The implosion of Enron Corporation stands as one of the most infamous and cautionary tales in modern financial history. Once lauded as an innovative energy giant, its spectacular collapse in late 2001 sent shockwaves through the global economy, leading to the loss of billions of dollars for investors, the decimation of employee pensions, and a profound erosion of public trust in corporate America. While often remembered for its sheer scale and audacity, a deeper examination of Enron’s demise reveals a complex web of financial engineering, ethical bankruptcy, and a systemic failure of oversight that continues to inform corporate governance and financial regulation today. This article delves into the multifaceted story of Enron’s rise and fall, focusing on the financial machinations that fueled its growth and ultimately led to its catastrophic end.

The Illusion of Growth: Aggressive Accounting and Financial Engineering

Enron’s meteoric rise was fueled by a relentless pursuit of growth, often at the expense of genuine profitability. The company masterfully employed complex financial instruments and accounting loopholes to present an image of robust and consistent earnings, masking a far more precarious reality. This section explores the key accounting practices and financial strategies that formed the bedrock of Enron’s fraudulent edifice.

Mark-to-Market Accounting: A Double-Edged Sword

One of Enron’s most significant and ultimately destructive accounting tools was the widespread application of mark-to-market accounting. Introduced in the energy trading business, this method allowed companies to record projected profits from long-term contracts immediately, even if those profits were years away and highly speculative. In theory, mark-to-market could provide a more accurate reflection of an asset’s current value. However, at Enron, it became a potent instrument for inflating reported earnings.

- Projecting Unrealistic Future Profits: Enron executives and traders were incentivized to make optimistic, often wildly inaccurate, projections about the future profitability of their complex energy contracts. These projections, however dubious, were immediately recognized as revenue and profit, irrespective of whether the underlying deals ever generated actual cash flow.

- Obscuring Risk: By recognizing potential profits upfront, the inherent risks associated with these speculative long-term contracts were effectively hidden from investors and the public. The volatile nature of energy markets meant that many of these projected profits never materialized, leading to significant hidden losses.

- The Incentive for Deception: The mark-to-market system created a powerful incentive for traders and executives to manipulate future estimates to meet Wall Street’s ever-increasing expectations. This fostered a culture where accounting, rather than sound business operations, became the primary driver of reported success.

Special Purpose Entities (SPEs): The Art of Hiding Debt

Perhaps the most infamous aspect of Enron’s financial deception was its extensive use of Special Purpose Entities, or SPEs. These were off-balance-sheet entities, often thinly capitalized, created to engage in specific financial transactions. Enron, under the guidance of Chief Financial Officer Andrew Fastow, utilized SPEs not merely for legitimate risk management but primarily to conceal massive amounts of debt and failing assets from its financial statements.

- Concealing Debt and Losses: By transferring assets and liabilities to SPEs that were technically independent, Enron could remove them from its own balance sheet, thereby reducing its reported debt levels and avoiding the recognition of losses on underperforming investments. This made the company appear far healthier and less leveraged than it actually was.

- Inflating Earnings Through “Asset Sales”: Enron would “sell” assets to its own SPEs, often for cash that was itself financed by debt taken on by the SPE, which was implicitly or explicitly guaranteed by Enron. These transactions were structured to generate accounting gains, further boosting Enron’s reported profits.

- The Predator and the Prey: Many of these SPEs were managed or controlled by Enron executives, including Fastow himself. This created blatant conflicts of interest, as these individuals profited personally from transactions that were detrimental to the company and its shareholders. The SPEs effectively became vehicles for personal enrichment at the expense of the corporation.

The Role of Executive Compensation and Incentives

The corporate culture at Enron was deeply ingrained with a performance-driven ethos, but the metrics used to define “performance” were heavily skewed towards short-term financial gains, often achieved through aggressive accounting. Executive compensation packages were intrinsically linked to reported earnings and stock price, creating a powerful incentive to maintain the illusion of success at all costs.

