Tax season is often viewed with a mixture of trepidation and necessity. For the average taxpayer, the primary goal is twofold: ensuring total compliance with the Internal Revenue Service (IRS) and maximizing the potential refund. In the landscape of modern personal finance, TurboTax has established itself as the premier software solution for navigating the complexities of the tax code. However, the platform offers a variety of tiers, each tailored to specific financial profiles. Selecting the wrong version can lead to unnecessary expenditures on features you don’t need or, conversely, a failure to capture critical deductions that could save you thousands.

To determine which TurboTax version aligns with your financial reality, you must first audit your income streams, investment portfolio, and household expenses. This guide provides a professional deep dive into the TurboTax ecosystem, helping you identify the specific tool required to optimize your financial standing this year.

Understanding Your Financial Profile: The First Step in Selection

Before diving into the software specifications, it is essential to categorize your financial life. The IRS categorizes taxpayers based on the complexity of their income and the nature of their expenses. Your choice of tax software is a direct reflection of these categories.

Simple Returns and the Standard Deduction

For many early-career professionals or students, financial life is relatively straightforward. If your primary source of income is a standard W-2 from a single employer and you do not own a home or significant investments, you likely fall into the “simple return” category. In this scenario, you are usually claiming the standard deduction rather than itemizing. The financial tool needed here is one that prioritizes speed and accuracy over complex form-filling.

Itemizing Deductions and Homeownership

As your net worth grows and your financial responsibilities shift, the “simple” approach often becomes insufficient. Homeownership introduces mortgage interest deductions and property tax considerations. Furthermore, if you live in a state with high income taxes or if you make significant charitable contributions, your total itemized deductions may exceed the standard deduction. At this stage, your software needs to transition from a basic filing tool to a comprehensive financial scanner that looks for “hidden” tax breaks.

Analyzing the TurboTax Tiers: From Basic Filing to Complex Business Needs

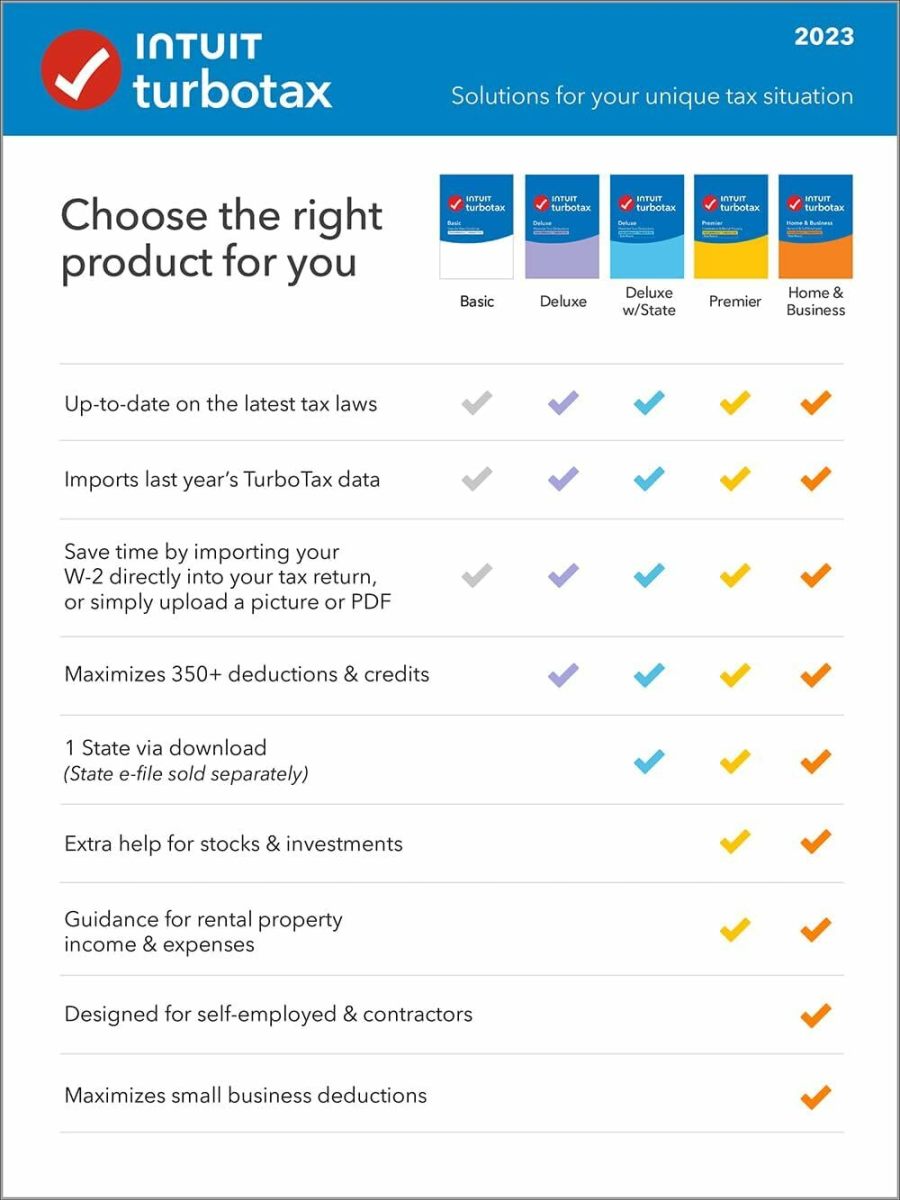

TurboTax categorizes its products into several distinct levels. Each level is designed to handle specific financial forms and schedules. Choosing the right one is a matter of matching your financial documents (1094s, 1099s, K-1s) to the software’s capabilities.

