Annuities are often marketed as the ultimate tool for retirement security, providing a predictable stream of income that one cannot outlive. However, for many investors, the primary concern isn’t just their own financial stability, but also the legacy they leave behind. One of the most common questions posed to financial advisors is: “What happens to my annuity when I die?”

The answer is not a one-size-fits-all response. The fate of an annuity after the owner’s passing depends heavily on the specific terms of the contract, the type of annuity purchased, and the designated beneficiaries. Understanding these nuances is critical for effective estate planning and ensuring that your hard-earned assets are distributed according to your wishes.

1. The Impact of Annuity Payout Structures

The way you choose to receive payments during your lifetime directly dictates what remains for your heirs. When you “annuitize” a contract—meaning you convert your lump sum into a guaranteed income stream—you must select a payout option. Each option handles the death of the annuitant differently.

Life-Only Annuities: The Risk of Forfeiture

A “Life-Only” or “Straight Life” annuity offers the highest possible monthly payout because it carries the highest risk. Under this structure, the insurance company agrees to pay you for as long as you live, but all payments cease immediately upon your death. Even if you die just two months after starting the payments, the insurance company keeps the remaining balance. There is no death benefit for beneficiaries under a standard life-only contract. While this maximizes your personal income, it is generally discouraged for those who wish to leave a financial legacy.

Life with Period Certain

To mitigate the risk of a life-only policy, many investors choose a “Period Certain” rider. This ensures that if the annuitant dies within a specific timeframe (usually 10, 15, or 20 years), the remaining payments will continue to be paid to the designated beneficiary for the duration of that period. For example, if you have a 15-year period certain and die in year seven, your beneficiary will receive the remaining eight years of scheduled payments.

Joint-and-Survivor Annuities

Commonly used by married couples, a joint-and-survivor annuity continues to pay as long as at least one of the two named individuals is alive. Upon the death of the first spouse, the survivor continues to receive a check—though depending on the contract, the amount may stay the same or decrease (e.g., to 50% or 75% of the original payment). This structure ensures the surviving spouse is never left without income, but it typically results in lower monthly payments compared to a single-life annuity.

2. Death Benefits and Beneficiary Designations

For annuities that are still in the “accumulation phase”—meaning you haven’t started taking regular payments yet—or for those with specific death benefit riders, the contract holds a value that can be passed on.

The Standard Death Benefit

Most modern deferred annuities come with a standard death benefit. If the owner dies before the contract is annuitized, the beneficiary usually receives the greater of two amounts: the current market value of the account or the total of all premiums paid (minus any previous withdrawals). This protects the principal against market downturns, ensuring that your heirs receive at least what you put into the contract.

Enhanced Death Benefit Riders

For an additional fee, some investors opt for “enhanced” or “stepped-up” death benefits. These riders are designed to maximize the inheritance. A common version is the “Highest Anniversary Value” rider, which locks in the highest value the account reached on any contract anniversary. Even if the market crashes right before the owner dies, the beneficiary receives that peak value. This is a powerful tool for those using annuities as a pseudo-life insurance vehicle within their broader financial portfolio.

The Role of Primary and Contingent Beneficiaries

Designating beneficiaries is arguably the most important step in managing an annuity. If no beneficiary is named, the death benefit usually defaults to the estate, where it may be subject to a lengthy and expensive probate process. By naming primary and contingent beneficiaries, the assets bypass probate and pass directly to the heirs, providing them with faster access to the funds.

3. Tax Implications for Inherited Annuities

From a financial planning perspective, the tax treatment of an inherited annuity is where things become complex. Unlike life insurance proceeds, which are generally tax-free, annuity death benefits are subject to income tax on any earnings within the contract.

Qualified vs. Non-Qualified Annuities

The tax rules depend on whether the annuity is “qualified” or “non-qualified.” A qualified annuity is funded with pre-tax dollars (like an IRA or 401k). In this case, every dollar distributed to the beneficiary is taxed as ordinary income. A non-qualified annuity is funded with after-tax dollars. For these, the beneficiary only pays taxes on the “growth” or interest earned in the account; the original principal (the cost basis) is returned tax-free.

