A 2-1 buydown is a type of mortgage interest rate reduction strategy designed to make homeownership more affordable, particularly in the initial years of a loan. It’s a temporary concession offered by the lender, seller, or builder, where a portion of the interest is prepaid, effectively lowering the borrower’s monthly payments for the first two years of the mortgage. Understanding how a 2-1 buydown works, its implications, and when it might be a beneficial financial tool is crucial for potential homebuyers navigating the current real estate market.

Understanding the Mechanics of a 2-1 Buydown

At its core, a 2-1 buydown involves a lump sum payment made at closing to subsidize the borrower’s interest rate for a specified period. This payment is typically funded by the seller, builder, or sometimes even the borrower themselves, depending on the market conditions and negotiation leverage. The “2-1” designation refers to the tiered reduction in the interest rate.

The Interest Rate Reduction Structure

The most common structure for a 2-1 buydown involves the following:

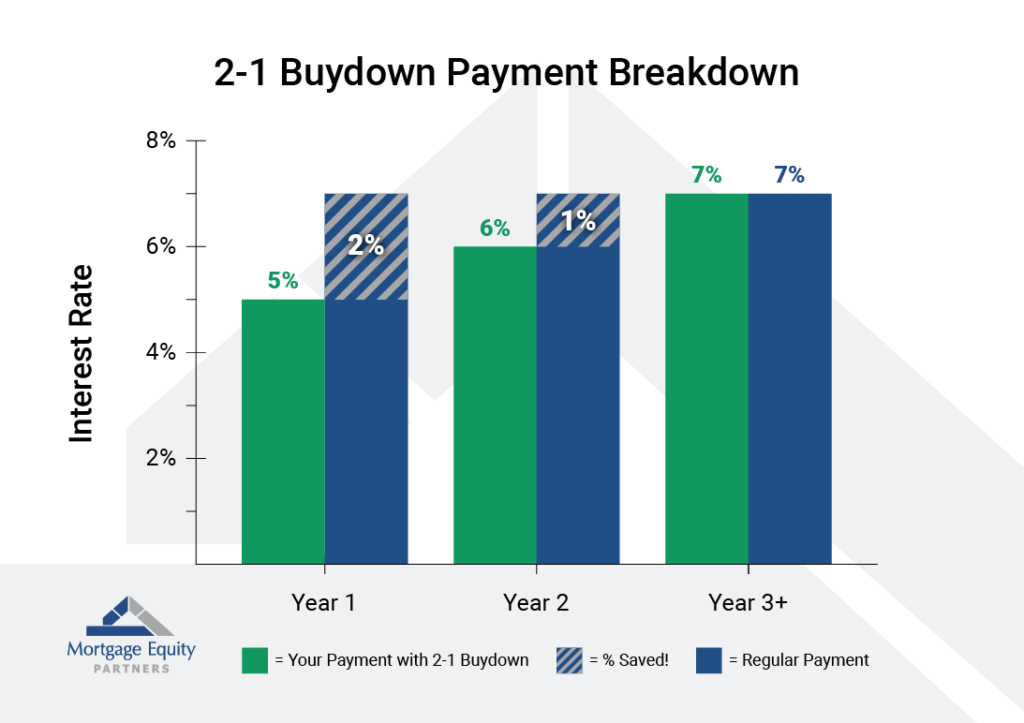

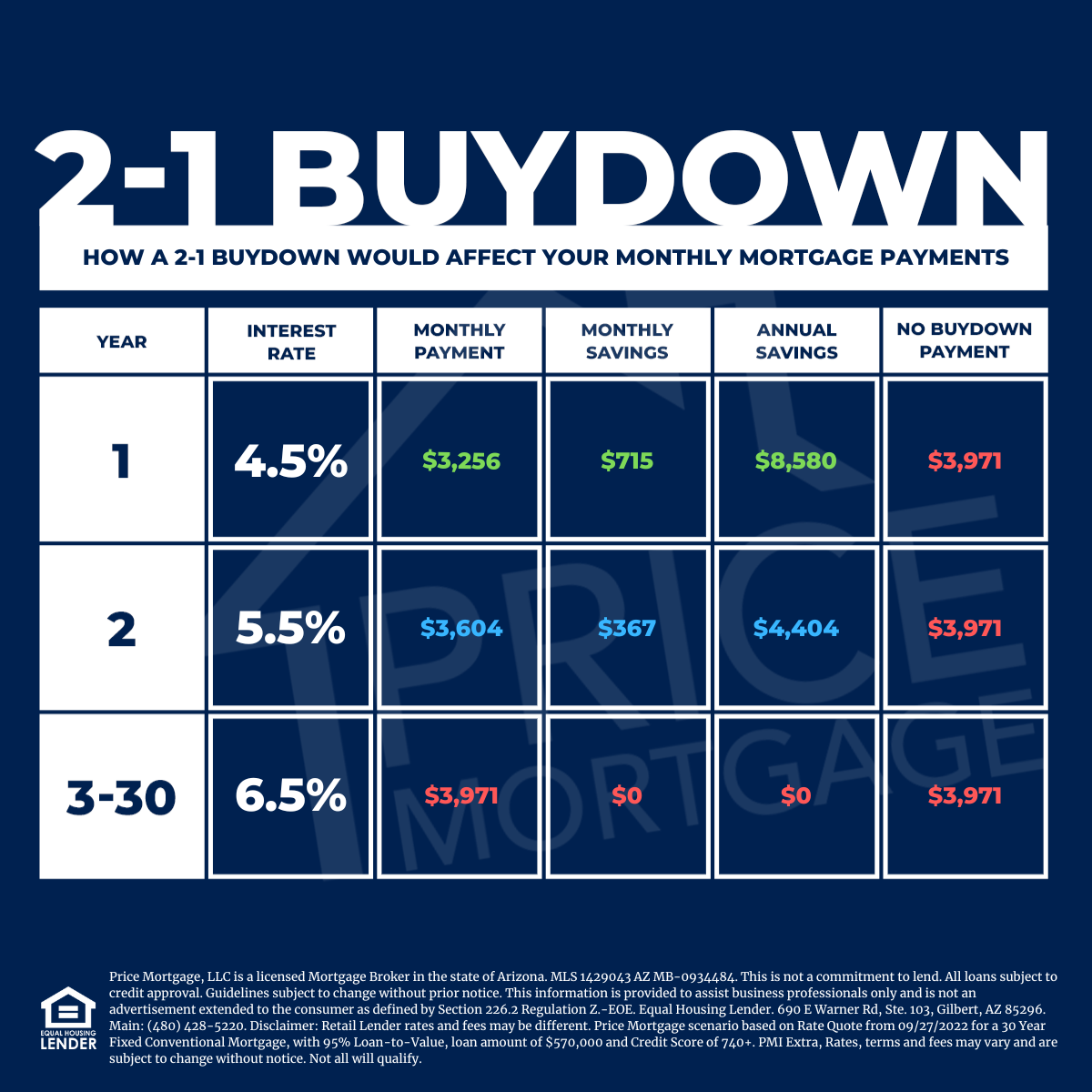

- Year 1: The interest rate is reduced by 2% below the fully indexed rate of the loan. For example, if the fully indexed rate is 7%, the borrower will pay an interest rate of 5% in the first year. This translates to a significantly lower monthly payment, easing the initial financial burden of homeownership.

- Year 2: The interest rate is reduced by 1% below the fully indexed rate. Using the same example, the interest rate in the second year would be 6%. This is still lower than the fully indexed rate, providing continued savings, albeit less substantial than in the first year.

- Year 3 Onward: From the third year of the loan until its maturity, the borrower will pay the full, agreed-upon interest rate as outlined in the mortgage note. This is the rate that was initially qualified for, and the monthly payments will adjust accordingly.