TurboTax Free Edition vs. Deluxe

The Free Edition is strictly for simple tax returns (Form 1040 only). It is designed for those whose financial footprint is minimal. However, most taxpayers find that the Deluxe version is the “sweet spot” for personal finance optimization. The Deluxe version is engineered to search over 350 deductions and credits. From a wealth management perspective, the Deluxe tier is essential if you want to ensure that your home-related expenses and education credits are accurately accounted for, preventing “money left on the table.”

TurboTax Premier for Investors

For those engaged in wealth building through the capital markets, TurboTax Premier is the non-negotiable choice. This version is specifically tuned for investment income. If you sold stocks, bonds, or mutual funds during the fiscal year, you are required to report capital gains or losses. Premier automates the import of thousands of transactions from financial institutions, ensuring that your cost-basis reporting is precise. This is critical for tax-loss harvesting—a sophisticated financial strategy where you offset capital gains with losses to minimize your overall tax liability.

TurboTax Self-Employed and Small Business

The rise of the “gig economy” and independent consulting has fundamentally changed the financial landscape. If you receive 1099-NEC or 1099-K forms, you are essentially a small business owner in the eyes of the IRS. The Self-Employed version (and the standalone TurboTax Business for S-Corps and Partnerships) provides the necessary infrastructure to file Schedule C. It allows you to deduct industry-specific expenses, such as home office costs, travel, and equipment. For the self-employed, this software is less of a “filing tool” and more of a “business expense optimizer.”

The Impact of Life Changes on Your Software Choice

Financial situations are rarely static. Significant life events—often referred to as “taxable events”—can shift you from one TurboTax tier to another in a single year. Understanding these shifts is vital for maintaining an accurate long-term financial plan.

Handling Cryptocurrency and Stock Trades

The integration of digital assets into personal portfolios has added a layer of complexity to modern finance. Cryptocurrency is treated as property by the IRS, meaning every trade, sale, or exchange is a taxable event. If your financial year included moving Bitcoin to cold storage after a sale or trading Ethereum for another token, you require the Premier tier. The software’s ability to sync with crypto exchanges is a vital technological feature that prevents manual entry errors, which are a leading cause of IRS audits.

Rental Property Income and Management

Real estate remains one of the most effective vehicles for building generational wealth. However, being a landlord introduces complex depreciation schedules and expense tracking. If you own rental property, the Premier version is again the required tool. It guides you through the process of calculating rental income versus expenses like repairs, insurance, and management fees. From a personal finance standpoint, correctly calculating depreciation is one of the most significant ways to reduce your taxable income, and the software ensures this is done according to current tax laws.

Maximizing Value: Features and Support Options

When selecting a financial tool, one must consider the “Value of Time” versus the “Cost of Service.” TurboTax has expanded its offerings to include different levels of human intervention, which can be a wise investment depending on your comfort level with financial regulations.

Full Service vs. Live Assisted

TurboTax Live Assisted allows you to navigate the software yourself while having access to a CPA or Enrolled Agent on demand. This is an excellent middle ground for those with a moderately complex portfolio who want the peace of mind that comes with professional verification. TurboTax Full Service, on the other hand, involves handing your documents over to a professional who handles the entire process. From a business finance perspective, this is often a “tax-deductible” expense in itself, and the time saved can be reinvested into your primary income-generating activities.

The Cost-Benefit Analysis of Professional Review

Is it worth paying the extra $50 to $100 for a higher tier or live support? In the world of finance, the answer is usually found in the “Effective Tax Rate.” If the software identifies a single credit—such as the Earned Income Tax Credit (EITC) or a specific energy-efficient home improvement credit—it frequently pays for itself five times over. A professional review can also mitigate the risk of an audit, which carries a high “stress cost” and potential financial penalties.

Future-Proofing Your Tax Strategy with Financial Tools

The decision of which TurboTax to use should not be made in a vacuum. It should be part of a broader annual financial review. By using the right software, you gain insights into your spending and earning patterns that can inform your strategy for the following year.

Integrating with Budgeting Apps and Bank Feeds

Modern TurboTax versions allow for the seamless import of data from financial aggregators and banks. This integration is a cornerstone of “FinTech” (Financial Technology). By seeing your year in review through the lens of a tax return, you can identify where you might be over-leveraged or where you could increase contributions to tax-advantaged accounts like a 401(k) or an HSA.

Planning for the Upcoming Fiscal Year

The “Tax Reform” feature within the higher tiers of TurboTax allows you to run “what-if” scenarios. For example, if you are considering selling a business or purchasing a second home, you can use the software to estimate the impact on your future liquidity. This transform’s the software from a reactive filing tool into a proactive financial planning instrument.

In conclusion, choosing the right TurboTax version is a strategic financial decision. If you are a student or a simple W-2 earner, the Free or Deluxe versions are your path to efficiency. If you are building wealth through the stock market or real estate, Premier is your analytical partner. And if you are an entrepreneur or freelancer, the Self-Employed version is your primary tool for protecting your bottom line. By matching the software’s capabilities to your financial complexity, you ensure that you are not just “doing your taxes,” but actively managing your wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.