In the contemporary financial landscape, the boundary between traditional banking and digital liquidity has become increasingly blurred. Among the vanguard of this shift is Cash App, a peer-to-peer (P2P) payment service that has evolved from a simple transfer tool into a multi-faceted financial ecosystem. For individuals looking to optimize their personal finances, understanding how to “get money” from Cash App—whether through standard withdrawals, rewards, or investment returns—is essential. This guide explores the strategic use of Cash App as a financial tool, focusing on maximizing efficiency and security.

1. Navigating the Mechanics of Funds Extraction

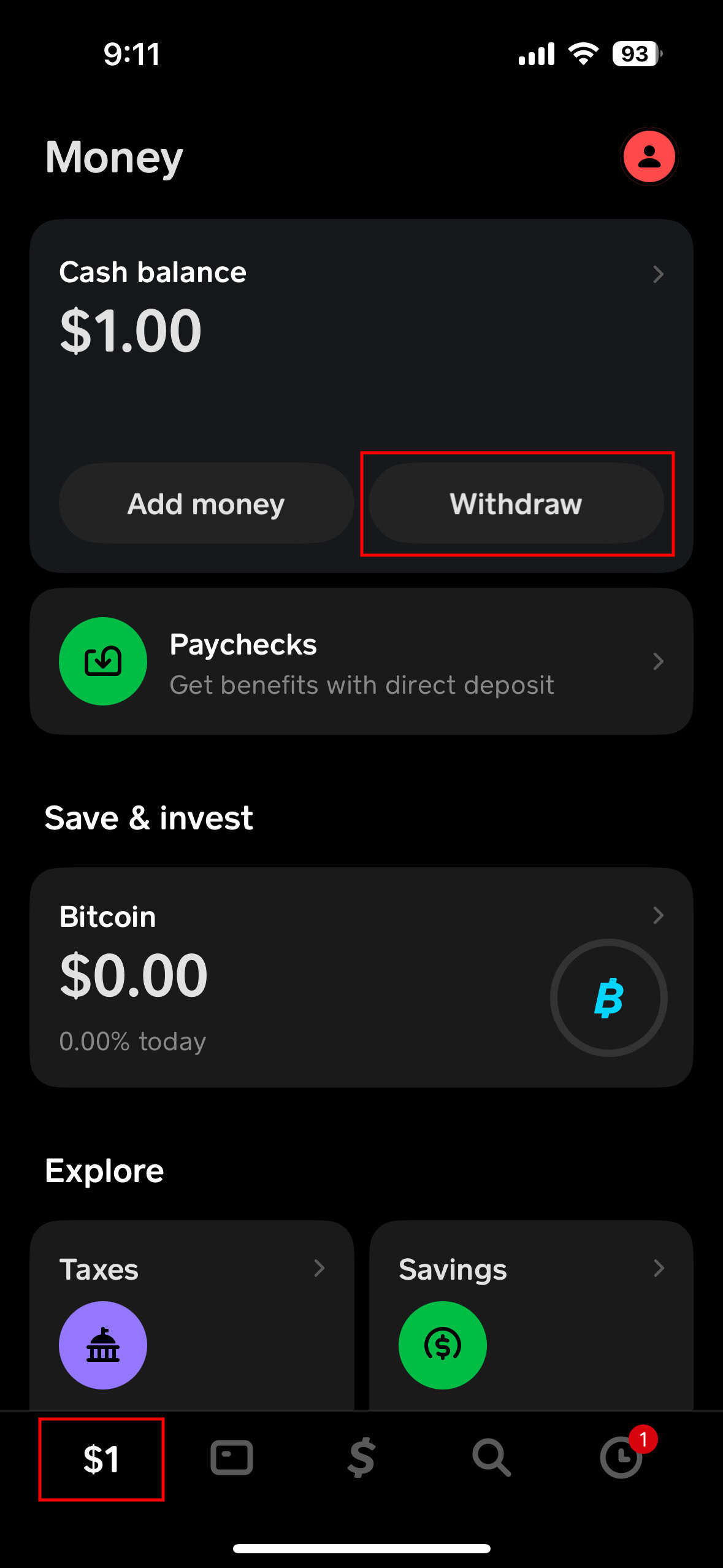

The most fundamental aspect of using Cash App is the ability to move digital balances into a physical or traditional bank environment. While the interface is designed for simplicity, there are strategic choices a user must make regarding speed and cost.

Understanding Standard vs. Instant Deposits

When you have a balance in your Cash App account and wish to transfer it to your linked bank account, you are presented with two primary options: Standard and Instant.

Standard deposits are free of charge and typically arrive within one to three business days. From a personal finance perspective, this is the preferred method for non-urgent funds, as it avoids unnecessary “leakage” through fees. Instant deposits, conversely, offer immediate liquidity but carry a fee (typically 0.5% to 1.75%, with a minimum fee). For those managing a tight cash flow or a business-oriented side hustle, these fees can accumulate, making it vital to plan withdrawals in advance to preserve capital.

