Social Security plays a crucial role in the financial security of millions of Americans, particularly during retirement. While many are familiar with individual retirement benefits, a significant aspect of the Social Security system often overlooked is the provision for spousal benefits. These benefits are designed to provide a safety net for individuals who may not have earned significant Social Security credits in their own right, or whose own earning record would result in a lower retirement benefit than their spouse’s. Understanding spousal benefits is vital for married couples and divorced individuals to maximize their Social Security income and ensure a more secure financial future. This comprehensive guide will delve into the intricacies of Social Security spousal benefits, exploring who is eligible, how benefits are calculated, and the strategic considerations involved.

Understanding the Foundation: Eligibility for Spousal Benefits

At its core, Social Security spousal benefits are intended to recognize the contributions of both spouses to a marriage, even if one spouse has a lower or no earning history. This ensures that a household’s collective earning power is reflected in their Social Security income. To qualify for spousal benefits, several key criteria must be met.

Marriage Requirements

The most fundamental requirement for receiving spousal benefits is a valid marriage. The Social Security Administration (SSA) recognizes legal marriages. This means that at the time you apply for benefits, you must be legally married. For individuals who are divorced, there are specific rules that can still allow them to claim benefits based on an ex-spouse’s record, which we will discuss later. The duration of the marriage also plays a role. Generally, a marriage must have lasted for at least one continuous year for a spouse to be eligible for benefits based on their living spouse’s record. This one-year rule is waived in cases where the applying spouse is caring for the worker’s child who is under age 16 or disabled.

Worker’s Eligibility and Benefit Status

The spouse claiming benefits is not the only one who needs to meet criteria. The worker on whose record the spousal benefit is claimed must also be eligible for Social Security retirement or disability benefits. This means the worker must have earned enough work credits (typically 40 credits, equivalent to about 10 years of work) to qualify for their own benefit. Furthermore, the worker must have already filed for their own Social Security benefits. You cannot claim spousal benefits if the worker is still actively employed and not yet receiving their own Social Security income, unless they are at least age 62 and have filed for benefits.

Age Requirements for Claimants

The age at which you claim spousal benefits significantly impacts the amount you receive.

