The term “statement balance” is fundamental to understanding your financial health, particularly when dealing with credit cards, loans, and bank accounts. It represents a snapshot of your financial obligations or holdings at a specific point in time, as reflected on a statement. While seemingly straightforward, a nuanced understanding of statement balance is crucial for effective financial management, avoiding unnecessary costs, and making informed decisions about your spending and borrowing habits. This article delves into the various facets of statement balance, exploring its significance across different financial products and providing actionable insights for leveraging this information to your advantage.

Understanding the Core Concept of Statement Balance

At its heart, a statement balance is the total amount owed or held on a particular financial account as of the closing date of a statement period. This period typically spans a month, during which all transactions – purchases, payments, fees, and interest charges – are recorded. The statement balance, therefore, is the net result of these activities.

The Statement Balance in Different Financial Contexts

The interpretation and implication of a statement balance can vary depending on the type of financial instrument.

Credit Card Statement Balance

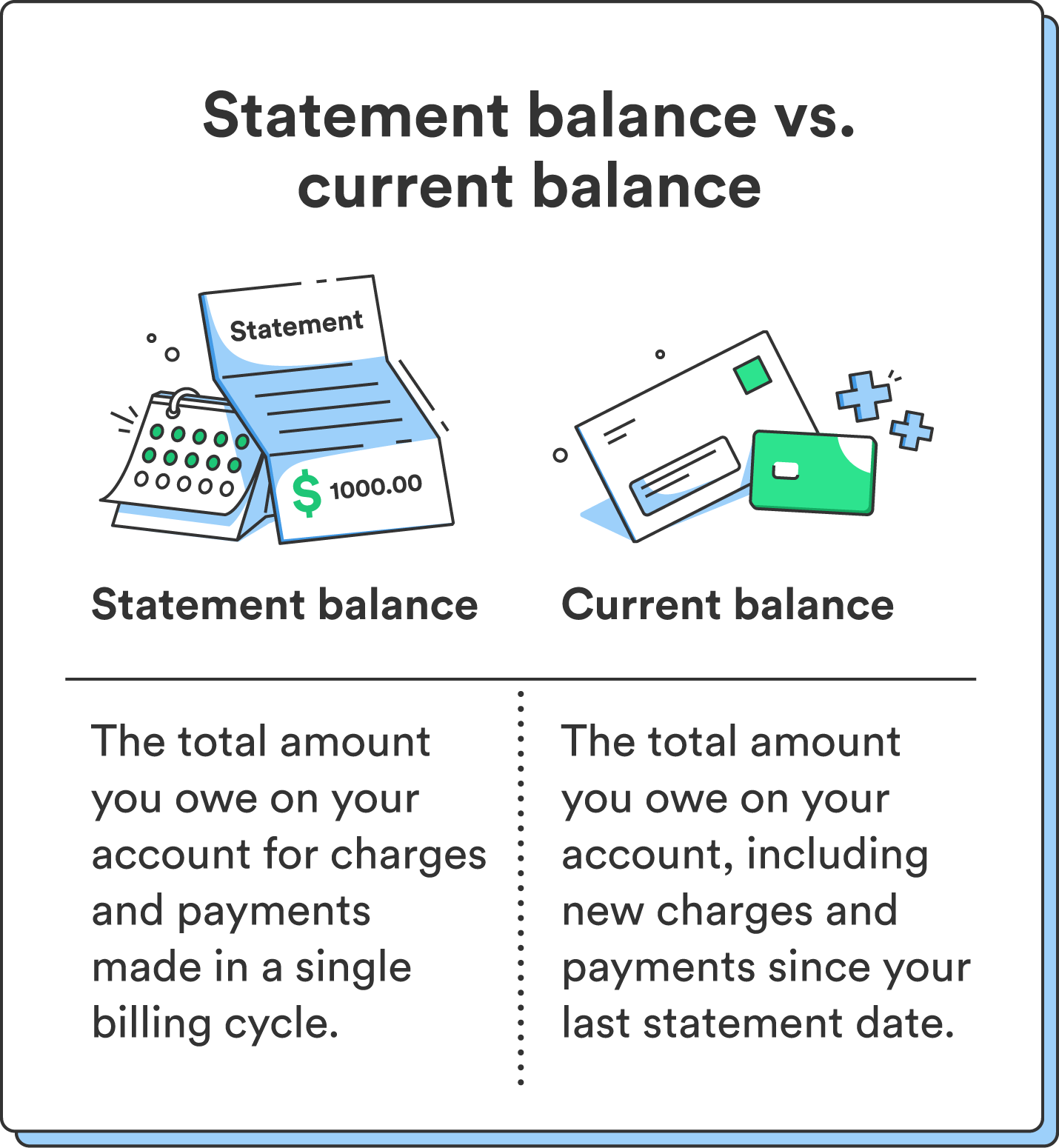

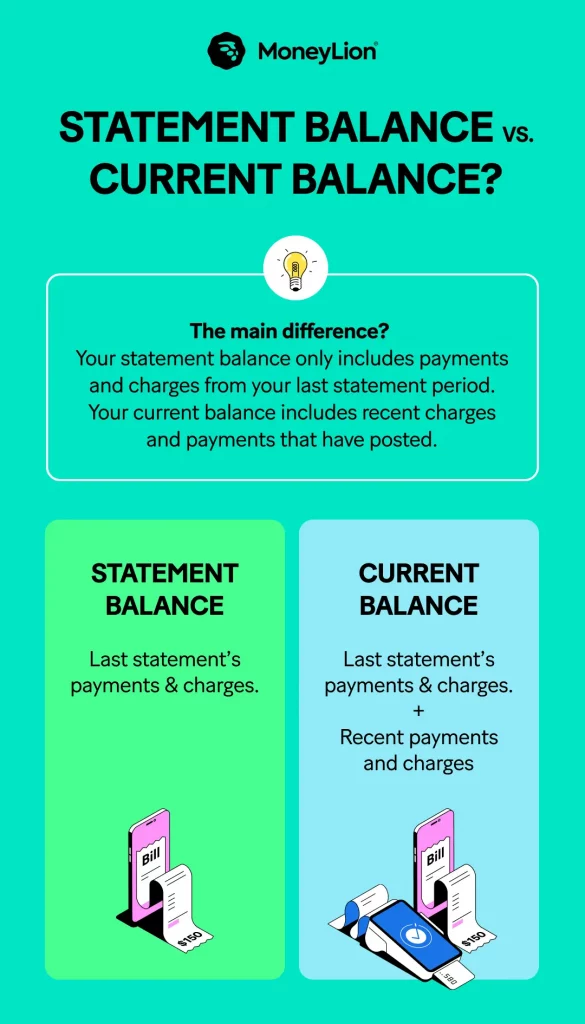

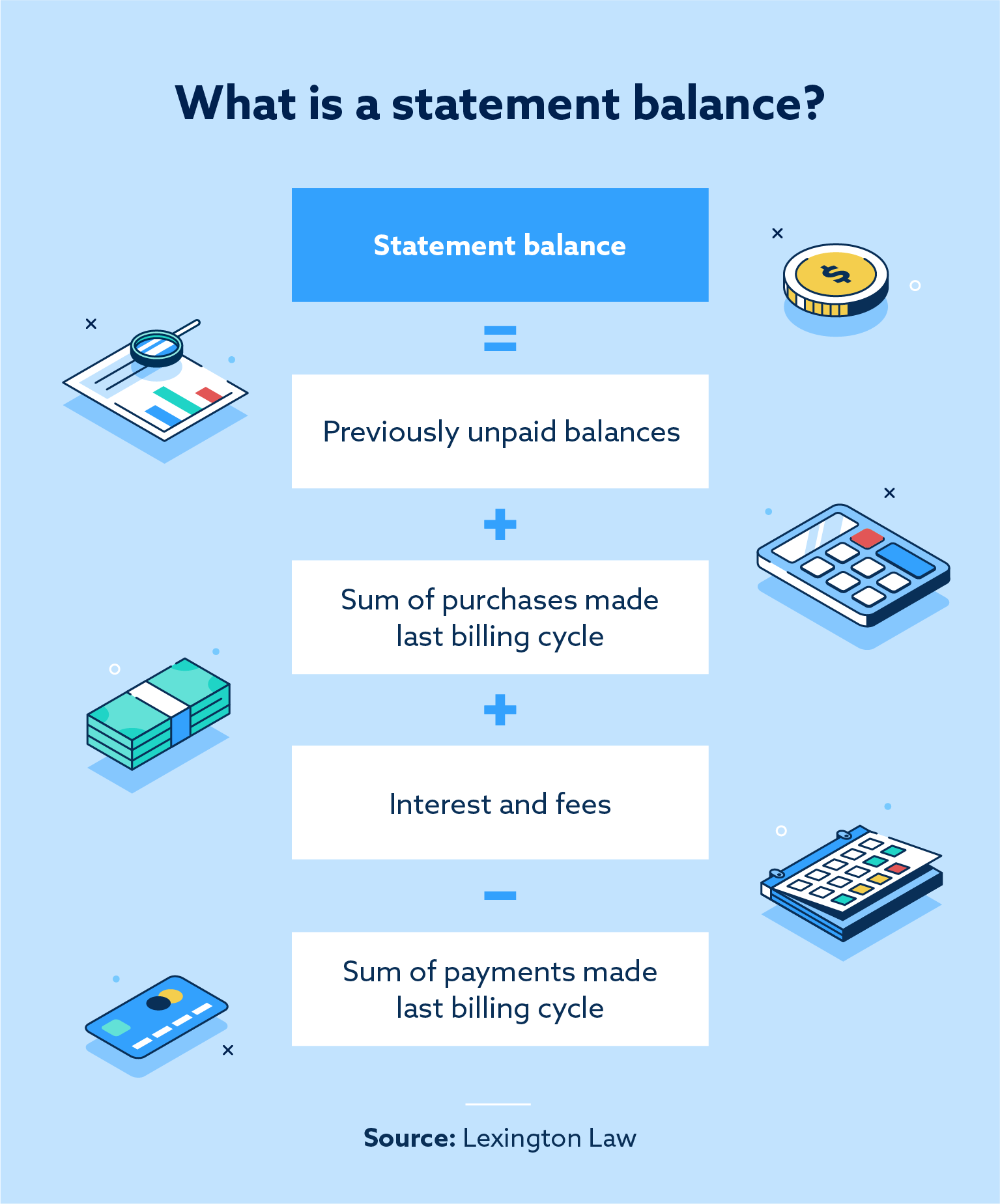

For credit cards, the statement balance is arguably the most critical figure. It represents the total amount you owe to the credit card issuer for all the transactions made during the billing cycle, plus any outstanding balance from previous cycles, minus any payments made during the current cycle. It also includes any accrued interest and fees.

- Impact on Credit Score: The statement balance is directly linked to your credit utilization ratio, a key factor in determining your credit score. A high statement balance relative to your credit limit can negatively impact your score.

- Minimum Payment vs. Statement Balance: It’s essential to distinguish between the statement balance and the minimum payment due. Paying only the minimum payment will result in carrying over a substantial portion of the balance to the next billing cycle, incurring significant interest charges.

- Grace Period: Understanding your grace period is vital. If you pay your statement balance in full by the due date, you typically avoid interest charges on new purchases made during that billing cycle.

Bank Account Statement Balance

For checking and savings accounts, the statement balance reflects the total funds available in your account as of the statement closing date. This includes deposits, withdrawals, interest earned, and any bank fees.

- Reconciliation: Bank statement balances are used for reconciliation purposes, ensuring that your personal records match the bank’s records. This helps in identifying any discrepancies or unauthorized transactions.

