A Health Savings Account (HSA) is a powerful financial tool designed to help individuals manage their healthcare expenses while simultaneously offering significant tax advantages. For those enrolled in a High Deductible Health Plan (HDHP), an HSA presents an opportunity to save, invest, and spend on qualified medical costs with unparalleled flexibility. Understanding its mechanics is crucial for maximizing its benefits and integrating it effectively into your overall financial strategy.

Understanding the Fundamentals of a Health Savings Account

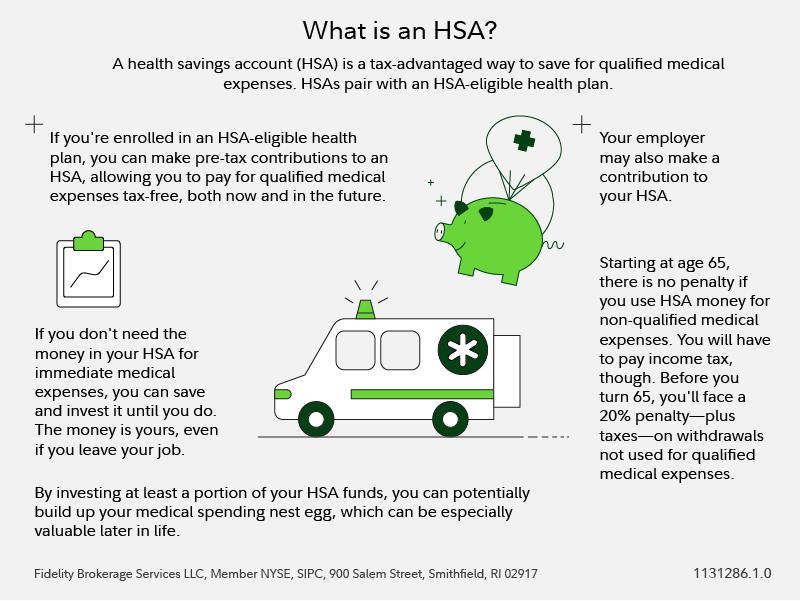

At its core, an HSA is a tax-advantaged savings account specifically earmarked for healthcare expenses. It’s a tripartite agreement between the account holder, the financial institution holding the funds, and the IRS, which dictates the tax benefits. The primary prerequisite for opening and contributing to an HSA is enrollment in a qualifying High Deductible Health Plan (HDHP). This type of health insurance plan typically has a lower monthly premium but a higher deductible that must be met before the insurance begins to cover most medical costs.

