The Roth IRA is a powerful retirement savings tool, offering tax-free growth and tax-free withdrawals in retirement. However, its accessibility is tied to your income. Understanding the Roth IRA income limits is crucial for anyone looking to maximize their retirement savings and take advantage of this tax-advantaged account. This article will delve into the specifics of these income limits, explaining who qualifies, how they are calculated, and what strategies you can employ if your income currently falls outside the eligibility range.

Understanding the Mechanics of Roth IRA Income Limits

The income limits for contributing to a Roth IRA are set annually by the Internal Revenue Service (IRS). These limits are designed to ensure that the tax benefits of a Roth IRA are primarily available to individuals and families with moderate incomes, preventing higher earners from disproportionately benefiting from the tax-free withdrawal feature. It’s important to note that these limits can and do change each year due to inflation adjustments.

Modified Adjusted Gross Income (MAGI): The Key Metric

The IRS uses your Modified Adjusted Gross Income (MAGI) to determine your eligibility for a Roth IRA. MAGI is not simply your gross income; it’s a calculated figure derived from your Adjusted Gross Income (AGI) with certain deductions added back in. The most common additions back are:

- Deductions for student loan interest: If you’ve deducted interest paid on qualified student loans, this amount is added back.

- Deductions for tuition and fees: Any deduction claimed for educational expenses is added back.

- Deductions for IRA contributions: If you’ve contributed to a traditional IRA and deducted those contributions, that amount is added back.

- Deductions for foreign earned income and foreign housing exclusion: If you’ve excluded foreign income or housing costs, these amounts are added back.

- Deductions for U.S. savings bonds used for higher education: If you excluded interest from Series EE or Series I U.S. savings bonds used for qualified education expenses, this is added back.

- Deductions for alimony paid: For divorce or separation agreements executed before January 1, 2019, alimony payments made are added back. (Note: For agreements executed after this date, alimony is generally not deductible for the payer and not taxable for the recipient, so this addition back becomes less relevant).

Essentially, MAGI aims to capture a broader measure of your financial capacity to save for retirement. It’s crucial to accurately calculate your MAGI when determining your Roth IRA eligibility. You can find your AGI on your federal income tax return (Form 1040), and then you’ll need to make the necessary additions to arrive at your MAGI.

Filing Status Matters

The Roth IRA income limits are tiered based on your tax filing status. This means that married couples filing jointly have different income thresholds than single individuals, married individuals filing separately, or heads of household. This differentiation acknowledges the different financial responsibilities and tax burdens associated with each filing status.

- Single, Head of Household, or Married Filing Separately (and didn’t live with spouse at any time during the year): These filers generally have the most stringent income limits.

- Married Filing Jointly: This category typically has the highest income thresholds, allowing more couples to contribute directly to a Roth IRA.

- Married Filing Separately (and lived with spouse at any time during the year): This status often has the lowest income limits, reflecting a scenario where spousal income may be a factor even with separate filings.

It’s essential to use the correct filing status when checking the IRS-published income limits for the relevant tax year.

