Navigating the world of personal finance can often feel like an intricate maze. Amidst the myriad of investment options and retirement planning strategies, one vehicle stands out for its widespread availability and significant advantages: the 401(k) plan. A cornerstone of employer-sponsored retirement savings in the United States, the 401(k) offers a powerful pathway to building long-term wealth and securing a comfortable future. Understanding its multifaceted benefits is crucial for anyone looking to optimize their financial well-being. This article delves into the core advantages of participating in a 401(k) plan, illuminating why it remains a pivotal tool for retirement preparedness.

The Power of Tax Advantages

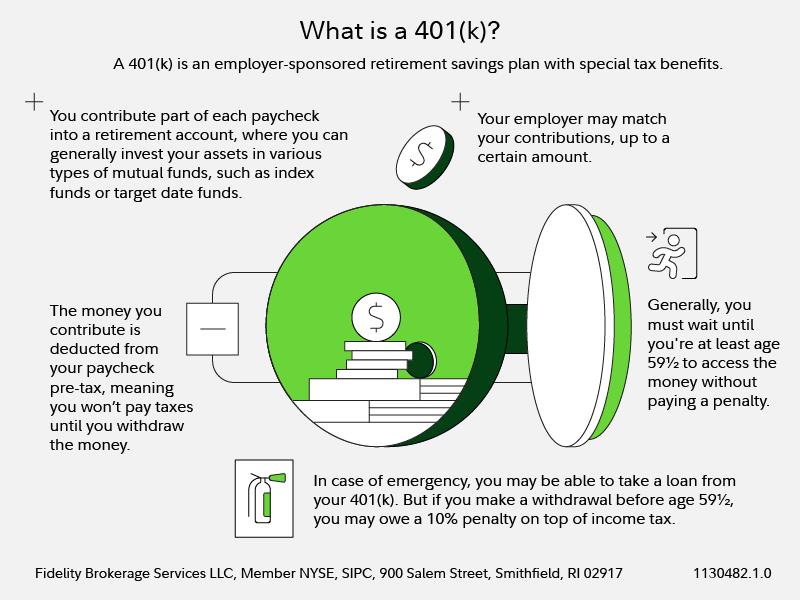

One of the most compelling reasons to embrace a 401(k) is its inherent tax advantages. These benefits are designed to encourage long-term saving by reducing your current tax burden and allowing your investments to grow tax-deferred. This dual advantage significantly accelerates wealth accumulation compared to taxable investment accounts.

Tax-Deferred Growth

The primary tax benefit of a traditional 401(k) is tax-deferred growth. This means that any earnings your investments generate – be it through dividends, interest, or capital appreciation – are not taxed in the year they are realized. Instead, taxation is postponed until you withdraw the funds in retirement. This is a monumental advantage because it allows your entire investment balance to continue compounding year after year, unimpeded by annual tax liabilities. Imagine an investment that earns 8% annually. If you were to pay taxes on those earnings each year, a significant portion would be siphoned off, slowing down your growth trajectory. With tax-deferred growth, that full 8% remains invested, working to build a larger nest egg. Over decades, this difference can amount to tens or even hundreds of thousands of dollars more in your retirement account.

Pre-Tax Contributions

Contributions made to a traditional 401(k) are typically made on a pre-tax basis. This means the money you contribute is deducted from your gross income before federal and state income taxes are calculated. The immediate effect of this is a reduction in your current taxable income. For individuals in higher tax brackets, this can translate into a substantial immediate tax saving. For example, if you earn $70,000 a year and contribute $10,000 to your 401(k), your taxable income for that year is reduced to $60,000. This can lead to a noticeably smaller tax bill, freeing up more cash flow in your current budget, or allowing you to reinvest those tax savings elsewhere. This immediate financial relief makes saving for retirement more palatable, especially when faced with competing financial demands.

Roth 401(k) Option: Tax-Free Withdrawals in Retirement

While traditional 401(k)s offer tax-deferred growth, many employers now also offer a Roth 401(k) option. The mechanics are slightly different, but the underlying principle of tax advantage remains. With a Roth 401(k), contributions are made with after-tax dollars. This means you don’t receive an immediate tax deduction on your contributions. However, the true magic of the Roth 401(k) lies in its withdrawal treatment. Qualified withdrawals in retirement are entirely tax-free. This includes both your contributions and all the earnings generated over the years. This can be a game-changer for individuals who anticipate being in a higher tax bracket in retirement than they are currently, or for those who simply prefer the certainty of knowing their retirement income will be free from future tax obligations. The decision between a traditional and Roth 401(k) often hinges on an individual’s current income, expected future income, and tax expectations.