The Eligibility Requirements for an HSA

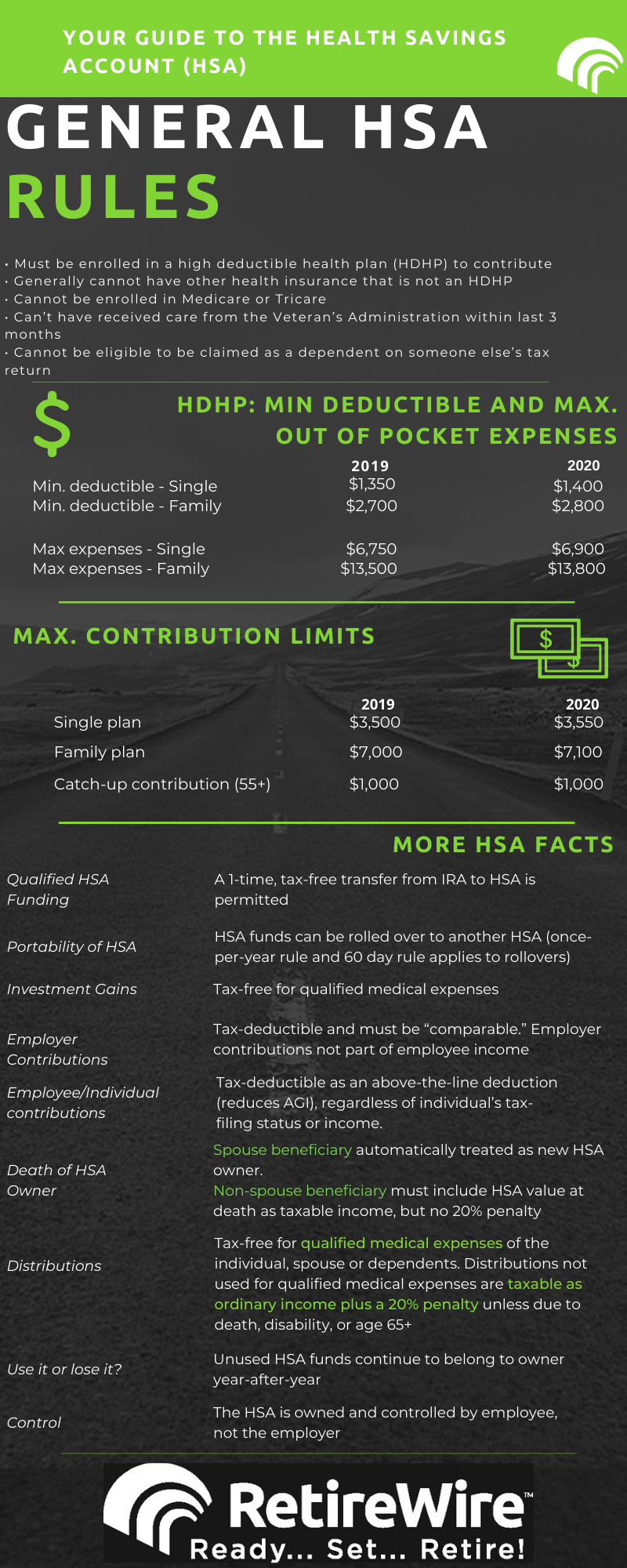

To be eligible for an HSA, you must meet several criteria established by the IRS. Firstly, as mentioned, you must be covered by an HDHP. For the current tax year, the IRS sets specific minimum deductible amounts and maximum out-of-pocket expense limits for HDHPs. These figures are adjusted annually to account for inflation. For instance, for 2023, a qualifying HDHP must have a deductible of at least $1,500 for self-only coverage and $3,000 for family coverage. The maximum out-of-pocket expenses cannot exceed $7,500 for self-only coverage and $15,000 for family coverage.

Secondly, you cannot be enrolled in Medicare, which is a federal health insurance program for people aged 65 or older, certain younger people with disabilities, and people with End-Stage Renal Disease. Once you are enrolled in Medicare, you are no longer eligible to contribute to an HSA. Thirdly, you cannot be claimed as a dependent on someone else’s tax return. This means that if your parents still claim you as a dependent, you cannot open or contribute to your own HSA. Finally, you cannot have other health coverage that is not considered an HDHP, unless it’s specifically allowed by the IRS (e.g., vision or dental insurance, specific disease or accident coverage).

The Triple Tax Advantage of HSAs

The most compelling aspect of HSAs is their unparalleled triple tax advantage, which sets them apart from other savings vehicles like 401(k)s or traditional IRAs.

Tax-Deductible Contributions

Contributions made to an HSA are tax-deductible. This means that the money you contribute is subtracted from your taxable income, reducing your overall tax liability for the year. Whether you contribute directly through your employer via payroll deductions or make contributions yourself, these funds are excluded from your gross income. This deduction is available regardless of whether you itemize deductions or take the standard deduction, making it a universally beneficial tax break.

Tax-Deferred Growth

Once the money is in your HSA, any earnings it generates are allowed to grow on a tax-deferred basis. Similar to other investment accounts, your HSA funds can be invested in a variety of options, such as stocks, bonds, and mutual funds. As these investments grow, any dividends, interest, or capital gains are not taxed annually. This allows your savings to compound more effectively over time, as you are not paying taxes on the growth year after year. This is a significant advantage for long-term healthcare savings and wealth accumulation.

