The prime lending rate, often referred to as the prime rate, is a fundamental benchmark in the financial world. It represents the interest rate that commercial banks charge their most creditworthy corporate customers. However, its influence extends far beyond large corporations, directly impacting the borrowing costs for individuals and small businesses alike. Understanding the current prime lending rate and the factors that drive its fluctuations is crucial for anyone managing their personal finances, seeking loans, or operating a business.

This article will delve into the intricacies of the prime lending rate, exploring its origins, how it’s determined, its significance in the broader economic landscape, and its tangible effects on various financial products and decisions.

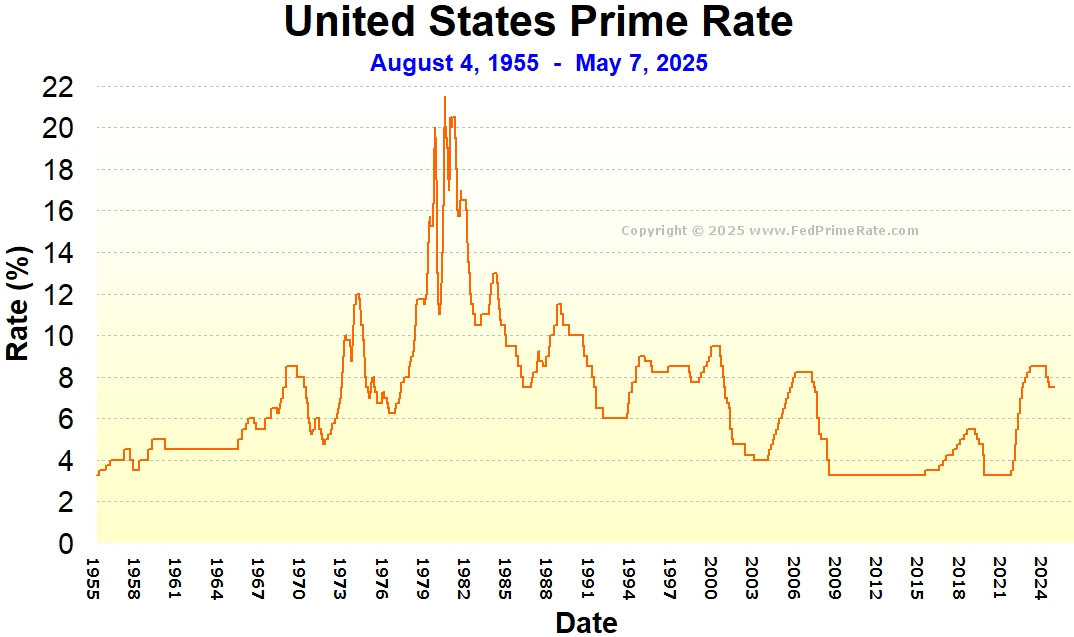

The Genesis and Determination of the Prime Lending Rate

The concept of a “prime” customer implies a borrower with the lowest risk of default. Historically, banks would set their prime rate based on their own internal cost of funds and perceived risk. However, in the modern financial era, the prime lending rate has become more standardized and closely tied to a widely recognized benchmark.

The Federal Funds Rate as the Primary Driver

The Federal Funds Rate as the Primary Driver

The most significant determinant of the U.S. prime lending rate is the federal funds rate. This is the target interest rate at which commercial banks lend reserve balances to other depository institutions overnight on an uncollateralized basis. The Federal Reserve, through its Federal Open Market Committee (FOMC), sets this target rate as a primary tool of monetary policy.

When the FOMC decides to increase the federal funds rate, it becomes more expensive for banks to borrow from each other. This increased cost of funds is then passed on to their customers, including the prime lending rate. Conversely, when the FOMC lowers the federal funds rate, the cost of borrowing for banks decreases, leading to a reduction in the prime rate. The relationship is typically direct and almost immediate: a quarter-point increase in the federal funds rate usually translates to a quarter-point increase in the prime rate.

The “Prime Plus” Formula

While the federal funds rate is the primary influence, the actual prime rate published by major banks isn’t solely a direct copy of the federal funds rate. Historically, the prime rate was often quoted as a specific percentage, such as 3% or 5%. However, in recent decades, the prime rate has largely transitioned to a “prime plus” formula. This means the prime rate is officially set as a specific margin above the federal funds rate.

For example, if the federal funds rate is 5.25%, a common prime rate might be set at 8.25% (5.25% + 3%). This 3% spread is a historical convention and a profit margin for banks. While this spread has remained relatively stable, it’s important to remember that the underlying federal funds rate is the dynamic component. When the federal funds rate moves, the prime rate moves in lockstep, maintaining that 3% differential (or whatever the prevailing spread is for a given bank).

The Role of Major Banks and Financial Publications

While many banks have their own published prime rates, there’s a general consensus among major financial institutions regarding the prevailing prime lending rate. Publications like The Wall Street Journal survey major banks to track their prime rates, and the consensus rate is widely adopted. This standardization ensures a degree of predictability and comparability across the financial system. When a bank announces a change in its prime rate, it almost invariably aligns with the changes made by other major players.

The Pervasive Influence of the Prime Lending Rate on Borrowing Costs

The prime lending rate is not an isolated economic indicator; it acts as a foundational rate upon which countless other interest rates are built. Its fluctuations have a ripple effect across the entire spectrum of borrowing, impacting both consumers and businesses.

Variable-Rate Loans and Credit Cards

Variable-Rate Loans and Credit Cards

One of the most direct and common impacts of the prime lending rate is on variable-rate loans and credit cards. Many credit cards, especially those offering introductory low rates or balance transfers, have an annual percentage rate (APR) that is tied to the prime rate. This APR is typically expressed as “Prime + X%,” where “X” represents a variable margin determined by the card issuer based on your creditworthiness.