The Power of Employer Matching Contributions

Beyond the personal tax advantages, one of the most significant and often overlooked benefits of a 401(k) is the potential for employer matching contributions. This is essentially free money, an immediate boost to your retirement savings that can dramatically accelerate your wealth-building journey.

“Free Money” for Your Retirement

An employer match works by the employer contributing a certain amount to your 401(k) based on your own contributions. Common matching formulas include percentages of your salary, such as “50% match up to 6% of your salary.” This means if you contribute 6% of your income, your employer will add an additional 3% to your account. It’s critical to understand your employer’s specific matching formula. Failing to contribute enough to capture the full employer match is akin to leaving free money on the table, a financial misstep that can cost you dearly in the long run. Over a career, these matched contributions can amount to tens of thousands of dollars, significantly increasing your retirement nest egg without any additional personal sacrifice beyond what you’re already contributing.

Boosting Your Savings Rate

The presence of an employer match inherently encourages higher contribution rates from employees. Knowing that your contributions will be amplified by your employer’s generosity can be a powerful motivator to save more aggressively. Many individuals who might otherwise contribute a modest amount to a retirement plan are incentivized to maximize their contributions to take full advantage of the match. This increased savings rate, combined with the matching funds, creates a virtuous cycle of accelerated wealth accumulation. It transforms a good savings plan into a great one, ensuring that more of your income is consistently directed towards your future financial security.

Compounding Effect Amplified

When employer contributions are added to your own, the total amount invested in your 401(k) is larger from the outset. This larger principal, when subjected to the power of compounding, grows at an even faster rate. The employer’s match effectively acts as an immediate injection of capital, giving your investments a head start. This amplified compounding effect, fueled by both your contributions and your employer’s generosity, is a key reason why 401(k)s are so effective for long-term retirement planning.

Convenience, Simplicity, and Additional Benefits

Beyond tax advantages and employer matches, 401(k) plans offer a suite of practical benefits that make them an accessible and attractive option for a broad range of employees.

Automatic Deductions and Payroll Integration

One of the most significant conveniences of a 401(k) is the automatic deduction of contributions directly from your paycheck. This “set it and forget it” approach simplifies the saving process, removing the need for manual transfers or remembering to contribute each pay period. By the time the money hits your bank account, it has already been allocated to your retirement savings. This seamless integration into your payroll system ensures consistent saving without requiring constant attention, which is particularly beneficial for individuals who may struggle with discipline or forgetfulness when it comes to managing their finances.

Investment Options and Professional Management

While the specific investment choices within a 401(k) plan vary by employer, most plans offer a curated selection of investment options, often including mutual funds and target-date funds. These funds are managed by professional investment managers who make decisions about asset allocation and security selection. For many individuals, this means they can participate in diversified investment portfolios without needing to become expert investors themselves. Target-date funds, in particular, are designed to automatically adjust their asset allocation over time, becoming more conservative as you approach your target retirement date, providing a hands-off approach to managing your investment risk.

Portability and Rollover Options

Should you change employers, your 401(k) plan doesn’t disappear. Most 401(k) plans are portable, meaning you can take your vested balance with you. You typically have several options: leave the money with your former employer’s plan (if permitted), roll it over into your new employer’s 401(k) plan, or roll it over into an Individual Retirement Arrangement (IRA). This portability ensures that your accumulated savings remain secure and continue to grow, regardless of your employment status. The ability to consolidate retirement accounts through rollovers can also simplify your financial management in the long run.

Loan Provisions

Many 401(k) plans allow participants to take out loans against their vested balance. While this should generally be considered a last resort due to potential fees and the risk of depleting your retirement savings if you are unable to repay, it can offer a financial lifeline in times of genuine emergency, such as for a down payment on a home or to cover unforeseen medical expenses. It’s crucial to understand the terms and conditions of any 401(k) loan, as borrowing from your retirement savings can have long-term implications.

Protection Under ERISA

401(k) plans are governed by the Employee Retirement Income Security Act of 1974 (ERISA). ERISA provides a framework of protections for participants, including fiduciary responsibilities for plan administrators, disclosure requirements, and rules against self-dealing. This legal framework offers a degree of security and transparency for your retirement savings, ensuring that your plan is managed in your best interest.

In conclusion, the benefits of participating in a 401(k) plan are substantial and far-reaching. From the immediate gratification of tax savings and the potent allure of employer matching contributions to the long-term advantages of tax-deferred growth and the sheer convenience of automatic saving, the 401(k) stands as an indispensable tool for achieving financial independence in retirement. By understanding and leveraging these benefits, individuals can confidently build a secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.