- Stock Options and the Pressure to Perform: Executives were granted large stock options, their value directly tied to the company’s stock price. This created immense pressure to continually increase reported earnings and thus the stock price, regardless of the underlying economic reality. When reported numbers faltered, the temptation to manipulate them became overwhelming.

- Bonuses Tied to Inflated Profits: Annual bonuses and other incentives were often calculated based on financial targets that were achieved through the aggressive accounting practices described above. This created a feedback loop where fraudulent behavior was rewarded, further entrenching the deceptive practices within the organization.

- A Culture of “Winning at All Costs”: Enron fostered a competitive and aggressive culture, often characterized by a “can-do” attitude that blurred the lines between ambition and unethical conduct. This environment, coupled with the financial incentives, created a fertile ground for the widespread acceptance of questionable accounting and business practices.

The Erosion of Trust: Auditing Failures and Analyst Complicity

The sophisticated financial engineering at Enron would have been difficult to maintain without the tacit approval or outright complicity of external parties. The failure of its auditors and the relative silence of financial analysts played crucial roles in perpetuating the deception and allowing Enron’s collapse to be so devastating.

Arthur Andersen’s Abdication of Responsibility

![]()

Arthur Andersen, one of the “Big Five” accounting firms at the time, served as Enron’s auditor. The firm’s primary responsibility was to provide an independent and objective opinion on Enron’s financial statements. However, Andersen’s performance in this role was severely compromised.

- Conflicts of Interest: Arthur Andersen derived substantial consulting fees from Enron, in addition to its auditing fees. This created a significant conflict of interest, as the firm may have been reluctant to challenge Enron’s aggressive accounting practices for fear of jeopardizing its lucrative consulting business.

- Ignoring Red Flags: Numerous warnings and red flags regarding Enron’s accounting practices were reportedly raised within Arthur Andersen. However, these concerns were often downplayed or ignored by senior partners who were keen to maintain the relationship with their high-paying client.

- Document Shredding and Obstruction of Justice: In the aftermath of Enron’s collapse, Arthur Andersen was found to have shredded documents related to Enron’s audits, a clear act of obstruction of justice. This further solidified the perception that the firm had actively participated in the cover-up. The firm’s eventual demise, conviction, and dissolution marked a significant moment in the history of corporate auditing.

Financial Analysts: Blinded by Enthusiasm or Complicit Silence?

Financial analysts, whose job it is to provide independent research and recommendations to investors, largely remained bullish on Enron for an extended period. While some analysts did express skepticism, the majority maintained strong “buy” ratings, contributing to the inflated perception of Enron’s value.

- Reliance on Management’s Numbers: Analysts often relied heavily on the financial information provided by Enron’s management, which, as we now know, was highly manipulated. They lacked the full picture and were not privy to the intricate, off-balance-sheet dealings.

- “Wall Street’s” Pressure to be Positive: There was a general culture on Wall Street that favored positive coverage of large, prominent companies. Analysts who issued negative reports often found themselves ostracized, losing access to management and potentially impacting their firms’ investment banking relationships.

- Lack of Skepticism and Due Diligence: In hindsight, many of the accounting practices employed by Enron should have triggered greater skepticism and more rigorous due diligence from analysts. The complex nature of the financial instruments and the sheer speed of Enron’s reported growth should have raised more alarms.

The Unraveling: From Suspicion to Scandal and Bankruptcy

As the scale of Enron’s financial engineering became increasingly apparent, scrutiny intensified, leading to an inevitable and rapid downfall. The company’s carefully constructed facade began to crumble, revealing the rotten core beneath.

Whistleblowers and Investigative Journalism

The first significant cracks in Enron’s armor appeared with the brave actions of whistleblowers and the persistent efforts of investigative journalists. These individuals played a critical role in bringing the truth to light.

- Sherron Watkins’ Warning: Sherron Watkins, a vice president at Enron, famously wrote a memo to then-CEO Ken Lay in August 2001, expressing concerns about the company’s accounting practices and warning of potential bankruptcy. Her courage in highlighting these issues, though ultimately insufficient to save the company, became a key piece of the narrative.

