The world of investing can seem daunting, a labyrinth of jargon and complex instruments. For many, the idea of putting their hard-earned money to work in the financial markets evokes images of high-stakes trading floors and exclusive clubs. However, the reality for most investors is far more accessible, and at the heart of this accessibility lies a powerful tool: the mutual fund. If you’ve ever wondered what a mutual fund is and how it can fit into your financial journey, you’ve come to the right place. This article aims to demystify mutual funds, breaking down their fundamental principles, exploring their advantages and disadvantages, and guiding you on how to make informed decisions about their role in your investment portfolio.

Understanding the Core Concept of Mutual Funds

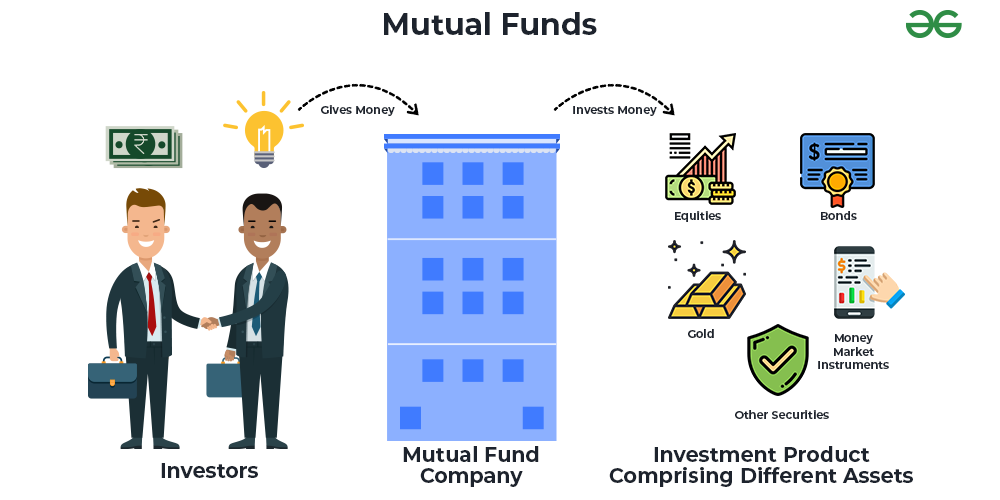

At its most basic, a mutual fund is an investment vehicle that pools money from many investors to purchase a diversified portfolio of securities, such as stocks, bonds, or other assets. Think of it as a collective investment where a group of people contribute their money, and a professional fund manager uses this combined pool to buy a variety of investments on behalf of all the investors. Each investor owns a portion of the fund, proportional to their investment. The value of your investment in a mutual fund fluctuates with the market value of the underlying securities.

How Mutual Funds Work: Pooling Resources for Diversification

The magic of a mutual fund lies in its ability to achieve diversification, a cornerstone of sound investment strategy. Diversification means spreading your investments across different asset classes, industries, and geographic regions. This reduces the risk associated with any single investment performing poorly. For an individual investor, buying a diversified portfolio of stocks or bonds can be prohibitively expensive and require significant expertise. A mutual fund, however, allows even small investors to gain instant diversification by owning a piece of a much larger, professionally managed portfolio.

When you invest in a mutual fund, you are essentially buying “shares” or “units” of the fund. The price of these shares is known as the Net Asset Value (NAV), which is calculated daily by dividing the total value of the fund’s assets (minus liabilities) by the number of outstanding shares. The NAV reflects the current market value of all the securities held within the fund. As the value of these underlying securities rises or falls, so does the NAV of the mutual fund, and consequently, the value of your investment.

