Tax season is an indispensable part of the financial calendar, a period that prompts individuals and businesses alike to reconcile their financial activities with government regulations. Far from being a mere administrative chore, it is a critical juncture for personal finance planning, business compliance, and national economic health. Understanding when tax season officially begins, what factors influence its schedule, and how best to prepare for it is paramount for ensuring financial well-being and avoiding potential penalties. This comprehensive guide delves into the nuances of the annual tax cycle, equipping you with the knowledge to navigate it successfully.

Understanding the Federal Tax Filing Calendar

The commencement of tax season isn’t an arbitrary date; it’s a carefully orchestrated event by the Internal Revenue Service (IRS), designed to allow taxpayers ample time to gather their documentation and submit their returns. While specific dates can shift slightly year to year due to weekends or holidays, the general framework remains consistent.

The Standard Start Date: A Familiar Beginning

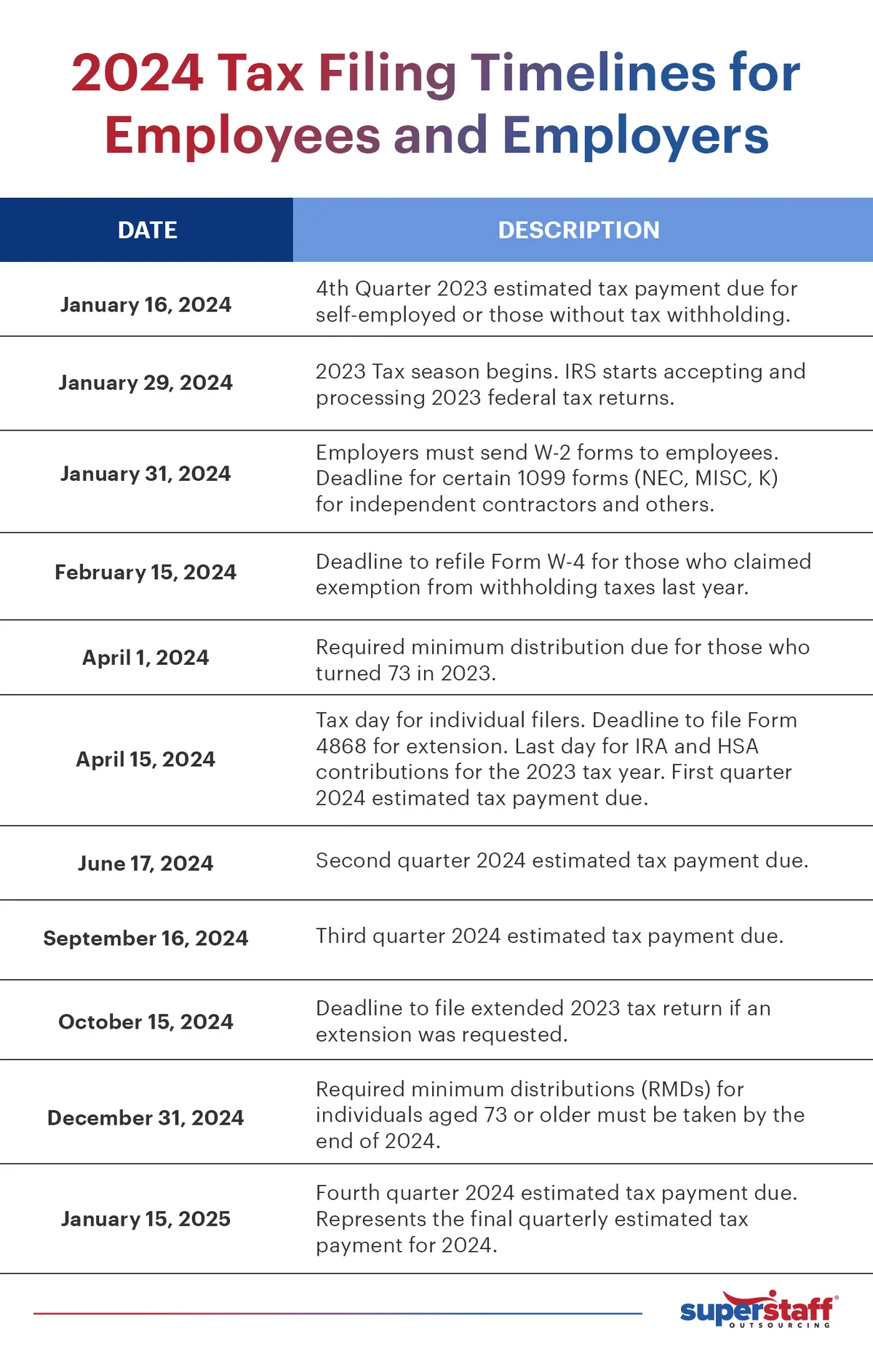

For the vast majority of taxpayers, primarily those filing individual income tax returns (Form 1040), tax season officially begins in late January. This is the date when the IRS typically starts accepting and processing tax returns for the previous calendar year. For instance, for the 2023 tax year, the IRS usually begins accepting returns in late January 2024. This timing is strategic, allowing employers and financial institutions sufficient time to issue necessary tax forms, such as W-2s (Wage and Tax Statement) and 1099s (Miscellaneous Income), to individuals. These forms, critical for accurately reporting income, are generally required to be sent out by January 31st. The synchronization ensures that by the time the IRS system opens, most taxpayers should have received the documents they need to file.

Key Deadlines: Mark Your Calendar

While the start date signals the opening of the filing window, the true milestone for most is the primary filing deadline. For individual federal income tax returns, this date is typically April 15th of each year. If April 15th falls on a weekend or a holiday, the deadline is shifted to the next business day. For example, if April 15th is a Saturday, the deadline moves to Monday, April 17th. This deadline also applies to payment of any taxes owed. It’s crucial to remember that filing an extension (Form 4868) extends the time to file your return, usually until October 15th, but it does not extend the time to pay any taxes due. Estimated taxes, for those with income not subject to withholding (e.g., self-employment income, rental income), have their own quarterly deadlines throughout the year (April 15, June 15, September 15, and January 15 of the following year), ensuring a more consistent flow of tax payments to the government.