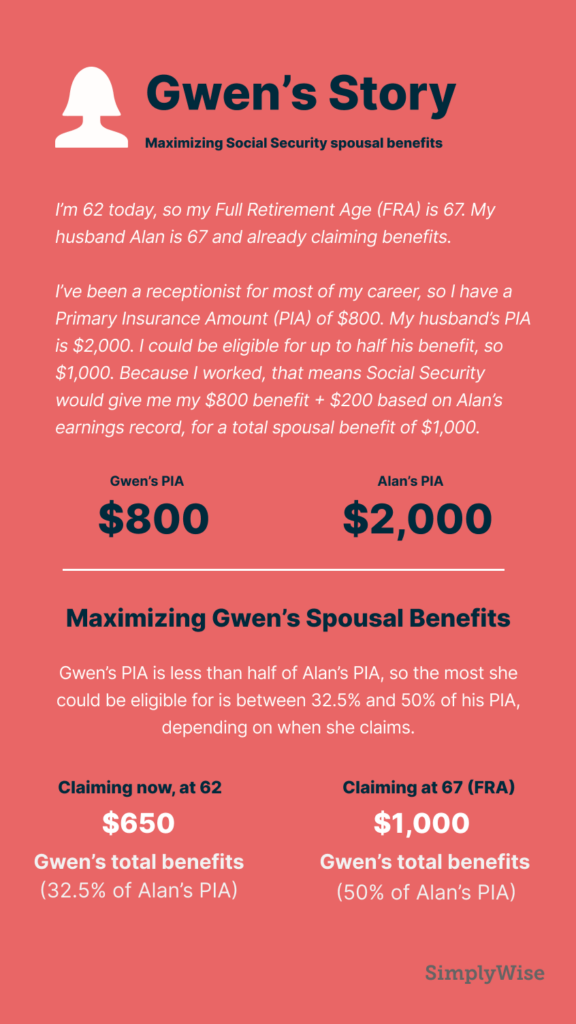

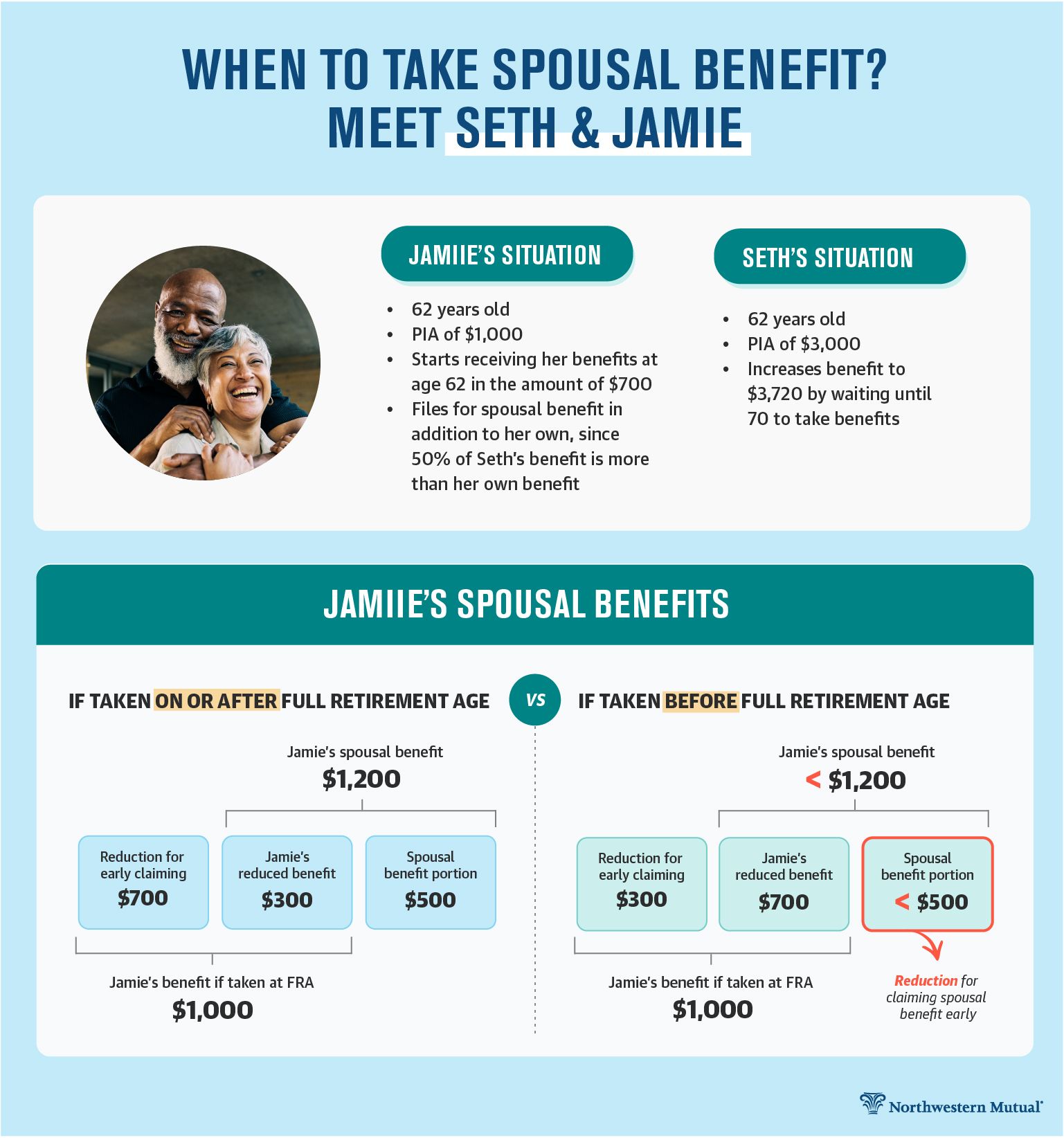

- Full Retirement Age (FRA): If you claim spousal benefits at your own Full Retirement Age, you will receive 50% of your spouse’s primary insurance amount (PIA). The PIA is the amount a worker is entitled to at their FRA.

- Before Full Retirement Age: You can claim spousal benefits as early as age 62. However, if you claim before your FRA, your benefit will be permanently reduced. The reduction is approximately 25/36 of 1% for each month before FRA, up to 36 months, and then about 5/12 of 1% for each additional month. This reduction can be substantial, so careful consideration is needed. For example, claiming at age 62, assuming an FRA of 67, would result in a benefit that is about 70% of the full spousal amount.

- After Full Retirement Age: Claiming spousal benefits after your FRA does not increase the benefit amount beyond the 50% of your spouse’s PIA. Once you reach your FRA, the benefit is set at that level.

Caregiver Exception

As mentioned earlier, the one-year marriage rule is waived if the individual applying for spousal benefits is caring for a child who is the worker’s biological or adopted child, and that child is under age 16 or has a disability and is receiving benefits on the worker’s record. In this scenario, the caregiver spouse can receive benefits regardless of the marriage duration.

Calculating Spousal Benefits: How Your Benefit Amount is Determined

The calculation of spousal benefits is based on the worker’s primary insurance amount (PIA) and the age at which the claimant begins receiving benefits. It’s a system designed to offer support, but the specifics can be complex.