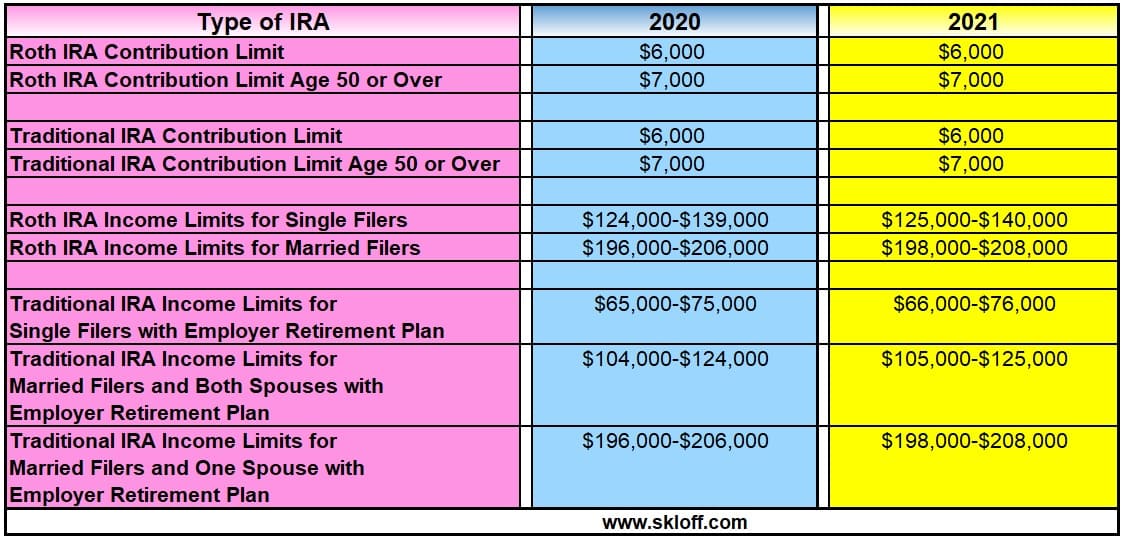

Current Roth IRA Income Limits and Contribution Phase-Outs

The IRS releases updated income limits for Roth IRAs annually. For the tax year 2023, the following MAGI thresholds apply:

For Single, Head of Household, or Married Filing Separately (who lived with spouse at any time during the year)

- Full Contribution: If your MAGI is less than $146,000, you can contribute the maximum allowable amount to a Roth IRA.

- Reduced Contribution (Phase-Out Range): If your MAGI is between $146,000 and $161,000, your ability to contribute is gradually reduced. For every dollar within this range, your maximum contribution is lowered.

- No Contribution Allowed: If your MAGI is $161,000 or more, you cannot contribute directly to a Roth IRA for the 2023 tax year.

For Married Filing Jointly

- Full Contribution: If your MAGI is less than $230,000, you can contribute the maximum allowable amount to a Roth IRA.

- Reduced Contribution (Phase-Out Range): If your MAGI is between $230,000 and $240,000, your contribution amount is gradually reduced.

- No Contribution Allowed: If your MAGI is $240,000 or more, you cannot contribute directly to a Roth IRA for the 2023 tax year.

For Married Filing Separately (and lived with spouse at any time during the year)

- Full Contribution: If your MAGI is less than $10,000, you can contribute the maximum allowable amount.

- Reduced Contribution (Phase-Out Range): If your MAGI is between $10,000 and $11,500, your contribution is gradually reduced.

- No Contribution Allowed: If your MAGI is $11,500 or more, you cannot contribute directly to a Roth IRA for the 2023 tax year.

It is crucial to consult the IRS website or a tax professional for the most up-to-date figures for the current tax year and any future years, as these numbers are subject to change.

The Annual Contribution Limit

In addition to the income limits, there’s an overall annual contribution limit for IRAs (both Roth and Traditional combined). For 2023, this limit is $6,500 for individuals under age 50 and $7,500 for individuals aged 50 and over (this includes a $1,000 catch-up contribution). If your income is within the phase-out range, your maximum allowable contribution will be prorated based on your MAGI within that range, down to a minimum of $200 if your MAGI falls within the phase-out, or zero if your MAGI is above the upper limit.

Navigating the Income Limits: Strategies for Higher Earners

For individuals and couples whose MAGI exceeds the Roth IRA income limits, there are still ways to benefit from Roth IRA advantages. These strategies often involve tax planning and understanding alternative contribution methods.

The “Backdoor” Roth IRA Conversion

The most popular strategy for high earners is the “backdoor” Roth IRA. This method involves making a non-deductible contribution to a Traditional IRA and then immediately converting that Traditional IRA into a Roth IRA.

The key to making this strategy work effectively is to ensure you have no pre-tax funds already in any Traditional IRAs, SEP IRAs, or SIMPLE IRAs. This is because the IRS’s “pro-rata rule” applies to conversions. If you have both pre-tax and after-tax (non-deductible) money in your IRAs, only a portion of your converted amount will be tax-free. The portion of the conversion that is taxable will be based on the ratio of your pre-tax IRA funds to your total IRA funds.