It’s important to note that the actual interest rate paid by the borrower is reduced, not the underlying interest rate of the loan. The lender still earns the full interest amount, with the difference being covered by the buydown funds. This distinction is crucial for understanding how the loan is structured and how it impacts long-term financial planning.

Funding the Buydown

The funds required to implement a 2-1 buydown can come from various sources, significantly influencing its attractiveness and availability.

- Seller Contributions: In a buyer’s market or when sellers are eager to close a deal, they may offer to contribute to a 2-1 buydown as an incentive. This is a way for them to make the home more financially accessible to buyers without directly lowering the listing price, which can impact their perceived equity.

- Builder Incentives: Home builders often utilize buydowns, especially during periods of slower sales or when launching new developments. It’s a powerful marketing tool to attract buyers and move inventory quickly.

- Lender Incentives: In some cases, lenders might offer buydowns as part of their loan products, particularly if they are looking to attract new borrowers or compete with other financial institutions. However, this is less common than seller or builder contributions.

- Borrower Contribution: While less frequent, a borrower might opt to contribute to a buydown fund if they believe the short-term savings will provide significant financial relief during a period of anticipated income fluctuations or if they are strategically planning their finances.

The source of the buydown funds can sometimes influence the terms and conditions, so it’s always advisable to clarify who is providing the subsidy.

Advantages of a 2-1 Buydown for Homebuyers

The primary appeal of a 2-1 buydown lies in its ability to provide immediate financial relief, making the dream of homeownership more attainable and less stressful in the crucial early years.

Reduced Initial Monthly Payments

The most tangible benefit of a 2-1 buydown is the reduction in monthly mortgage payments during the first two years. This can be a game-changer for individuals or families who are just entering homeownership and may be experiencing a tighter budget due to moving expenses, furnishing a new home, or other initial costs. Lower payments can free up cash flow, allowing buyers to:

- Build Emergency Savings: Having a cushion for unexpected expenses is vital for new homeowners. Lower initial payments can help accelerate this process.

- Cover Moving and Furnishing Costs: The transition to a new home often comes with significant upfront expenses. Reduced mortgage payments can alleviate some of this financial pressure.

- Manage Other Financial Obligations: Lower housing costs can provide breathing room for other debts, investments, or lifestyle choices.

- Adjust to New Responsibilities: Homeownership comes with new responsibilities, such as property taxes, homeowner’s insurance, and potential maintenance costs. The reduced mortgage payment can help new owners absorb these additional financial demands.

Potential for Improved Borrowing Capacity

While the buydown itself doesn’t change the underlying loan amount or interest rate, the lower initial payments can sometimes positively influence a borrower’s debt-to-income (DTI) ratio during the qualification process, especially if the lender considers the actual initial payment rather than the fully indexed payment for a portion of the evaluation. This can potentially allow buyers to qualify for a slightly larger loan than they might have otherwise, depending on the lender’s specific policies. However, it’s crucial to understand that the qualification is still based on the borrower’s ability to afford the payments at the fully indexed rate.

A Strategic Financial Tool

For financially savvy individuals, a 2-1 buydown can be a strategic tool to manage cash flow during a specific period. If a buyer anticipates a significant income increase or bonus within the first two years, the buydown can help them bridge the gap until that additional income materializes, allowing them to take advantage of current interest rates before they potentially rise. It can also be beneficial for those who plan to refinance their mortgage within the first few years, as the buydown allows them to secure a home at a lower initial cost while planning for a future refinance at potentially better rates.

Considerations and Potential Drawbacks of a 2-1 Buydown

While the immediate savings are attractive, it’s essential to approach a 2-1 buydown with a clear understanding of its limitations and potential future implications.

The “Bigger Payment Shock” Later

The most significant drawback is the inevitable increase in monthly payments in years 2 and 3. Borrowers must be prepared for this jump. If a buyer does not accurately budget for these higher payments, they could face financial strain or even delinquency.

- Budgeting for the Increase: It is paramount for buyers to understand the exact payment amounts for year 1, year 2, and year 3 and beyond. They should create a budget that accommodates the higher payments from year 3 onwards, even if they are currently enjoying the lower rates.