The Primary Insurance Amount (PIA)

The foundation of any Social Security benefit, including spousal benefits, is the worker’s Primary Insurance Amount (PIA). The PIA is calculated by the Social Security Administration based on a worker’s 35 highest years of earnings, adjusted for inflation. This amount represents the benefit the worker would receive if they claimed at their Full Retirement Age (FRA). For spousal benefits, the claimant’s benefit is a percentage of the worker’s PIA.

The 50% Rule for Spouses

When a spouse claims benefits based on their partner’s record, they are generally entitled to up to 50% of the worker’s PIA. This is the maximum they can receive, and it applies if the claimant waits until their own Full Retirement Age (FRA) to claim. This 50% figure is crucial because it often provides a significant financial boost to couples where one spouse has a lower earning history.

Impact of Early Claiming on Spousal Benefits

If a spouse claims spousal benefits before their FRA, their benefit is permanently reduced. The reduction is calculated based on how many months before their FRA they start receiving benefits. For each month prior to FRA, the benefit is reduced by a fraction of the full spousal amount. For example, if your FRA is 67 and you start receiving spousal benefits at age 62 (5 years or 60 months early), your benefit will be reduced by approximately 30% (5 years * 12 months/year * 0.417% per month). This means you would receive roughly 35% of your spouse’s PIA instead of 50%. It’s vital to understand this reduction, as it affects the ongoing monthly income for the remainder of your life.

The “Deductible Amount” and the Rule of “Less Than 100%”

A crucial concept in spousal benefit calculation is the “deductible amount.” If an individual is eligible for both their own retirement benefit and a spousal benefit, the Social Security Administration will pay them the higher of the two. However, if their own retirement benefit is less than the full spousal benefit they would otherwise receive (i.e., less than 50% of their spouse’s PIA), the spousal benefit will be adjusted. The spousal benefit will be the worker’s PIA minus the amount of the claimant’s own retirement benefit. The result is that the claimant receives their own benefit plus an additional amount, bringing their total benefit up to the spousal amount. This is often referred to as the “benefit equal to less than 100%.” Effectively, the spousal benefit supplements their own lower benefit so that they receive the full spousal entitlement. This ensures that the spouse with the lower earnings history still receives the intended portion of the couple’s combined Social Security potential.

Divorced Spouses’ Benefits

The rules for spousal benefits extend to divorced individuals. If you were married for at least 10 years, and are currently unmarried, you may be eligible to receive spousal benefits based on your ex-spouse’s work record, even if they have not yet retired or remarried. The eligibility requirements are similar:

- You must be at least age 62.

- Your ex-spouse must be entitled to Social Security retirement or disability benefits.

- Your own retirement benefit must be less than the spousal benefit you would receive.

- The marriage must have lasted at least 10 years.

If your ex-spouse has remarried, you can still claim benefits on their record, provided your divorce was final before they remarried. If your ex-spouse is deceased, you may be eligible for survivor benefits, which are typically higher than spousal benefits.

Strategies for Maximizing Spousal Benefits

Understanding how spousal benefits work is the first step; the next is to strategically utilize them to your financial advantage. This often involves coordinating benefit claiming strategies with your spouse.

Coordinating Claiming Ages

One of the most impactful strategies for married couples is to coordinate when each spouse files for benefits. The decision of who claims first, and when, can significantly affect the total lifetime benefits received by the couple.

- Delaying for Higher Benefits: If one spouse has a significantly higher earning record, it often makes sense for them to delay claiming their benefits as long as possible, up to age 70. This maximizes their own PIA. By delaying, they also increase the potential spousal benefit available to their partner.

- The “File and Suspend” Strategy (No Longer Available for New Filers): It’s important to note that the “file and suspend” strategy, which allowed a spouse to claim benefits based on their partner’s record while their own benefit continued to grow, is no longer available for new applicants since legislative changes in 2015. However, individuals who initiated this strategy before November 2015 can continue to benefit from it.

- Spousal Benefit First Strategy: For couples where one spouse has a very low or no earning history, a common strategy is for that spouse to claim their spousal benefit at age 62 (or later, if they can afford to wait) while the higher-earning spouse continues to delay their own benefits until FRA or age 70. This provides immediate income to the lower-earning spouse. Once the higher-earning spouse claims their larger benefit, the lower-earning spouse can then switch to their own, potentially higher, retirement benefit if it is greater than the spousal benefit they were receiving.

Understanding the Impact on Survivor Benefits

Spousal benefits are intrinsically linked to survivor benefits. When one spouse passes away, the surviving spouse may be eligible to receive survivor benefits. The survivor benefit is typically 100% of the deceased worker’s benefit amount (PIA).

- Benefit Transition: If the surviving spouse was already receiving spousal benefits, their benefit will automatically convert to the survivor benefit upon the death of their spouse.

