., 10-20%), is required to reserve the item. This deposit secures the item for the customer.

- Installment Payments: The customer agrees to make regular payments, typically weekly or bi-weekly, for a predetermined period. The length of the layaway plan can range from a few weeks to several months, depending on the retailer and the value of the item.

- Final Payment and Collection: Once the full amount is paid, the customer can collect the item. Failure to complete payments within the agreed-upon timeframe usually results in the cancellation of the layaway agreement and potential forfeiture of deposits or partial payments, though some retailers may offer store credit.

Layaway vs. Buy-Now-Pay-Later (BNPL)

It is crucial to distinguish layaway from the increasingly popular Buy-Now-Pay-Later (BNPL) services like Afterpay, Klarna, or Affirm. While both are designed to facilitate purchases through deferred payments, their operational models and implications for consumers differ significantly:

- Possession of Goods: With layaway, the customer receives the item only after the full payment has been completed. In contrast, BNPL services allow the customer to take possession of the item immediately upon approval, making installment payments thereafter.

- Interest and Fees: Traditional layaway plans are typically interest-free, as the retailer holds the item until paid in full, mitigating their own risk. BNPL services, while often advertised as interest-free for consumers, may have associated fees for retailers, and some plans can incur interest if payments are missed or late.

- Credit Checks: Layaway generally does not involve a credit check, making it accessible to individuals with limited or poor credit history. Most BNPL services, however, do perform a soft credit check to assess eligibility.

- Impact on Credit Score: Since layaway doesn’t involve borrowing money in the traditional sense, it doesn’t directly impact a consumer’s credit score. BNPL payments, on the other hand, can sometimes be reported to credit bureaus, potentially affecting credit scores depending on the provider and payment behavior.

Which Stores Offer Layaway? Navigating Retail Options

The availability of layaway services has evolved over time. While many national big-box retailers have phased out the program in favor of BNPL solutions, layaway can still be found, particularly in specific retail sectors and with certain types of businesses. Understanding where to look is key to utilizing this payment method.

Brick-and-Mortar Retailers with Layaway Programs

Historically, department stores and large general merchandise retailers were primary providers of layaway. While many have shifted their strategies, some still offer layaway, often for specific product categories or during peak shopping seasons.

- Apparel and Footwear Stores: Some independent shoe stores, boutique clothing shops, and specialty athletic wear retailers may still offer layaway, especially for higher-priced items like expensive sneakers or designer apparel. This is often a strategy to build customer loyalty and cater to a demographic that prefers to budget without credit.

- Electronics and Appliance Stores: While large electronics chains have largely adopted BNPL, smaller, independent electronics retailers or those specializing in high-end audio-visual equipment might continue to offer layaway. This is particularly true for custom orders or larger appliances where immediate full payment might be a barrier for some customers.

- Furniture and Home Goods Stores: Layaway is still a relatively common option in furniture stores and shops selling home décor, especially for custom orders or larger pieces of furniture. The significant cost of these items makes layaway an attractive alternative to financing for many consumers.

- Toy Stores and Seasonal Retailers: During holiday seasons, especially for Christmas or back-to-school shopping, toy stores and seasonal retailers might reintroduce layaway programs to help parents spread out the cost of gifts and supplies. This can be a significant benefit for families managing holiday budgets.

- Specialty and Niche Retailers: Beyond broad categories, smaller, independent shops focusing on specific hobbies or interests, such as musical instruments, bicycles, or collectibles, may offer layaway to accommodate their customer base’s purchasing power.

Online Retailers and E-commerce Integration

The integration of layaway into the online shopping experience is less common than its brick-and-mortar counterpart, largely due to the logistics and technological requirements. However, some online-only businesses and platforms are exploring ways to offer similar deferred payment options.

- Direct-to-Consumer (DTC) Brands: Some direct-to-consumer brands that control their entire sales process might implement their own layaway-style payment plans. This allows them to build direct customer relationships and offer a unique payment solution that aligns with their brand values.

- Marketplaces with Layaway Features: While rare, some online marketplaces might facilitate layaway through their platform, acting as an intermediary between the seller and buyer. This requires robust payment processing and order management systems.

- “Payment Plan” Alternatives: It’s important to note that some online retailers may use the term “payment plan” or “layaway” loosely, when in fact they are offering a BNPL service. Always scrutinize the terms and conditions to understand the exact payment structure and when you will receive the item.

The Financial Wisdom of Layaway: Strategic Budgeting and Debt Avoidance

Layaway’s enduring appeal lies in its inherent alignment with sound financial principles. It encourages thoughtful purchasing decisions, helps individuals avoid accumulating debt, and offers a tangible path to ownership without the risks associated with credit.