The Role of the IRS: Setting the Schedule

The IRS is the federal agency responsible for collecting taxes and administering the Internal Revenue Code. It meticulously plans the tax season schedule, taking into account operational readiness, system testing, and legislative changes. The decision to open tax season on a specific date involves extensive preparation, including updating tax forms, refining processing systems, and disseminating information to taxpayers and tax preparers. Any significant changes in tax law, as often happens with new legislation, require substantial adjustments to IRS systems and forms, which can sometimes influence the precise start date or lead to delays in processing certain types of returns. The agency’s goal is to ensure a smooth, efficient, and secure filing process for millions of taxpayers.

Factors Influencing the Tax Season Timeline

While the general framework of tax season is stable, specific dates and operational nuances can be influenced by several external and internal factors. Being aware of these can help manage expectations and planning.

Weekends and Holidays: Shifting Deadlines

One of the most common reasons for a shift in tax deadlines is the occurrence of weekends and federal holidays. As mentioned, if April 15th lands on a Saturday or Sunday, the deadline is automatically moved to the next business day. Furthermore, certain holidays can also impact the schedule. For instance, Emancipation Day, observed in Washington D.C. on April 16th, can push the federal tax deadline to April 18th if April 15th falls on a Friday. This applies to all taxpayers across the country, not just those in D.C., due to the location of the IRS headquarters. Understanding these subtle shifts is vital for timely filing and payment, especially for those who tend to file closer to the deadline.

Economic Stimulus and Legislative Changes

Major legislative changes or economic events can significantly impact the tax season timeline and complexity. During times of economic crisis, such as the COVID-19 pandemic, Congress may pass relief legislation that introduces new tax credits, deductions, or even alters filing deadlines. For example, during the pandemic, the federal tax deadline was extended to July. Such changes require the IRS to update its systems, forms, and guidance, which can sometimes lead to later start dates for tax season or delays in processing certain types of returns (e.g., those claiming new or modified credits) while the IRS implements the new rules. Staying informed about current tax legislation is crucial, as it can directly affect your filing obligations and opportunities.