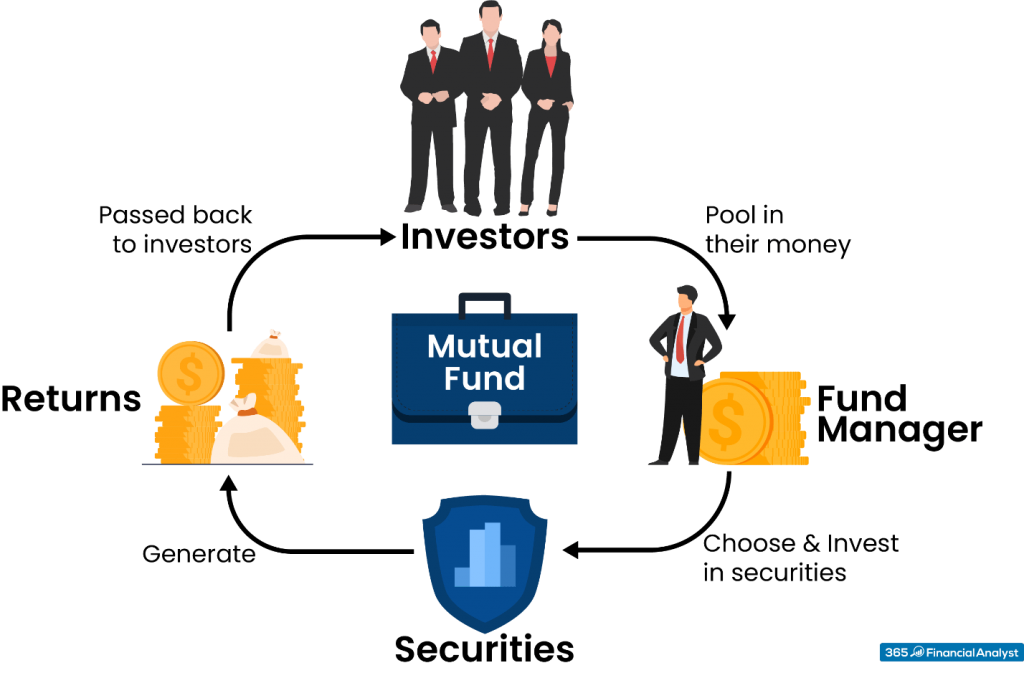

The Role of the Fund Manager: Expertise at Your Service

A crucial element of a mutual fund is the professional fund manager. These are individuals or teams with extensive knowledge and experience in financial markets. Their primary responsibility is to make investment decisions on behalf of the fund’s investors. This includes selecting which securities to buy and sell, determining the optimal allocation of assets, and monitoring the portfolio’s performance. For individual investors who may lack the time, knowledge, or desire to manage their own investments actively, a fund manager offers a valuable service. They conduct research, analyze market trends, and aim to achieve the fund’s stated investment objectives, whether it’s capital appreciation, income generation, or a combination of both.

Types of Mutual Funds: Tailoring Investments to Your Goals

The world of mutual funds is not monolithic. They come in various structures and cater to a wide spectrum of investment goals and risk appetites. Understanding these different types is crucial for selecting a fund that aligns with your personal financial objectives.

Equity Funds: Investing in Stocks for Growth

Equity funds, also known as stock funds, primarily invest in the shares of publicly traded companies. The primary objective of equity funds is capital appreciation, meaning they aim to grow the value of your investment over time by selecting stocks that are expected to increase in price. These funds can be further categorized based on the size of the companies they invest in (large-cap, mid-cap, small-cap), the investment style (growth, value), or the sector they focus on (technology, healthcare, financials). Equity funds generally carry a higher risk than bond funds but also offer the potential for higher returns over the long term. They are often favored by investors with a longer time horizon and a higher tolerance for risk.

Debt Funds: Seeking Stability and Income

Debt funds, or bond funds, invest in fixed-income securities, such as government bonds, corporate bonds, and municipal bonds. The primary objective of debt funds is usually to provide a steady stream of income and preserve capital, making them generally less risky than equity funds. The returns from debt funds come from the interest payments made by the bond issuers and any appreciation in the bond’s price. Similar to equity funds, debt funds can be categorized by the maturity of the bonds they hold (short-term, long-term), the credit quality of the issuers (government, high-yield), or the type of issuer. These funds are often suitable for investors who prioritize capital preservation and regular income over aggressive growth, or for those who have a shorter investment horizon.

Hybrid Funds: The Best of Both Worlds

Hybrid funds, also known as balanced funds, invest in a mix of equities and debt instruments. This blend aims to offer investors a balance between growth potential and risk mitigation. The allocation between stocks and bonds can vary significantly, leading to different types of hybrid funds. For instance, an aggressive hybrid fund might have a higher allocation to equities, while a conservative hybrid fund will lean more towards debt. The specific asset allocation is typically determined by the fund’s investment objective. Hybrid funds can be a good option for investors who want diversification and are looking for a less volatile investment than pure equity funds but with more growth potential than pure debt funds.

Advantages of Investing in Mutual Funds

Mutual funds have become a popular investment vehicle for a reason. They offer a compelling set of benefits that cater to a wide range of investors, from beginners to seasoned professionals.

Diversification Made Easy and Affordable

As previously mentioned, one of the most significant advantages of mutual funds is their ability to provide instant diversification. For a relatively small investment, you gain exposure to a broad range of securities, significantly reducing the risk associated with investing in just a few individual stocks or bonds. This is particularly beneficial for retail investors who might not have the capital or expertise to build a diversified portfolio on their own. By spreading risk across numerous holdings, the impact of any single security’s poor performance is minimized.

