The annual ritual of tax filing can often feel like a looming deadline, a complex puzzle, or for some, an exciting opportunity for a refund. Regardless of your perspective, understanding when you can file your taxes is the first critical step toward fulfilling your obligations and managing your personal finances effectively. This article delves into the specifics of the 2024 tax filing season, clarifying key dates, offering strategic advice, and providing a roadmap to ensure a smooth and successful tax experience.

It’s crucial to clarify upfront what “filing your 2024 taxes” actually means. In the context of the calendar year, “2024 taxes” typically refers to the taxes you are filing during the 2024 calendar year for the 2023 tax year. The tax year describes the period for which income was earned and expenses incurred, while the filing year is when you submit the return. So, when we talk about filing your 2024 taxes, we are primarily discussing your income and activities from January 1 to December 31, 2023, which you will report to the IRS and state tax authorities in 2024. Getting these timelines straight is fundamental to navigating the tax season without confusion or missteps.

Understanding the 2024 Tax Filing Season: What to Expect

The tax filing season is a predictable annual event, yet each year brings subtle nuances and specific dates that taxpayers must be aware of. For the 2024 season, taxpayers will be primarily concerned with reporting their financial activities from the 2023 calendar year.

Differentiating Tax Year from Filing Year

One of the most common sources of confusion for taxpayers is the distinction between the “tax year” and the “filing year.” The tax year refers to the period during which income was earned and deductions/credits were accrued – in this case, January 1, 2023, through December 31, 2023. The filing year is the calendar year in which you prepare and submit your tax return for that previous tax year. Therefore, when you “file your 2024 taxes,” you are submitting a return for the 2023 tax year. This clarity is vital for accurately gathering documents, understanding deadlines, and avoiding unnecessary penalties.

The IRS’s Annual Opening Day

Every year, the Internal Revenue Service (IRS) announces an official start date for processing tax returns. This date marks when their systems are fully operational to accept electronically filed returns. While the exact date varies slightly from year to year, it generally falls in late January. For the 2024 filing season (for 2023 tax returns), taxpayers can expect the IRS to begin accepting e-filed returns sometime around the last week of January. Historically, the IRS usually provides ample notice of this date. It’s important to remember that while tax software and tax professionals might allow you to prepare your return earlier, they typically hold onto it until the IRS systems are ready to officially receive it.

Why the Dates Matter for Your Financial Planning

Understanding the tax season’s timeline is more than just about avoiding penalties; it’s a critical component of sound financial planning. Knowing when you can file allows you to:

- Plan for refunds: If you expect a refund, filing early means getting your money back sooner, which can be invested, saved, or used to pay down debt.

- Prepare for payments: If you anticipate owing taxes, knowing the deadlines gives you time to budget and save the necessary funds, preventing last-minute financial strain.

- Reduce stress: Proactive tax preparation and filing eliminate the anxiety associated with procrastination, allowing for a more thoughtful and accurate submission.

- Identity theft protection: Filing early can reduce the risk of tax identity theft, as fraudsters are less likely to successfully file a fraudulent return using your information if yours has already been processed.

Key Dates and Deadlines: Navigating the 2024 Tax Calendar

The 2024 tax filing season comes with several critical dates that every taxpayer should mark on their calendar. Missing these deadlines can lead to penalties and unnecessary financial headaches.