State Tax Considerations: A Separate but Linked Calendar

It’s important to remember that federal tax season is distinct from state tax season, though they are often closely linked. Most states that levy income tax have filing deadlines that largely mirror the federal April 15th deadline. However, there are exceptions. Some states have slightly different deadlines, and a few states do not impose a state income tax at all. Furthermore, state-specific extensions and payment rules may differ from federal guidelines. Businesses operating across multiple states or individuals with residency in different states within a single tax year must be particularly diligent in understanding the varying state tax requirements. Often, tax software can help synchronize federal and state filings, but it’s always wise to verify state-specific dates and rules.

Preparing for a Smooth Tax Season

Preparation is the cornerstone of a stress-free and accurate tax season. Proactive steps taken throughout the year and in the weeks leading up to the filing deadline can make a significant difference.

Gathering Your Documents: The Essential Checklist

The most critical step in preparing for tax season is organizing all necessary financial documents. This includes, but is not limited to:

- Income Statements: W-2s from employers, 1099 forms (1099-NEC for non-employee compensation, 1099-MISC for miscellaneous income, 1099-INT for interest, 1099-DIV for dividends, 1099-B for stock sales).

- Deductions and Credits: Receipts for charitable contributions, medical expenses, property taxes paid, mortgage interest statements (Form 1098), student loan interest statements (Form 1098-E), tuition statements (Form 1098-T), records for IRA contributions, and business expenses for self-employed individuals.

- Other Important Information: Social Security numbers for all family members, bank account information for direct deposit of refunds or direct debit of payments, and previous year’s tax returns for reference.

Creating a dedicated folder or digital file throughout the year for tax-related documents can prevent a frantic scramble come January.

Choosing Your Filing Method: DIY vs. Professional

Taxpayers have several options for filing their returns, each with its own advantages:

- DIY Tax Software: Platforms like TurboTax, H&R Block, and TaxAct offer user-friendly interfaces that guide individuals through the filing process. These are excellent for straightforward returns and can be cost-effective. Many offer free filing options for basic returns, particularly for lower-income taxpayers.

- IRS Free File: For taxpayers meeting certain income thresholds, the IRS offers free tax preparation software from various providers through its Free File program. This is a valuable resource for eligible individuals.

- Professional Tax Preparers: For complex returns (e.g., small businesses, multiple investments, significant life changes), consulting a certified public accountant (CPA) or enrolled agent (EA) is often advisable. Professionals can identify all applicable deductions and credits, ensure compliance, and represent you in case of an audit.

The choice largely depends on the complexity of your financial situation, your comfort level with tax forms, and your budget.

Proactive Planning: Beyond the Annual Rush

Effective tax planning extends beyond merely gathering documents at year-end. It involves strategic financial decisions throughout the year. For instance, adjusting W-4 withholdings with your employer can prevent a large tax bill or a disproportionately large refund, leading to better cash flow management. For self-employed individuals, regularly setting aside funds for estimated taxes and understanding quarterly payment obligations is crucial. Maintaining meticulous records for business expenses, investment gains and losses, and charitable contributions throughout the year simplifies the filing process and ensures you don’t miss out on potential deductions. Engaging in mid-year tax reviews with a financial advisor can help identify opportunities to optimize your tax situation before the year ends.

Maximizing Your Tax Season Outcomes

Tax season isn’t just about compliance; it’s also an opportunity to optimize your financial position by understanding and utilizing the tools available to you.

Understanding Deductions and Credits: Lowering Your Liability

One of the most impactful ways to optimize your taxes is to fully leverage available deductions and credits.

- Deductions reduce your taxable income. Examples include contributions to traditional IRAs, health savings accounts (HSAs), student loan interest, self-employment tax, and certain itemized deductions (e.g., mortgage interest, state and local taxes, charitable contributions). Choosing between the standard deduction and itemizing depends on which provides a greater reduction in your taxable income.