Optimizing the Cash Card for Direct Access

For many users, “getting money” doesn’t necessarily mean transferring it to a bank. The Cash Card—a customizable Visa debit card linked to your balance—allows for direct spending or ATM withdrawals. To maximize the utility of this card, users should be aware of ATM fee reimbursements. Cash App often offers to reimburse ATM fees for users who receive a certain amount in direct deposits each month. This transforms the app into a functional checking account alternative, providing fee-free access to physical currency.

Troubleshooting Liquidity Barriers

Occasionally, users may encounter “pending” transactions or failed transfers. This often stems from security triggers or unverified account limits. To ensure seamless access to your money, it is imperative to complete the identity verification process (KYC – Know Your Customer). Verifying your account increases your sending and receiving limits, ensuring that larger sums of money are not trapped in a “pending” state during critical financial moments.

2. Strategic Income Generation Through the Cash App Ecosystem

Beyond simply moving money you already possess, Cash App offers several avenues to actively increase your net worth or generate incremental income. Within the “Money” niche, these are categorized as side hustles or optimization strategies.

Leveraging the Referral Architecture

One of the most straightforward ways to generate funds on Cash App is through its referral program. By inviting new users to the platform who then link a debit card and send a qualifying payment, both the referrer and the referee receive a cash bonus (typically ranging from $5 to $15). For those with a significant social or professional network, this can serve as a low-effort stream of referral income. The key to success here is transparency and helping the new user navigate their first transaction to ensure the bonus triggers correctly.

Capitalizing on Cash App “Boosts”

While often viewed as a discount tool, “Boosts” are effectively a form of immediate cash back, which functions as a direct increase in your disposable income. By selecting a specific “Boost” on your Cash Card—such as 10% off at a grocery store or $1 off a coffee shop visit—you are essentially keeping more money in your account. For the disciplined budgeter, these savings can be diverted into the app’s investment features, allowing “saved” money to become “invested” money.

Utilizing Cash App for Business and Freelancing

For freelancers and small business owners, Cash App offers a “Business Account” setting. This allows you to accept payments for goods and services legally and professionally. While business accounts incur a small transaction fee (2.75%), they provide a seamless way for clients to pay you instantly. Integrating Cash App into your professional payment stack can increase your “receivables” speed, improving the overall cash flow of your business operations.