The Five-Year Rule and Distribution Options

Non-spouse beneficiaries generally have a few options for how they receive the money, each with different tax consequences:

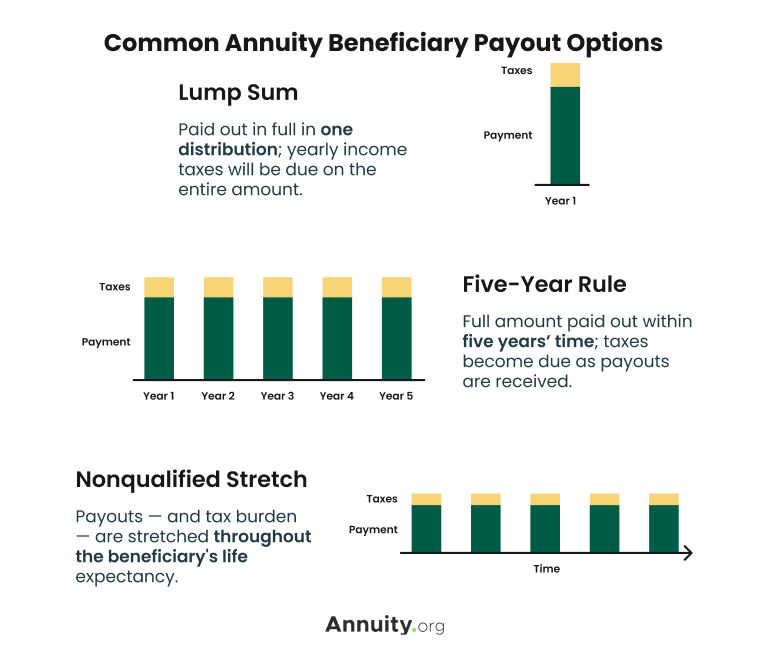

- Lump-Sum Distribution: The beneficiary receives the entire value at once. This is simple but can trigger a massive tax bill in a single year, potentially pushing the heir into a higher tax bracket.

- The Five-Year Rule: The beneficiary must withdraw the entire balance of the annuity within five years of the owner’s death. They can take it in increments or all at once at the end.

- Non-Qualified Stretch (if available): Before the SECURE Act and subsequent tax changes, many beneficiaries could “stretch” payments over their own life expectancy. This is now much more restricted, particularly for qualified annuities, where most non-spouse beneficiaries must empty the account within 10 years.

Income in Respect of a Decedent (IRD)

It is important to note that inherited annuities do not receive a “step-up in basis.” In the world of investing, a step-up in basis allows heirs to inherit stocks or real estate at their current market value, effectively erasing the capital gains tax liability. Annuities do not qualify for this. The gain is considered Income in Respect of a Decedent (IRD), meaning the tax liability follows the asset from the original owner to the heir.

4. Spousal Continuation: A Unique Advantage

The IRS provides a significant “safety net” for surviving spouses that is not available to children, siblings, or other heirs. This is known as spousal continuation.

How Spousal Continuation Works

If a spouse is the sole primary beneficiary, they can choose to step into the shoes of the original owner rather than taking a death benefit payout. This means the contract continues as if the original owner were still alive. The spouse maintains the tax-deferred status of the account, keeps any living benefit riders intact, and can name their own new beneficiaries.

Strategic Advantages for the Survivor

Spousal continuation is often the most financially sound choice. It avoids immediate taxation and allows the surviving spouse to wait until they are older—and perhaps in a lower tax bracket—to begin taking distributions. Furthermore, if the annuity has an “income rider” that guarantees a certain growth rate, the spouse can continue to let that rider accumulate, potentially leading to a much larger income stream later in life.

5. Strategic Estate Planning with Annuities

Given the tax complexities and the variety of payout options, incorporating an annuity into a legacy plan requires careful coordination with other financial assets.

Maximizing the Legacy

If your goal is to leave the largest possible inheritance, you might consider using the “free withdrawal” provision of an annuity to pay for a life insurance policy. Since life insurance death benefits are generally tax-free and annuities are taxable, this strategy converts a taxable asset into a tax-free one for your heirs.

Avoiding Common Mistakes

One of the most frequent errors in annuity management is failing to update beneficiary designations after major life events, such as divorce or the death of a spouse. Because an annuity is a contract, the beneficiary designation on file with the insurance company typically overrides whatever is written in a will. Keeping these documents current is essential to ensure the money goes where it is intended.

The Importance of Professional Guidance

The intersection of insurance contracts and tax law is a dense thicket. Before making a decision on an annuity structure—or before a beneficiary decides how to take a payout—consulting with a fiduciary financial advisor or a tax professional is highly recommended. They can help run the numbers on “lump-sum” vs. “annuitization” and help beneficiaries navigate the 10-year rule for qualified accounts, ensuring that Uncle Sam doesn’t take a larger share of the legacy than necessary.

In conclusion, an annuity does not simply “disappear” when you die, provided you have selected the right contract features. By understanding the difference between life-only and period-certain options, recognizing the tax burdens associated with different types of funding, and utilizing spousal continuation rights, you can turn a retirement income tool into a robust component of your estate plan. Proper preparation today ensures that your annuity serves its dual purpose: providing for your life and protecting your loved ones after you’re gone.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.