Tax-Free Withdrawals for Qualified Medical Expenses

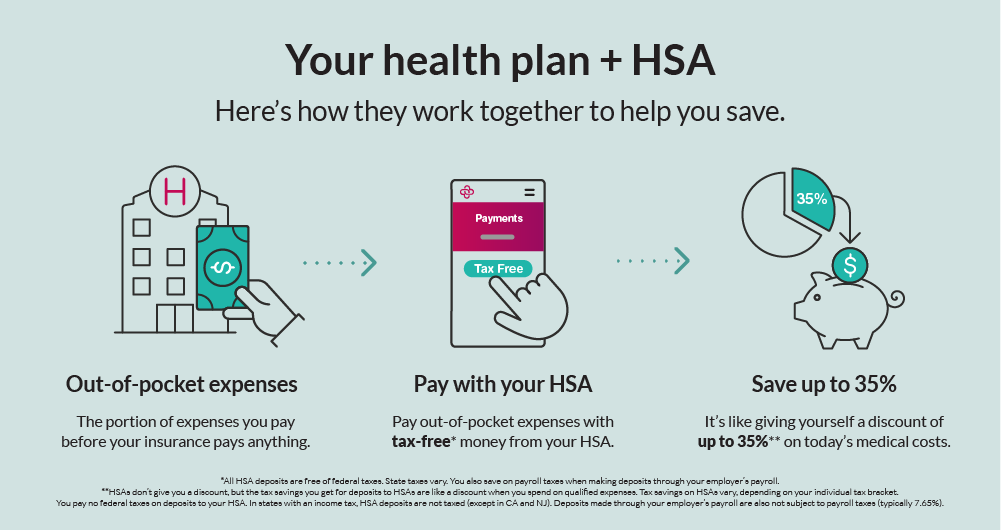

The ultimate benefit of an HSA is realized when you withdraw funds to pay for qualified medical expenses. When used for these purposes, the withdrawals are entirely tax-free. This includes not only routine medical care but also a wide range of other health-related costs. The IRS provides a comprehensive list of qualified medical expenses, which generally encompass costs that could be deducted if you itemized medical expenses. This means you can use your HSA funds to cover deductibles, co-payments, prescription medications, dental care, vision care, and even certain long-term care insurance premiums.

How an HSA Works in Practice

The operational mechanics of an HSA are designed for simplicity and flexibility, allowing account holders to manage their funds efficiently. From making contributions to utilizing the funds for medical needs and even investing, the process is straightforward.

Contributing to Your HSA

Contributions to an HSA can be made in two primary ways: through your employer or directly by you.

Employer Contributions

Many employers offer HSAs as part of their benefits package, especially for employees enrolled in an HDHP. These contributions are typically made through payroll deductions. The advantage here is that these contributions are made pre-tax, meaning they reduce your taxable income before taxes are calculated. This is often referred to as “pre-tax dollars.” Your employer will likely have a specific HSA provider they partner with, and you will need to set up your account through them.

Individual Contributions

If your employer does not offer an HSA, or if you wish to contribute more than your employer allows, you can make direct contributions to your HSA. These contributions are made with after-tax dollars, but you can then deduct them from your taxable income when you file your federal income tax return. This is done using IRS Form 8889, Health Savings Accounts (HSAs). It’s important to keep track of all contributions, both from your employer and directly from you, to ensure you do not exceed the annual contribution limit.

The IRS sets annual limits on how much an individual or family can contribute to an HSA. For 2023, the maximum contribution for self-only HDHP coverage is $3,850, and for family HDHP coverage, it’s $7,750. Individuals aged 55 and older can make an additional catch-up contribution of $1,000 per year. These limits are designed to encourage responsible saving for healthcare needs without allowing for excessive tax sheltering.

Spending Your HSA Funds

The flexibility of an HSA extends to how and when you can use the funds. You can use your HSA funds at any time to pay for qualified medical expenses, even if you haven’t met your health plan’s deductible yet.

Using Funds for Qualified Medical Expenses

The IRS defines a broad range of expenses that qualify for tax-free withdrawal from an HSA. This includes:

- Medical Insurance Deductibles and Co-payments: The most common use for HSA funds is to cover the costs associated with your HDHP deductible and any co-pays you incur for doctor visits or prescriptions.

- Prescription Drugs: Both over-the-counter and prescription medications are generally considered qualified expenses.

- Dental and Vision Care: Expenses for dental check-ups, cleanings, fillings, braces, eye exams, eyeglasses, and contact lenses are eligible.

- Medical Equipment and Supplies: This can include items like crutches, bandages, and diagnostic devices.

- Therapy and Rehabilitation Services: Physical therapy, occupational therapy, and mental health counseling can be paid for with HSA funds.

- Premiums for Long-Term Care Insurance: A portion of the premiums paid for qualified long-term care insurance policies can be reimbursed from an HSA.

- Qualified Medical Expenses for Dependents: You can also use your HSA funds to pay for the qualified medical expenses of your spouse and any dependents you claim on your tax return.

It’s essential to retain records of all medical expenses paid with HSA funds, as well as receipts for those expenses, in case the IRS requests verification.