For instance, if your credit card APR is currently “Prime + 15%,” and the prime rate increases from 8.25% to 8.50%, your APR will automatically increase from 23.25% (8.25% + 15%) to 23.50% (8.50% + 15%). This means the interest you pay on outstanding balances will immediately go up. Similarly, home equity lines of credit (HELOCs) and some auto loans often carry variable rates directly linked to the prime rate, making their monthly payments subject to change as the prime rate adjusts.

Mortgages and Other Fixed-Rate Products

While fixed-rate mortgages might seem immune to changes in the prime lending rate, the connection is more subtle but still significant. The prime rate is a strong indicator of the overall cost of borrowing in the economy. When the prime rate is high, it generally signifies a tightening monetary policy and a higher cost of capital for lenders. This, in turn, influences the yields on longer-term debt instruments, like U.S. Treasury bonds, which are key benchmarks for fixed-rate mortgage pricing.

Therefore, while a fixed-rate mortgage’s interest rate won’t change once it’s locked in, the initial rate offered will be higher when the prime rate is elevated. Conversely, during periods of low prime rates, fixed mortgage rates tend to be more attractive. Beyond mortgages, other fixed-rate loans, such as personal loans or some student loans, will also reflect the prevailing interest rate environment influenced by the prime rate when they are originated.

Business Loans and Lines of Credit

For businesses, the prime lending rate is a critical factor in their operational costs and expansion plans. Many business loans and lines of credit are directly priced off the prime rate, often using the “Prime + X%” model similar to consumer credit. This means that as the prime rate rises, the cost of borrowing for businesses increases, impacting their profitability and cash flow.

This increased cost of capital can have several consequences for businesses:

- Reduced Investment: Higher borrowing costs can make new projects and capital expenditures less attractive, potentially slowing down business growth and innovation.

- Increased Operating Expenses: For businesses that rely on lines of credit for day-to-day operations, such as managing inventory or payroll, rising interest payments can significantly strain their budget.

- Impact on Profit Margins: The cost of debt is a direct expense. For businesses with significant debt, an increase in the prime rate can lead to a noticeable reduction in their profit margins.

- Difficulty Securing Financing: In a high-interest-rate environment, lenders may become more cautious, making it harder for businesses, especially smaller ones or those with less robust credit profiles, to secure the financing they need.

Navigating Your Finances in a Shifting Prime Rate Environment

Understanding the current prime lending rate is not just an academic exercise; it has practical implications for your financial well-being. Whether you’re a consumer managing personal debt or a business owner making strategic decisions, awareness of the prime rate’s movement allows for more informed planning and action.

Strategies for Consumers

For individuals, the prime lending rate’s influence is most keenly felt through their credit cards, HELOCs, and other variable-rate debts. Here are some strategies to consider:

- Monitor Your Variable-Rate Debts: Regularly check the terms of your credit cards and other variable-rate loans. Understand how your interest rate is calculated (e.g., Prime + X%) and keep an eye on changes in the prime rate.

- Consider Refinancing or Consolidation: If you have significant balances on variable-rate credit cards and interest rates are rising, explore options to refinance that debt into a fixed-rate loan or a balance transfer to a card with a 0% introductory APR. This can lock in your interest rate for a period, providing payment stability.

- Aggressively Pay Down Debt: When interest rates are high, the cost of carrying debt increases significantly. Prioritizing paying down balances on variable-rate accounts can help you save on interest payments over time.

- Build an Emergency Fund: A robust emergency fund can prevent you from relying on high-interest credit cards or loans when unexpected expenses arise, especially during periods of rising interest rates.

Strategies for Businesses

Businesses need to be particularly agile in managing their finances when the prime lending rate is in flux.

- Review Loan Covenants and Terms: Businesses with existing loans tied to the prime rate should carefully review their loan agreements. Understand the specific margin above prime and how often payments will be adjusted.

- Explore Fixed-Rate Financing Options: If your business anticipates needing significant financing in the future, or if you have existing variable-rate debt, investigate the possibility of securing fixed-rate loans or locking in rates for existing credit lines. While fixed rates might be higher initially than current variable rates, they offer protection against future increases.

- Optimize Cash Flow Management: With potentially higher borrowing costs, meticulous cash flow management becomes even more critical. Forecast expenses and revenues accurately, and look for opportunities to reduce operational costs.

- Diversify Funding Sources: Relying on a single source of financing can be risky. Explore different types of loans, lines of credit, and even alternative funding options to ensure financial flexibility.

- Budget for Higher Interest Expenses: Businesses should proactively adjust their budgets to account for potential increases in interest expenses. This proactive approach can prevent unexpected financial strains.

The Broader Economic Context

The prime lending rate is not set in a vacuum; it’s a reflection of the broader economic conditions and the Federal Reserve’s monetary policy objectives. The Fed typically raises interest rates to combat inflation, aiming to cool down an overheating economy by making borrowing more expensive and encouraging saving. Conversely, they lower rates to stimulate economic growth during downturns by making borrowing cheaper and encouraging spending and investment.

Understanding these broader economic trends can provide valuable foresight into potential future movements of the prime lending rate. For instance, if inflation is persistently high, it’s likely the Fed will continue to raise interest rates, leading to a higher prime rate. Conversely, if the economy shows signs of slowing down significantly, rate cuts may be on the horizon, potentially leading to a lower prime rate. Staying informed about economic indicators, inflation reports, and Federal Reserve statements is therefore an integral part of anticipating changes in the prime lending rate.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.