Steps for a Backdoor Roth IRA:

- Open a Traditional IRA: If you don’t already have one, open a Traditional IRA.

- Make a Non-Deductible Contribution: Contribute the maximum allowable amount (up to the annual limit) to this Traditional IRA. Do not deduct this contribution on your taxes.

- Convert to Roth IRA: As soon as possible after the contribution settles, convert the funds from your Traditional IRA to a Roth IRA. Since the contribution was made with after-tax dollars and you have no pre-tax IRA balances, the conversion should be largely tax-free (or entirely tax-free if you have no pre-tax IRA balances).

It is advisable to consult with a tax professional before executing a backdoor Roth IRA to ensure you understand the pro-rata rule and to avoid any potential tax pitfalls, especially if you have existing pre-tax IRA balances.

Contribute to a Spousal Roth IRA

If you are married and your spouse earns less than you or not at all, and your combined MAGI is within the limits for married couples filing jointly, you may be able to contribute to a spousal Roth IRA. This allows one spouse to contribute to a Roth IRA on behalf of the other spouse, provided the couple files a joint return and the contributing spouse has earned income at least equal to the amount contributed. This can be a valuable strategy even if one spouse is a high earner, as long as the couple’s overall MAGI remains within the joint filing limits.

Explore Other Retirement Savings Vehicles

While a Roth IRA offers unique tax benefits, it’s not the only way to save for retirement. High earners with significant income may find other retirement savings vehicles more appropriate or accessible:

- 401(k)s and Other Employer-Sponsored Plans: If your employer offers a 401(k), 403(b), or similar plan, these often have much higher contribution limits than IRAs. Many of these plans also offer Roth contribution options, allowing for tax-free growth and withdrawals, albeit with different income considerations that are employer-specific rather than IRS-wide for eligibility.

- Traditional IRAs (for High Earners with Deductibility Limitations): If your MAGI is too high to contribute directly to a Roth IRA and you don’t want to do a backdoor Roth, you can still contribute to a Traditional IRA. However, your ability to deduct those contributions may be limited or eliminated if you (or your spouse, if married filing jointly) are covered by a retirement plan at work. Even if non-deductible, it can still offer tax-deferred growth, with taxes paid upon withdrawal in retirement.

- Health Savings Accounts (HSAs): If you have a high-deductible health plan, an HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Unused funds can be invested and used for retirement expenses after age 65, effectively acting as a Roth IRA for those expenses.

The Importance of Staying Informed

The Roth IRA income limits are a dynamic aspect of personal finance. They are subject to annual adjustments and can be influenced by changes in tax law. Therefore, it is paramount to:

Regularly Review Your Income and MAGI

As your income fluctuates and tax laws evolve, your eligibility for a Roth IRA can change. Make it a habit to review your Modified Adjusted Gross Income (MAGI) annually, ideally when preparing your taxes, to understand your current standing. This proactive approach will help you make informed decisions about your retirement savings strategy.

Consult IRS Publications and Tax Professionals

The IRS provides official publications detailing contribution limits and income thresholds for IRAs. These are the most authoritative sources of information. However, for personalized advice and to navigate complex tax situations, consulting with a qualified tax advisor or financial planner is highly recommended. They can help you accurately calculate your MAGI, understand the implications of different strategies, and ensure you are compliant with all tax regulations.

Plan for Future Changes

Tax legislation can change, and it’s possible that Roth IRA income limits or rules could be altered in the future. Staying informed about potential legislative changes can help you adapt your financial planning accordingly. For example, discussions about tax reform often include potential changes to retirement savings vehicles.

Understanding and adhering to the Roth IRA income limits is a fundamental step in optimizing your retirement savings strategy. Whether you qualify for direct contributions or need to explore alternative routes like the backdoor Roth IRA, knowledge is your most valuable asset in building a secure financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.