Accessing Your Funds

HSAs typically come with a debit card linked to the account, making it convenient to pay for services at the point of care. Alternatively, you can pay for expenses out-of-pocket and then submit a reimbursement request to your HSA administrator. Many HSA providers also offer online portals or mobile apps where you can manage your account, view transactions, and initiate reimbursements.

Investing Your HSA Funds for Long-Term Growth

Beyond simply saving for immediate healthcare needs, HSAs offer a powerful avenue for long-term wealth building through investment. As mentioned earlier, the tax-deferred growth characteristic of HSAs makes them an attractive investment vehicle.

The Investment Component of an HSA

Most HSA providers offer a range of investment options, allowing you to grow your savings beyond simple interest. These options typically mirror those found in retirement accounts like 401(k)s and often include:

- Mutual Funds: These are pooled investment vehicles that allow you to diversify across various stocks, bonds, or other securities. You can choose from a wide array of fund types, including index funds, actively managed funds, and target-date funds.

- Exchange-Traded Funds (ETFs): Similar to mutual funds, ETFs are baskets of securities that trade on stock exchanges. They are often favored for their lower expense ratios.

- Stocks and Bonds: Some HSA providers allow direct investment in individual stocks and bonds, offering more control but also potentially higher risk.

The specific investment options available will vary depending on your HSA administrator. It’s important to research these options and select investments that align with your risk tolerance and financial goals.

Strategies for Investing HSA Funds

The dual purpose of an HSA – to cover current healthcare costs and to save for the future – necessitates a thoughtful investment strategy.

Balancing Liquidity and Growth

A key consideration is balancing the need for readily accessible funds for immediate medical expenses with the desire to grow your savings for long-term goals, such as retirement or future healthcare needs that may arise after you’re no longer eligible to contribute. For immediate or near-term healthcare needs, keeping a portion of your HSA in a stable cash or money market fund can provide liquidity. For funds you anticipate not needing for several years, investing them in a diversified portfolio of stocks and bonds can yield significant long-term growth.

Long-Term Retirement Planning

Many individuals view their HSA as a supplemental retirement account. Since withdrawals for qualified medical expenses are tax-free at any age, and after age 65, withdrawals for any purpose are treated like those from a traditional IRA (meaning they are taxed as ordinary income, but without penalty), your HSA can provide a flexible source of funds in retirement. This is particularly beneficial for covering the increasing healthcare costs that often accompany aging. By consistently contributing and investing your HSA funds over your working life, you can build a substantial nest egg that addresses both healthcare and general living expenses in your later years.

Tax Implications and Portability of HSAs

Understanding the tax rules surrounding HSAs and their portability is crucial for effective management and long-term financial planning.

Tax Reporting and Contribution Limits

As previously mentioned, all HSA contributions and distributions must be reported on your federal tax return. You will use IRS Form 8889 to report these activities. It’s your responsibility to ensure you do not exceed the annual contribution limits. Exceeding these limits can result in excise taxes. Keeping meticulous records of all contributions, reimbursements, and expenditures is vital for accurate tax reporting and to avoid potential penalties.

HSA Portability and Rollover Options

One of the most significant advantages of an HSA is its portability. If you change employers, lose your job, or no longer have an HDHP, you retain ownership of your HSA. The funds in your HSA are yours to keep and manage, irrespective of your employment status or health insurance coverage.

Transferring Funds

If you switch to a different HSA provider, you can typically transfer your existing HSA funds to the new provider. This can be done through a direct trustee-to-trustee transfer, which does not count as a taxable distribution. Alternatively, you can request a distribution yourself and then deposit the funds into the new HSA within 60 days, though this method carries more risk and requires careful management to avoid taxes and penalties.

What Happens After Retirement or Losing HDHP Coverage

Even if you are no longer eligible to contribute to an HSA (e.g., you enroll in Medicare or switch to a non-HDHP plan), you can still keep the funds in your HSA and use them tax-free for qualified medical expenses. As mentioned, once you turn 65, you can withdraw funds for any purpose without penalty, although these withdrawals will be subject to ordinary income tax, similar to a traditional IRA distribution. This feature makes HSAs an incredibly versatile tool for managing healthcare costs throughout your life and can serve as a valuable supplement to your retirement savings.

In conclusion, a Health Savings Account is a sophisticated financial instrument offering substantial tax benefits for individuals with High Deductible Health Plans. By understanding its eligibility requirements, contribution methods, spending rules, and investment opportunities, account holders can effectively leverage their HSA to manage current medical costs, build long-term wealth, and secure their financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.