Layaway as a Debt-Free Acquisition Strategy

In an era where credit card debt and BNPL obligations can quickly accumulate, layaway presents a refreshing alternative. By paying for an item in full before taking possession, consumers naturally avoid interest charges and late fees that can plague other payment methods. This makes it an ideal strategy for:

- Budgeting for Large Purchases: For items like appliances, furniture, or seasonal toys that represent a significant outlay, layaway allows individuals to break down the cost into manageable, predictable payments over time. This avoids the need to deplete savings or resort to high-interest loans.

- Preventing Impulse Buying: The waiting period inherent in layaway acts as a natural brake on impulsive purchases. By the time the item is paid for, the consumer has had ample time to consider whether the purchase is truly necessary and aligns with their financial goals.

- Managing Irregular Income: For individuals with fluctuating or irregular income streams, layaway provides a structured way to save for desired items without the pressure of immediate payment. They can make payments when their cash flow is stronger and fulfill the commitment over time.

- Building Financial Discipline: Successfully completing a layaway plan can foster a sense of accomplishment and reinforce good financial habits. It demonstrates the power of patience and consistent saving to achieve a goal.

Considerations and Potential Pitfalls of Layaway

While layaway offers numerous benefits, it’s not without its drawbacks, and careful consideration of these aspects is crucial for responsible use.

- Item Availability: Layaway agreements are conditional on the item remaining available. If the retailer experiences stock issues or discontinues a product, the layaway plan could be cancelled.

- Non-Refundable Deposits and Fees: Many retailers charge a non-refundable deposit or a cancellation fee if the layaway agreement is not fulfilled. It’s essential to understand these terms before committing.

- Lack of Immediate Gratification: The primary drawback for some consumers is the delayed gratification. Unlike BNPL, you don’t get to enjoy your purchase immediately. This can be a significant hurdle for those who desire instant access to goods.

- Limited Return Window: The return period for layaway items typically begins once the item is collected. This means the effective return window might be shorter if the item is paid for over an extended period.

- Absence in Many Major Retailers: The declining prevalence of layaway in major retail chains means that consumers may have fewer options and need to be more diligent in their search for this payment method.

Making Layaway Work for You: Smart Shopping Strategies

To effectively leverage layaway for your financial benefit, a strategic approach is essential. It involves understanding your needs, researching retailers, and being aware of the terms and conditions.

Researching and Comparing Layaway Offers

The first step in utilizing layaway is to identify stores that offer it. This requires active research, as it is not always prominently advertised.

- Inquire Directly: The most reliable way to determine if a store offers layaway is to ask a sales associate or customer service representative. This is especially true for smaller, independent businesses.

- Check Store Websites: While less common, some retailers may list their layaway policies on their official websites, often within their FAQ or customer service sections.

- Seasonal Promotions: Keep an eye out for layaway announcements during key shopping periods like the holiday season or back-to-school sales.

- Understand the Terms: Once a store offers layaway, thoroughly review their specific terms and conditions. Pay close attention to:

- Minimum Deposit: The initial percentage or amount required.

- Payment Schedule: Frequency and duration of installments.

- Late Payment Penalties: Any fees or consequences for missed payments.

- Cancellation Policy: What happens if you can’t complete the payments.

- Item Eligibility: Which products are included in the layaway program.

Maximizing the Benefits of Layaway

To ensure layaway remains a positive financial tool rather than a source of frustration, follow these best practices:

- Only Use for Necessary Purchases: Layaway is most beneficial when used for items you genuinely need or have been planning to buy for a while. Avoid using it for wants that could be deferred or for which alternative, more flexible payment options might be better suited.

- Calculate Total Costs: Factor in any potential administrative fees or cancellation charges when evaluating the overall cost of an item through layaway.

- Set Up Payment Reminders: To avoid late fees and ensure timely completion, set up calendar reminders or automatic transfers if your bank offers such a service.

- Consider the Opportunity Cost: While layaway is interest-free, the money tied up in the layaway plan could potentially be earning interest if invested. For very long layaway periods, this opportunity cost might be worth considering for those with a strong investment strategy.

- Read the Fine Print: This cannot be stressed enough. Understanding all aspects of the layaway agreement before committing is paramount to a smooth and beneficial experience.

In conclusion, while the retail landscape continues to evolve, layaway persists as a valuable financial tool for consumers seeking to manage their spending, avoid debt, and make significant purchases without the immediate burden of full payment. By understanding where to find layaway options and employing smart shopping strategies, individuals can continue to benefit from this time-tested method of acquiring goods responsibly.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.