- The Media’s Growing Skepticism: As journalists delved deeper, inconsistencies and questionable transactions came to light. Reports in publications like The Wall Street Journal began to question Enron’s financial reporting, slowly eroding investor confidence.

Restatements and the Collapse

The mounting pressure from the media, regulators, and a growing number of skeptical investors forced Enron to confront its accounting irregularities. The eventual outcome was a cascade of financial restatements that revealed the true extent of the company’s losses.

- Massive Financial Restatements: In late 2001, Enron announced it would restate its financial results for previous years, admitting to billions of dollars in accounting errors. This confession immediately shattered investor confidence.

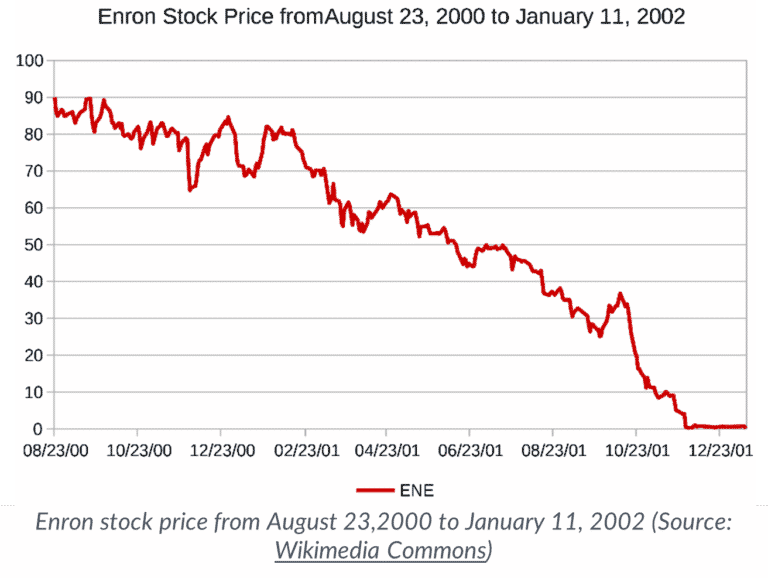

- Stock Price Plummet: The revelation of these accounting discrepancies sent Enron’s stock price into a freefall. What was once a darling of Wall Street became a pariah, trading at pennies on the dollar.

- Bankruptcy Filing: Facing an insurmountable debt burden and a complete loss of credibility, Enron filed for Chapter 11 bankruptcy protection on December 2, 2001. This marked the largest corporate bankruptcy in U.S. history at the time.

The Aftermath: Legal Ramifications and Lasting Impact

The Enron scandal had profound and far-reaching consequences, leading to significant legal actions and fundamentally altering the landscape of corporate governance and financial regulation.

- Criminal Prosecutions: Numerous Enron executives, including Kenneth Lay, Jeffrey Skilling, and Andrew Fastow, faced criminal charges for their roles in the fraud. While some convictions were overturned or reduced, the legal fallout was extensive, serving as a stark warning to corporate leaders.

- Sarbanes-Oxley Act of 2002: The Enron scandal, along with other corporate scandals of the era (e.g., WorldCom, Tyco), directly led to the passage of the Sarbanes-Oxley Act (SOX) in 2002. SOX significantly strengthened corporate governance rules, enhanced auditor independence, and increased accountability for corporate executives and boards of directors.

- Loss of Investor Confidence and Pension Devastation: The collapse of Enron resulted in the loss of billions of dollars for shareholders, many of whom were ordinary investors and pension funds. Employees saw their life savings, tied up in Enron stock and pensions, vanish overnight, a tragic human cost of corporate malfeasance.

Enron’s story remains a potent reminder of the dangers of unchecked ambition, the seductive allure of financial engineering, and the critical importance of ethical leadership and robust oversight. The lessons learned from Enron’s spectacular downfall continue to shape how we understand and regulate the world of business finance, emphasizing transparency, integrity, and accountability as the true cornerstones of sustainable corporate success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.