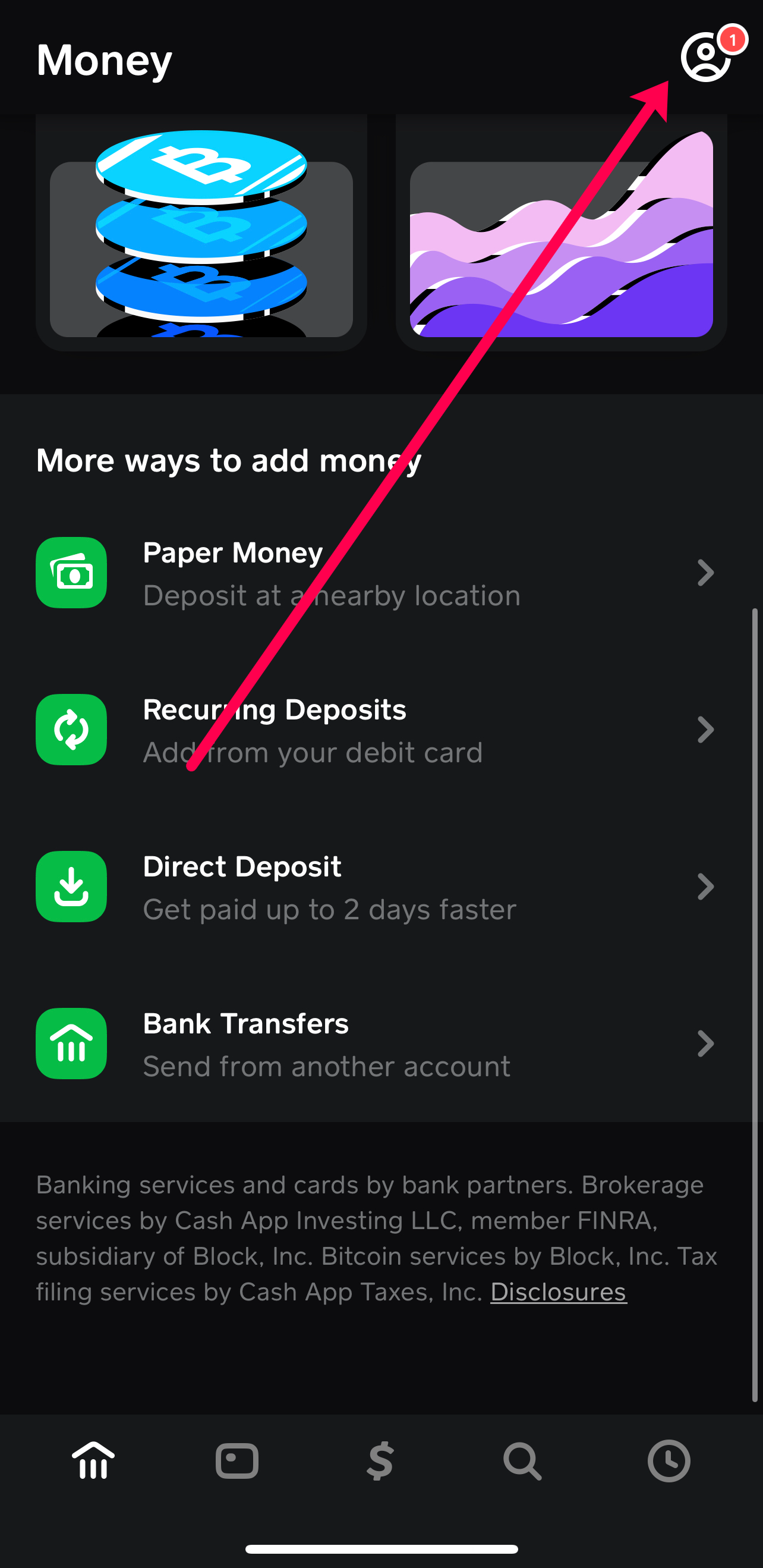

3. Wealth Building: Investing and Asset Liquidation

Cash App has democratized access to the financial markets by integrating stock and Bitcoin trading directly into the user interface. Understanding how to liquidate these assets is a crucial part of “getting money” from the platform.

Fractional Shares and Dividend Reinvestment

The platform allows users to buy as little as $1 of a company’s stock. This “fractional share” model is a powerful tool for building a portfolio over time. To get money out of these investments, a user must sell their shares. From a financial strategy standpoint, it is important to consider the timing of these sales to account for capital gains taxes. Furthermore, any dividends earned from these stocks are deposited directly into your Cash App balance, providing a source of passive income that can be spent or reinvested.

Bitcoin Liquidity and Transfers

Cash App is one of the most prominent gateways for Bitcoin. Users can buy, sell, and even withdraw Bitcoin to an external “cold” wallet. Getting money from Bitcoin involves either selling the asset for USD within the app—which can then be cashed out to a bank—or sending the Bitcoin to a different exchange. Because of Bitcoin’s volatility, savvy users often use the “Auto-Invest” feature to dollar-cost average, eventually selling portions of their holdings during market peaks to realize profits.

Tax Considerations for Digital Assets

When you earn money through stock sales or Bitcoin trading on Cash App, it is vital to remember that these are taxable events. Cash App provides 1099-B forms for its users. A professional approach to “getting money” from the app involves setting aside a percentage of your investment gains for tax season, ensuring that your net profit isn’t compromised by unforeseen liabilities.

4. Safeguarding Your Digital Capital

In the world of personal finance, keeping your money is just as important as getting it. The digital nature of Cash App makes it a target for various fraudulent schemes, and protecting your balance is paramount to your financial health.

Identifying and Avoiding P2P Scams

The most common way people “lose” rather than “get” money on Cash App is through social engineering scams. These include “cash flipping” schemes, fake customer support calls, or “accidental” payment requests. A professional rule of thumb: never send money to someone promising to “double” it, and always verify the $Cashtag of the recipient before confirming a transaction. Once a P2P payment is sent, it is nearly impossible to reverse, making caution your best financial defense.

Implementing Advanced Security Protocols

To ensure that your funds remain accessible only to you, you must utilize the app’s built-in security features. Enabling the “Security Lock” (which requires FaceID, TouchID, or a PIN for every transaction) is a non-negotiable step for anyone holding a significant balance. Additionally, setting up notification alerts for every transaction allows you to monitor your account in real-time, providing an early warning system against unauthorized access.

The Role of Cash App in a Diversified Financial Strategy

While Cash App is an excellent tool for liquidity and micro-investing, it should not be your only financial institution. Professional money management suggests using Cash App as a transactional hub rather than a long-term savings vault. By regularly “cashing out” your balance into a high-yield savings account (HYSA) or a diversified brokerage account, you ensure that your money is not only safe but also working for you at the highest possible interest rates.

Conclusion: The Future of Mobile Liquidity

Cash App has redefined what it means to “get money” in the 21st century. It is no longer just about cashing a paycheck; it is about managing a dynamic flow of peer-to-peer transfers, investment dividends, referral bonuses, and retail savings. By mastering the mechanics of withdrawals, leveraging the platform’s income-generating features, and maintaining a rigorous focus on security, users can turn Cash App into a sophisticated engine for personal financial growth. As digital finance continues to evolve, those who understand the nuances of these platforms will be best positioned to navigate the complex economy of tomorrow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.