- Maximizing Survivor Benefits: The amount of the survivor benefit is based on the deceased worker’s benefit. Therefore, if the worker delayed claiming their benefits until age 70, the survivor benefit will be significantly higher than if they had claimed at an earlier age. This underscores the importance of the higher-earning spouse maximizing their own benefit, as it directly benefits the surviving spouse.

- Electing at FRA: A surviving spouse can elect to receive survivor benefits at their FRA. If they elect before FRA, their benefit will be permanently reduced. They can also delay claiming survivor benefits past FRA to increase the amount, but the benefit is capped at 100% of the deceased’s PIA.

When to Seek Professional Advice

Navigating Social Security benefits can be complex, especially for couples with differing earning histories or those facing divorce. The nuances of calculation, the impact of early claiming, and the interaction with other income sources can be confusing.

- Consulting a Financial Advisor: A qualified financial advisor specializing in retirement planning can help couples analyze their specific situation, project future benefits, and develop a personalized claiming strategy. They can model different scenarios and explain the long-term implications of various choices.

- Utilizing Social Security Resources: The Social Security Administration’s website (ssa.gov) provides a wealth of information, including benefit calculators and detailed explanations of their programs. Creating a “my Social Security” account allows individuals to view their earnings record and estimated future benefits.

- Understanding Your Personal Situation: Ultimately, the best strategy depends on individual circumstances, including health, life expectancy, other retirement income sources, and financial needs. A thorough understanding of these factors, combined with knowledge of the Social Security system, is key to making informed decisions.

Spousal Benefits and Other Income Sources: A Holistic Financial View

While spousal benefits are a crucial component of retirement income, they are rarely the sole source of financial support. Understanding how spousal benefits interact with other retirement assets is essential for comprehensive financial planning.

Integration with Personal Retirement Benefits

As previously mentioned, if you are eligible for both your own Social Security retirement benefit and a spousal benefit, Social Security will pay you the higher of the two amounts. This is a protective mechanism to ensure you receive the most advantageous benefit. For instance, if your own PIA is $1,000 and the spousal benefit you are eligible for is $1,500, you will receive $1,500. However, if your own PIA is $1,200 and the spousal benefit is $1,500, your spousal benefit will be reduced by $300 ($1,500 – $1,200 = $300), so you receive your own $1,200 benefit plus an additional $300, for a total of $1,500. This prevents individuals from receiving more than the intended spousal benefit amount while still ensuring they are not penalized for having their own lower earnings history.

Impact of Pensions and Other Earnings

- Government Pensions (Windfall Elimination Provision – WEP): If you receive a pension from work that was not covered by Social Security (such as some state or local government jobs), your Social Security benefit, including any spousal benefit you might receive, could be reduced. The Windfall Elimination Provision (WEP) adjusts the formula used to calculate your Social Security benefit. This provision is designed to prevent individuals from receiving a disproportionately large Social Security benefit due to a combination of a non-covered pension and a short Social Security-covered work history.

- Garnishment and Deductions: Certain debts or legal obligations can lead to deductions from Social Security benefits, including spousal benefits. This can include child support, alimony, and federal income tax levies. It’s important to be aware of potential deductions that might affect your net benefit.

- Work After Claiming Benefits: If you claim spousal benefits before your FRA while still working, your benefits may be subject to an earnings test. For 2024, if you are under FRA, $1 in benefits will be withheld for every $2 you earn above a certain limit ($22,320 for 2024). Once you reach FRA, this earnings limit is lifted, and your benefits will no longer be reduced due to your earnings, although the benefit amount itself will not increase beyond what you were eligible for at FRA or beyond.

Planning for a Secure Retirement

Social Security spousal benefits are a powerful tool, but they are most effective when integrated into a broader retirement plan.

- Diversification of Income: Relying solely on Social Security can be risky. A diversified retirement income strategy that includes savings, investments (like 401(k)s or IRAs), pensions, and other assets provides a more robust financial foundation.

- Long-Term Financial Goals: Consider your long-term financial goals, including healthcare expenses, potential long-term care needs, and desired lifestyle in retirement. This will help you determine how much income you will need and how spousal benefits can contribute to meeting those needs.

- Regular Review: It’s advisable to review your retirement plan and Social Security strategy periodically, especially as life circumstances change (e.g., changes in marital status, health, or employment).

In conclusion, spousal benefits are an integral part of the Social Security system, offering financial support to spouses and ex-spouses who may not have earned sufficient credits on their own or whose individual benefits would be significantly lower. By understanding the eligibility requirements, calculation methods, and strategic claiming options, couples can make informed decisions to maximize their collective Social Security income, paving the way for a more secure and comfortable retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.