The little three or four-digit number on your debit card might seem insignificant, but it plays a crucial role in the security of your online and phone transactions. Known as the Card Verification Value (CVV), Card Security Code (CSC), or Card Identification Number (CID), this code is a vital layer of protection against fraud. Understanding what it is, why it’s important, and how to protect it is essential for anyone engaging in digital commerce.

The Genesis and Purpose of the CVV

The creation of the CVV stemmed from a growing need to secure card-not-present (CNP) transactions. As e-commerce and remote payments began to surge, so did the opportunities for fraudulent activities. Criminals could obtain card numbers and expiration dates through various means, such as data breaches or phishing schemes, and then use this information to make unauthorized purchases. The CVV was introduced as an additional security measure to verify that the person making the transaction physically possessed the card.

Card-Not-Present (CNP) Transactions and Their Vulnerabilities

Card-not-present transactions encompass any purchase made where the physical card is not swiped or inserted into a terminal. This includes online shopping, telephone orders, and mail-order purchases. While these methods offer unparalleled convenience, they inherently carry a higher risk of fraud compared to in-person transactions. In a physical transaction, the merchant can verify the cardholder’s identity by checking the signature on the receipt or asking for a PIN. However, in CNP scenarios, this direct verification is impossible.

The CVV as an Extra Layer of Security

The CVV acts as a powerful deterrent against CNP fraud. When you make an online or phone purchase, you’re typically asked to provide not just your card number and expiration date but also the CVV. This three or four-digit code is not stored in the magnetic stripe of your card, nor is it typically printed on receipts. This means that even if a merchant’s database is compromised and card numbers are stolen, the CVV is usually not part of that stolen data. Therefore, a fraudster who has acquired your card number and expiration date would still need to physically possess your card to obtain the CVV and complete a fraudulent transaction. This added step significantly raises the bar for fraudsters and protects consumers.