- Overdrafts: A negative statement balance in a checking account typically indicates an overdraft, meaning you’ve spent more money than you had available, leading to overdraft fees.

- Savings Growth: For savings accounts, the statement balance shows the accumulation of your savings, including any interest earned, providing a clear picture of your progress towards financial goals.

Loan Statement Balance

For loans, such as mortgages, auto loans, or personal loans, the statement balance represents the outstanding principal amount owed to the lender, plus any accrued interest and fees, as of the statement date.

- Amortization: Loan statements often detail how your payments are applied to both the principal and interest. The statement balance decreases as you pay down the principal.

- Prepayment: Understanding the statement balance is crucial if you plan to make extra payments or prepay the loan. It allows you to see how much you still owe and the impact of additional payments on reducing interest over time.

Key Metrics Related to Statement Balance

Beyond the primary statement balance, several related metrics provide a deeper understanding of your financial activity and obligations.

Previous Balance

This is the statement balance from your previous billing cycle. It represents the amount you owed or had at the end of the last statement period. Comparing the previous balance to the current statement balance helps you track changes in your spending, payments, and overall debt.

Payments and Credits

This section of a statement details any payments you’ve made towards the balance and any credits applied to your account (e.g., refunds, adjustments). The amount of payments and credits directly reduces the outstanding balance.

New Transactions

This encompasses all new purchases, cash advances, and other charges that have occurred during the current billing cycle. The sum of these new transactions, when added to the previous balance (after accounting for payments and credits), contributes to the current statement balance.

Interest Charged

For credit cards and some loans, interest charges are a significant component that increases the statement balance. This is calculated based on your average daily balance and the Annual Percentage Rate (APR). Understanding how interest is calculated is crucial for minimizing these costs.

Fees

Various fees can be added to your statement balance, including annual fees, late payment fees, over-limit fees, and foreign transaction fees. These fees add to the total amount owed and can significantly impact your overall financial burden.

The Strategic Importance of Managing Your Statement Balance

Effectively managing your statement balance is not merely about avoiding debt; it’s a strategic approach to financial well-being that can impact your creditworthiness, reduce costs, and facilitate the achievement of your financial goals.

Optimizing Credit Card Usage and Minimizing Interest

For credit card users, the statement balance is the primary driver of interest costs. The strategy here revolves around minimizing the amount carried over from one statement to the next.

- Paying in Full: The most effective way to manage your credit card statement balance is to pay it in full by the due date each month. This strategy, often referred to as “paying in full and on time,” ensures you leverage the grace period and avoid all interest charges on purchases. It also demonstrates responsible credit behavior to credit bureaus.

- Paying More Than the Minimum: If paying the full statement balance is not immediately feasible, paying significantly more than the minimum due is crucial. The minimum payment is often a small percentage of the balance and is designed to keep you in debt longer, accumulating more interest.

- Strategic Payments Before the Statement Closing Date: To influence your credit utilization ratio, you can make payments before the statement closing date. While your credit card company may report the balance on your statement date, making payments beforehand can lower the reported utilization, which is a positive factor for your credit score. This is distinct from paying the bill before the due date; it’s about managing the balance that appears on your statement.

- Balance Transfers: For individuals with high-interest credit card debt, a balance transfer to a card with a 0% introductory APR can be a powerful tool. This allows you to pay down the principal without accruing interest for a limited period, effectively reducing your statement balance over time. However, it’s crucial to be aware of balance transfer fees and the APR after the introductory period ends.

Enhancing Financial Planning and Budgeting

Statement balances serve as valuable data points for comprehensive financial planning and budgeting.

- Tracking Spending Habits: By regularly reviewing your statement balances across various accounts, you can identify patterns in your spending. A consistently growing statement balance on a credit card might indicate overspending in certain categories, prompting a review of your budget.

- Assessing Debt Reduction Progress: For loans, the statement balance provides a clear indicator of your progress in paying down debt. Monitoring this figure allows you to track how quickly you’re reducing your principal and to adjust your repayment strategy if necessary.