- Income Projections: If the buyer’s income is not projected to increase sufficiently to cover the rising payments, a 2-1 buydown might not be the wisest choice. Relying solely on the lower initial payments can lead to a rude awakening.

Impact on Equity and Refinancing

The reduced payments in the initial years mean that less of each payment goes towards principal reduction. This can slow down equity build-up compared to a mortgage with standard payments from day one.

- Slower Equity Growth: While you’re saving money monthly, you’re building equity at a slower pace. This might be a concern for homeowners who plan to sell their property within a few years or who prioritize rapid equity accumulation.

- Refinancing Considerations: If you plan to refinance your mortgage before the buydown period ends, the lender will typically base your new loan amount on the outstanding balance, which might be slightly higher due to the slower principal paydown. However, if market interest rates have decreased significantly, the benefits of refinancing might still outweigh this minor difference. It’s crucial to compare the costs and benefits of refinancing at different stages.

Understanding the Fine Print and Associated Costs

Like any financial product, a 2-1 buydown can have nuances that require careful examination.

- Who Pays for the Buydown? Clearly understand whether the seller, builder, or you are funding the buydown. This can influence negotiation power and the overall cost of the home.

- Loan Terms and Fees: Ensure that the underlying loan terms, such as the interest rate, points, and fees, are competitive and align with your financial goals. The buydown is an add-on to the primary mortgage; the core loan terms are what matter most in the long run.

- Prepayment Penalties: While less common with standard mortgages, always check for any prepayment penalties that might apply if you decide to sell or refinance early.

- Appraisal Impact: In some instances, a buydown might affect the appraisal value, as it can be seen as a concession that increases the effective price the seller receives.

When is a 2-1 Buydown a Good Financial Decision?

The suitability of a 2-1 buydown hinges on an individual’s financial situation, risk tolerance, and future financial projections.

For First-Time Homebuyers

For many first-time homebuyers, the initial years of homeownership can be financially challenging. A 2-1 buydown can provide much-needed breathing room, allowing them to:

- Establish Financial Stability: Get accustomed to the responsibilities of homeownership without the immediate pressure of higher mortgage payments.

- Save for Future Goals: Utilize the savings to build an emergency fund, invest, or plan for future home improvements.

- Gain Confidence: Experience the rewards of homeownership with a more manageable initial financial outlay.

For Those with Anticipated Income Increases

Individuals who are confident about future income growth, such as those expecting promotions, bonuses, or starting a new, higher-paying job, can strategically leverage a 2-1 buydown. The temporary lower payments allow them to secure a home now, knowing they can comfortably afford the increased payments later when their income rises.

In a Buyer’s Market or High-Interest Rate Environment

When the real estate market favors buyers, or when interest rates are relatively high, buydowns become more prevalent as a negotiating tool. In such scenarios, a 2-1 buydown can be an effective way to:

- Make a Property More Affordable: Lower initial payments can help buyers stretch their budget and secure a property they might otherwise be priced out of.

- Obtain a Lower Effective Rate: While the underlying rate remains the same, the immediate savings act as a form of immediate financial relief, effectively reducing the initial cost of borrowing.

Conclusion

A 2-1 buydown is a valuable financial instrument that can make homeownership more accessible and manageable, particularly during the critical initial years of a mortgage. By temporarily reducing interest payments, it offers significant cash flow relief, enabling homebuyers to better navigate the financial demands of a new home. However, it is not a one-size-fits-all solution. A thorough understanding of the interest rate progression, the funding source, potential long-term payment adjustments, and its impact on equity build-up is essential. By carefully evaluating personal financial circumstances, income projections, and market conditions, potential homebuyers can determine if a 2-1 buydown aligns with their goals and contributes to a sound financial foundation for their homeownership journey. Consulting with a mortgage professional or financial advisor is highly recommended to ensure all aspects of the buydown are fully understood before making a decision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.