Professional Management and Expertise

Mutual funds are managed by experienced professionals who dedicate their time and resources to researching, analyzing, and selecting investments. This professional oversight can be invaluable, especially for individuals who lack the time, knowledge, or inclination to manage their own investments. Fund managers are equipped to navigate the complexities of the financial markets, make strategic decisions, and strive to achieve the fund’s objectives. This frees up investors to focus on other aspects of their lives while still benefiting from professional investment management.

Liquidity and Accessibility

Mutual funds are generally considered highly liquid investments. This means you can typically buy or sell your shares easily on any business day at the fund’s current NAV. This accessibility allows investors to adjust their portfolios as their financial circumstances or market conditions change. Unlike certain other investments that can be difficult to sell quickly without significant price concessions, mutual fund shares can be redeemed with relative ease, providing investors with flexibility.

Considerations and Potential Drawbacks of Mutual Funds

While mutual funds offer numerous advantages, it’s essential to be aware of their potential drawbacks to make a well-rounded investment decision.

Fees and Expenses: The Cost of Management

A significant consideration when investing in mutual funds is the presence of fees and expenses. These costs are charged by the fund to cover management fees, administrative costs, marketing expenses, and other operational overheads. The most common fee is the expense ratio, which is an annual percentage of the fund’s assets that is deducted to cover these costs. A higher expense ratio can eat into your investment returns over time, especially if the fund’s performance is only mediocre. It’s crucial to compare expense ratios across different funds with similar investment objectives. Other fees might include sales charges (loads) when buying or selling fund shares, though many “no-load” funds are available.

Performance Not Guaranteed: Market Risks Persist

Despite the presence of professional management, mutual fund performance is not guaranteed. The value of your investment is subject to market fluctuations, and the fund’s underlying assets can lose value. While diversification helps mitigate risk, it cannot eliminate it entirely. There will be periods when the market declines, and consequently, the NAV of your mutual fund will also decrease. Investors must understand that mutual funds carry inherent market risks, and past performance is not indicative of future results.

Tax Implications: Understanding the Burden

Mutual funds can generate taxable events for investors even if they don’t sell their shares. When a fund manager sells securities within the portfolio that result in a capital gain, these gains are often distributed to the fund’s shareholders, who then become liable for taxes on those distributions, regardless of whether they received the cash or reinvested it. This can lead to unexpected tax bills, particularly in taxable accounts. Understanding the tax efficiency of different mutual fund types and strategies is crucial for tax planning. For example, index funds, which passively track an index, often have lower portfolio turnover and therefore generate fewer taxable capital gains distributions than actively managed funds.

Choosing the Right Mutual Fund for Your Investment Needs

Selecting the most suitable mutual fund requires careful consideration of your personal financial situation, investment goals, and risk tolerance. It’s not a one-size-fits-all decision.

Defining Your Investment Goals and Time Horizon

Before diving into specific funds, ask yourself: what are you trying to achieve with this investment? Are you saving for retirement in 30 years, a down payment on a house in five years, or simply looking to grow your wealth over the next decade? Your investment goals will significantly influence the type of mutual fund that is appropriate. For long-term goals like retirement, equity funds might be suitable due to their growth potential. For shorter-term goals, where capital preservation is paramount, debt funds or conservative hybrid funds might be a better choice. Your time horizon – the length of time you plan to invest – is intrinsically linked to your goals and dictates your ability to weather market volatility.

Assessing Your Risk Tolerance

Risk tolerance refers to your ability and willingness to withstand potential losses in pursuit of higher returns. If you are comfortable with a higher degree of volatility and potential for loss in exchange for the possibility of greater gains, you might lean towards equity-heavy funds. Conversely, if you prioritize stability and are uncomfortable with significant fluctuations in your investment value, you should consider debt funds or more conservative hybrid options. Many online questionnaires and financial advisors can help you assess your risk tolerance.

Researching Fund Performance, Fees, and Management

Once you have a clear understanding of your goals and risk tolerance, you can begin researching specific mutual funds. Look beyond just the headline returns. Examine the fund’s historical performance over various market cycles, but remember that past performance is not a guarantee of future results. Crucially, pay close attention to the fund’s expense ratio and any other fees. A fund that consistently underperforms its benchmark and charges high fees is unlikely to be a good long-term investment. Investigate the fund manager’s experience and the fund’s investment strategy. Reputable sources for fund research include financial websites, fund prospectuses, and independent financial advisors.

By understanding the fundamentals of mutual funds, their various types, their pros and cons, and by diligently researching your options, you can leverage this powerful investment vehicle to help you achieve your financial aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.