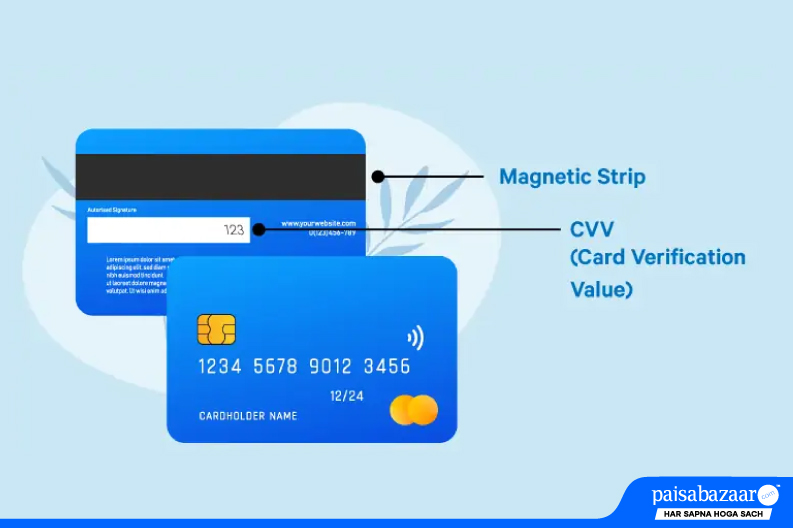

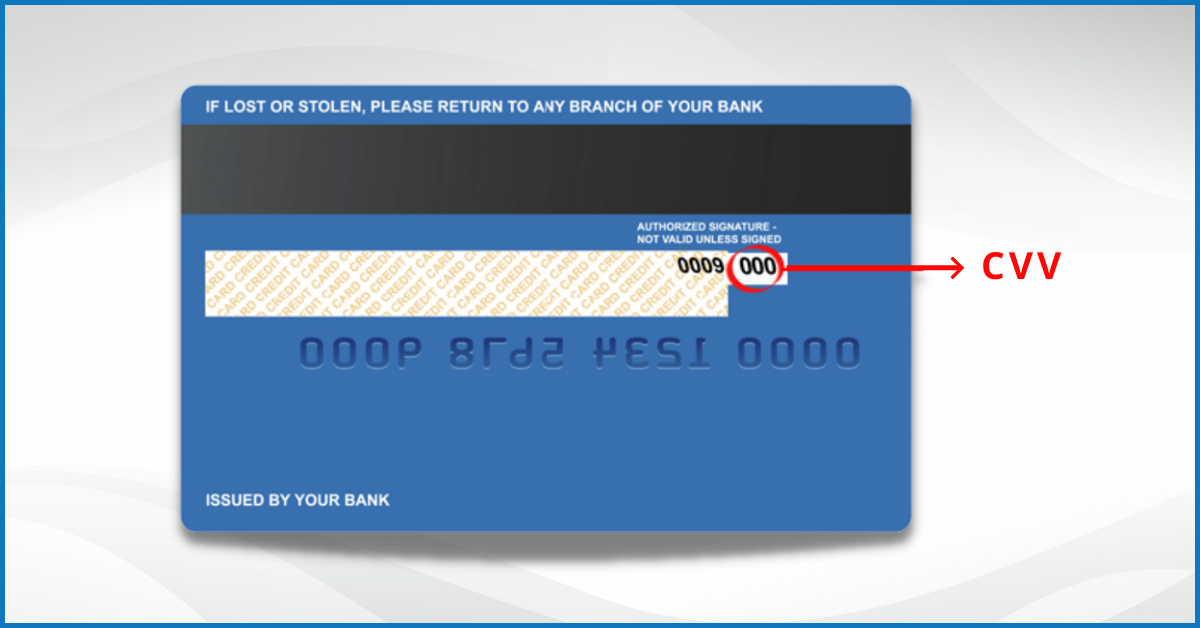

Deciphering the CVV: Location and Variations

The CVV’s appearance and terminology can vary slightly depending on the card network, but its function remains the same. Understanding where to find it and what it’s called can prevent confusion.

Identifying the CVV on Major Card Networks

- Visa: For Visa cards, the CVV is a three-digit number located on the back of the card, typically in or near the signature strip. It is often labeled as “CVV.”

- Mastercard: Similar to Visa, Mastercard also uses a three-digit CVV found on the back of the card, usually in the signature area. It is also often labeled as “CVV.”

- Discover: Discover cards feature a four-digit code on the front of the card, usually above the embossed account number. This is referred to as the Card Identification Number (CID).

- American Express: American Express cards have a four-digit code, known as the Card Identification Number (CID), printed on the front of the card, typically above the embossed account number.

The Significance of Not Storing the CVV

A crucial aspect of CVV security is that merchants are prohibited from storing this code after the transaction is authorized. This rule, enforced by the Payment Card Industry Data Security Standard (PCI DSS), is a cornerstone of preventing large-scale data breaches involving CVVs. While merchants can store card numbers, expiration dates, and cardholder names, they cannot retain the CVV. This ensures that even if a merchant’s systems are hacked, the CVVs are not compromised, making stolen card numbers less valuable to cybercriminals.

The Role of CVV in Transaction Authorization

The CVV’s involvement in the authorization process is sophisticated and happens behind the scenes. It’s a quick check that adds a significant layer of confidence for both the consumer and the payment processor.

How the CVV Verifies Cardholder Presence

When you enter your CVV during an online or phone transaction, it’s sent along with your other card details to the payment processor. This information is then relayed to the card-issuing bank for verification. The issuing bank checks if the provided CVV matches the code associated with that specific card. If the numbers align, it provides strong evidence that the person initiating the transaction is in possession of the physical card. This verification is a critical step in the authorization process and helps to prevent fraudulent transactions where a stolen card number might be used without the physical card.

CVV and Tokenization: A Combined Defense

While the CVV is a powerful security tool on its own, it’s often used in conjunction with other security measures, such as tokenization, to further enhance transaction security. Tokenization replaces sensitive card information with a unique, randomly generated string of characters called a token. This token can be used for transactions without revealing the actual card details. In some tokenized systems, the CVV might still be used for initial verification, but the ongoing transactions would rely on the token, reducing the risk if the token itself were compromised. This multi-layered approach creates a robust defense system for digital payments.

Protecting Your CVV and Preventing Fraud

While the CVV is designed to protect you, it’s essential to understand that it’s still a piece of sensitive information that needs safeguarding. Treat it with the same caution as your card number and PIN.

Best Practices for CVV Security

- Never Share Your CVV Unnecessarily: Only provide your CVV for legitimate transactions where you are making the purchase. Be wary of unsolicited requests for your CVV over email or phone.

- Be Cautious of Phishing Attempts: Fraudsters may try to trick you into revealing your CVV through fake websites or emails that mimic legitimate companies. Always verify the legitimacy of a website or sender before entering any card details.

- Secure Your Physical Card: If your card is lost or stolen, report it immediately to your bank. This will not only deactivate the card but also prevent any unauthorized transactions, including those that might require the CVV.

- Regularly Review Your Statements: Keep an eye on your bank and credit card statements for any suspicious or unauthorized transactions. If you spot something out of the ordinary, report it to your bank immediately. Early detection is key to mitigating financial losses.

- Use Strong Passwords for Online Accounts: While not directly related to the CVV, strong passwords for your online shopping accounts are crucial for overall digital security. If an account is compromised, it could potentially lead to a situation where card details are exposed.

Understanding CVV’s Limitations

It’s important to acknowledge that the CVV is not foolproof. While it significantly enhances security, it’s not an infallible shield against all types of fraud. For instance, if a fraudster gains physical access to your card, they can easily see and use the CVV. Similarly, sophisticated phishing attacks or malware could potentially capture your CVV along with other card details. This is why a comprehensive approach to security, encompassing strong personal practices and the adoption of advanced security technologies by financial institutions, is essential. The CVV is a vital component of this ecosystem, but it’s most effective when used as part of a broader security strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.