- Informing Savings Goals: In the context of savings accounts, the statement balance reflects your accumulated savings. This figure is essential for assessing whether you are on track to meet your short-term and long-term financial goals, such as saving for a down payment, retirement, or an emergency fund.

- Budgeting with Due Dates: Understanding statement closing dates and payment due dates is crucial for effective budgeting. It allows you to plan your cash flow to ensure you can meet your obligations without incurring late fees or interest charges.

Leveraging Financial Tools and Information

Financial institutions provide statements to empower consumers with information. Actively using and understanding this information can lead to better financial decisions.

- Online Banking Portals and Apps: Most banks and credit card companies offer online portals and mobile applications that provide real-time access to your statement balance and transaction history. These tools facilitate frequent monitoring and management of your accounts.

- Alerts and Notifications: Many financial institutions allow you to set up customized alerts for various account activities, such as when your statement balance reaches a certain threshold or when your payment due date is approaching. These proactive notifications can help you stay on top of your finances.

- Financial Management Software: Personal finance management software and apps can aggregate data from your various financial accounts, providing a consolidated view of your statement balances, spending patterns, and debt levels. This holistic perspective is invaluable for comprehensive financial planning.

Common Pitfalls and How to Avoid Them

Misunderstanding or neglecting statement balances can lead to costly mistakes and hinder financial progress. Awareness and proactive management are key to avoiding these pitfalls.

The Trap of Minimum Payments

One of the most insidious traps is falling into the habit of making only minimum payments on credit cards. While this may seem like a manageable solution in the short term, it can lead to an unending cycle of debt due to the significant amount of interest that accrues on the remaining balance.

- Understanding the True Cost of Debt: Recognize that minimum payments are often calculated to cover a small portion of the principal and the accrued interest. This means that a substantial portion of your payment goes towards interest, extending the repayment period and increasing the total amount you pay for your purchases.

- Prioritizing Debt Reduction: If you find yourself consistently making minimum payments, it’s a signal that you need to re-evaluate your budget and explore strategies to increase your payments or reduce your overall spending.

Ignoring Statement Closing Dates and Due Dates

Missing statement closing dates or payment due dates can result in a cascade of negative consequences, including late fees, increased interest rates (penalty APRs), and damage to your credit score.

- Automate Payments: To mitigate the risk of missed payments, consider setting up automatic payments for at least the minimum amount due. While you should still aim to pay in full manually to avoid interest, automation provides a safety net against accidental oversights.

- Calendar Reminders: If automatic payments are not ideal, set up calendar reminders well in advance of your due dates. This is especially important if you have multiple accounts with different due dates.

Misinterpreting Credit Card Grace Periods

The grace period is a valuable benefit offered by credit card companies, allowing you to avoid interest charges if you pay your statement balance in full by the due date. However, this benefit can be easily lost if not understood correctly.

- Grace Period Revocation: Be aware that if you carry a balance from one month to the next, you typically lose your grace period for new purchases. This means that new transactions made after you start carrying a balance will begin accruing interest immediately, even if you pay the statement balance in full for the current cycle.

- Understanding Statement Cycles: A clear understanding of your credit card’s statement cycle (the period during which transactions are recorded) and your payment due date is crucial for maximizing the benefit of the grace period.

Conclusion: Empowering Financial Control Through Statement Balance Mastery

The statement balance is more than just a number on a piece of paper or a digital display; it is a powerful indicator of your financial activity, obligations, and progress. By diligently understanding, monitoring, and strategically managing your statement balances across all your financial accounts, you equip yourself with the knowledge and control necessary to navigate the complexities of personal finance. Whether you aim to eliminate debt, build wealth, or simply maintain a healthy financial standing, mastering the concept of statement balance is a cornerstone of sound financial management. It empowers you to make informed decisions, avoid costly mistakes, and ultimately, achieve your financial aspirations with greater confidence and success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.