- Credits directly reduce the amount of tax you owe, dollar-for-dollar. Some credits, like the Earned Income Tax Credit (EITC) or the Child Tax Credit, can even be refundable, meaning they could result in a refund even if you owe no tax. Other common credits include education credits, dependent care credits, and various energy efficiency credits.

Understanding which deductions and credits apply to your unique situation is key to minimizing your tax liability or maximizing your refund.

What to Do if You Owe or Are Due a Refund

Once your return is filed, one of two scenarios typically unfolds: you either owe additional taxes or are due a refund.

- If You Owe: The IRS offers several payment options, including direct debit from your bank account, credit or debit card payments (though these often incur a processing fee), or sending a check or money order. It’s critical to pay by the deadline to avoid penalties and interest. If you cannot pay the full amount due, the IRS offers payment plans, such as short-term payment plans or installment agreements, which can help manage your obligation.

- If You Are Due a Refund: The fastest way to receive your refund is through direct deposit into your bank account. You can specify this when you file your return. The IRS also offers to mail a check, but this takes longer. You can track the status of your refund using the IRS “Where’s My Refund?” tool, which typically updates within 24 hours of e-filing.

Avoiding Common Pitfalls and Scams

Tax season is unfortunately also a prime time for scams. Be vigilant against phishing attempts (emails or calls pretending to be from the IRS demanding immediate payment or personal information), identity theft, and fraudulent tax preparers. The IRS typically initiates contact via mail, not unsolicited emails or phone calls, especially not demanding immediate payment via gift cards or wire transfers. Always verify the legitimacy of any communication. Furthermore, avoid common filing errors like math mistakes, incorrect Social Security numbers, or choosing the wrong filing status, as these can delay your refund or trigger an audit. Double-checking all information before submitting your return is a simple yet effective preventative measure.

The Broader Impact of Tax Season on Personal and Business Finance

Beyond the individual act of filing, tax season holds significant implications for broader financial planning and economic activity.

Financial Planning and Budgeting: Integrating Tax Obligations

For individuals, tax season serves as an annual financial health check-up. The process of gathering documents often reveals where money was spent, earned, and saved, providing valuable insights for future budgeting and financial planning. Understanding your tax liability and refund potential allows for better cash flow management throughout the year. For instance, anticipating a large refund might prompt you to adjust your withholdings to have more disposable income monthly, while consistently owing taxes might signal a need to save more or re-evaluate your tax strategy. Integrating tax considerations into your overall financial plan, including retirement planning and investment decisions, is a hallmark of sophisticated personal finance management.

Business Implications: Cash Flow and Compliance

For businesses, especially small and medium-sized enterprises (SMEs), tax season is a major financial event. It impacts cash flow directly, as businesses must set aside funds for corporate income taxes, payroll taxes, and self-employment taxes. Accurate record-keeping throughout the year is not just good practice; it’s essential for demonstrating compliance and maximizing legitimate business deductions. The financial burden and administrative complexity of tax season often necessitate dedicated accounting staff or professional services. Failure to comply can result in severe penalties, audits, and damage to a business’s reputation. Proactive tax planning, including understanding quarterly estimated tax requirements, is crucial for business sustainability and growth.

Economic Ripple Effects: Refunds and Spending

The sheer volume of money that flows through the economy during tax season creates significant ripple effects. Tax refunds, which can total hundreds of billions of dollars annually, often stimulate consumer spending, providing a boost to various sectors of the economy, from retail to automotive. Conversely, the collection of tax revenues funds public services, infrastructure projects, and government operations. The collective behavior of millions of taxpayers, whether they are receiving refunds or paying taxes, thus plays a substantial role in the nation’s economic rhythm. Policymakers often consider these economic impacts when debating tax law changes or stimulus packages.

In conclusion, knowing “when tax season starts” is merely the first step in a much larger and more intricate financial journey. It is a time for introspection, meticulous organization, and strategic planning. By understanding the federal and state calendars, preparing diligently, and leveraging available financial tools and professional advice, individuals and businesses can transform this annual obligation into an opportunity for financial optimization and stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.