The Official Start Date for E-filing

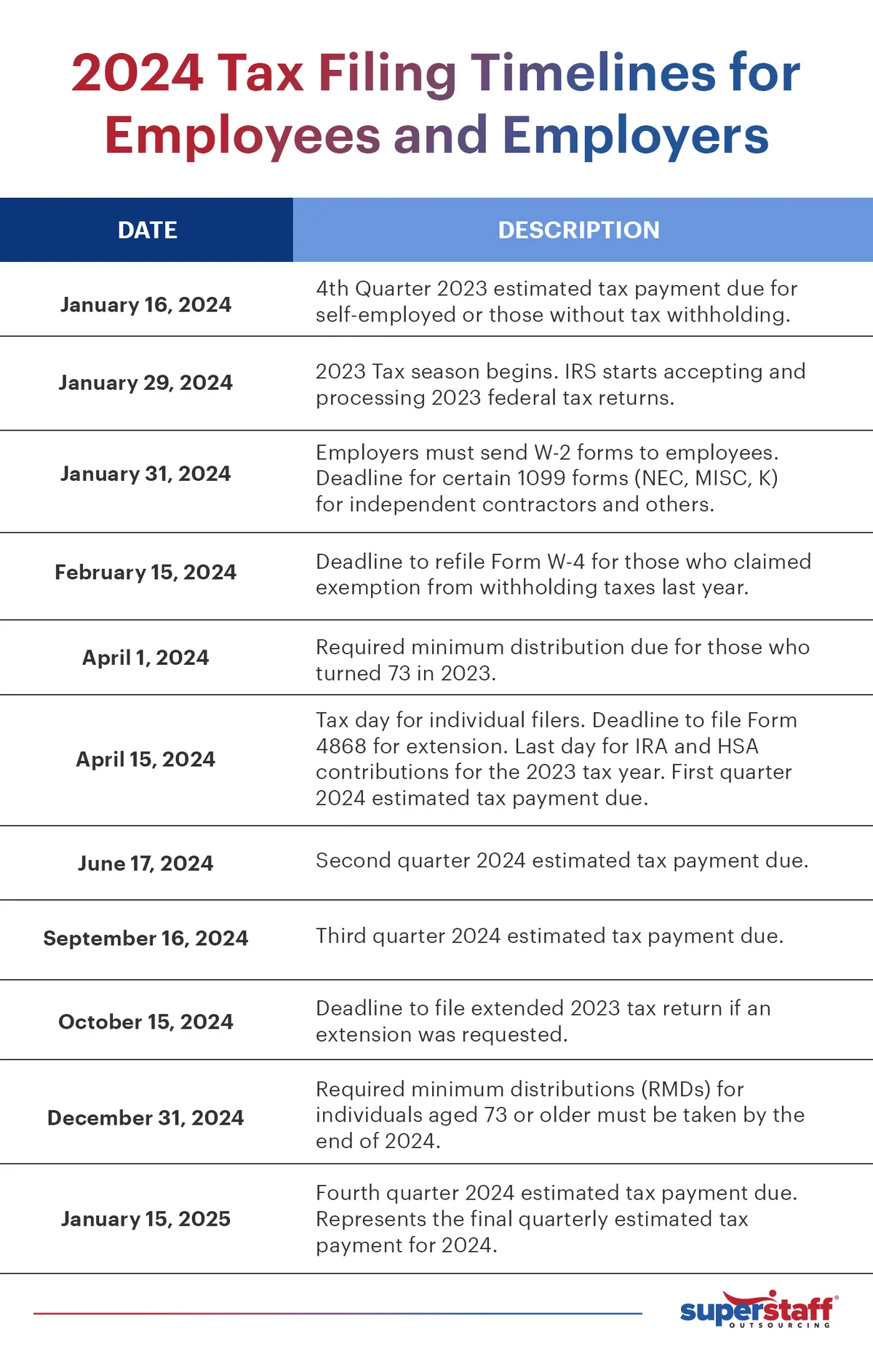

As mentioned, the IRS typically begins accepting e-filed returns in late January. While the exact date for the 2024 filing season (for 2023 tax returns) is usually announced by the IRS in December or early January, taxpayers should anticipate that they can start submitting their returns around January 29, 2024. This date is crucial for those eager to receive their refunds quickly or simply get their tax obligations out of the way. Prior to this date, tax preparation software and professionals can help you compile your information, but the actual submission to the IRS will be held until their systems open.

The Primary Filing Deadline

For most individual taxpayers, the unwavering cornerstone of the tax calendar is the mid-April deadline. For the 2024 tax season, the primary deadline to file your 2023 federal income tax return is Monday, April 15, 2024. This date also serves as the deadline for paying any taxes owed. If April 15th falls on a weekend or a holiday, the deadline shifts to the next business day. For instance, if April 15th, 2024 were a Saturday, the deadline would move to April 17th. However, since April 15, 2024, is a Monday, it stands as the firm deadline for most. Special rules apply to residents of Maine and Massachusetts due to Patriots’ Day and Emancipation Day in Washington D.C., respectively, which can push their state and sometimes federal filing deadlines a few days later.

Estimated Tax Payment Deadlines

For self-employed individuals, freelancers, gig workers, and those with significant income not subject to withholding, estimated tax payments are a quarterly requirement. While the focus of this article is primarily on the annual filing, it’s worth noting these deadlines as they are integral to the 2024 financial calendar. For the 2024 tax year (income earned in 2024, filed in 2025), the estimated payment due dates are:

- Q1 2024: April 15, 2024

- Q2 2024: June 15, 2024

- Q3 2024: September 15, 2024

- Q4 2024: January 15, 2025

Missing these payments or underpaying can result in penalties, even if you eventually receive a refund when you file your annual return.

Understanding Extension Deadlines

If you find yourself unable to meet the April 15th deadline, you can file for an extension. An extension typically grants you an additional six months to file your federal tax return, pushing the deadline to October 15, 2024. It is critically important to understand that an extension to file is not an extension to pay. If you anticipate owing taxes, you must still estimate and pay those taxes by April 15th to avoid penalties and interest. Failure to pay by the original deadline will result in penalties, even if you have an approved extension to file.

Preparing for a Smooth Tax Season: Essential Steps Before You File

A well-prepared taxpayer is a less stressed taxpayer. Taking proactive steps before the filing season officially opens can significantly streamline the process and potentially maximize your financial outcomes.

Gathering Your Critical Documents

The foundation of any accurate tax return is a complete set of financial documents. Begin collecting these as soon as they become available, typically in late January and early February:

- Income Statements: W-2s from employers, 1099-NEC (non-employee compensation), 1099-MISC, 1099-INT (interest income), 1099-DIV (dividend income), 1099-R (retirement distributions), K-1s (from partnerships, S corporations, and trusts), Social Security benefit statements (SSA-1099).

- Investment and Savings: Statements from brokerage accounts, cryptocurrency exchanges, and bank accounts.

- Deduction and Credit Documentation: Mortgage interest statements (Form 1098), student loan interest statements (Form 1098-E), tuition statements (Form 1098-T), records of charitable contributions, medical expense receipts, childcare expenses, and property tax bills.

- Identity Information: Your Social Security number (SSN) or Individual Taxpayer Identification Number (ITIN), and those for your spouse and dependents.

Organizing these documents systematically – perhaps in a dedicated folder or digital file – will save you considerable time and potential headaches.

Reviewing Your Prior Year’s Returns

Your previous year’s tax returns are invaluable resources. They provide a historical record of your income sources, deductions you’ve claimed, and credits you’ve received. Reviewing them can help you:

- Identify recurring items: Remind you of standard deductions, credits, or income sources that are likely to apply again.

- Spot changes: Highlight areas where your financial situation might have changed (e.g., new job, new home, marriage, birth of a child), prompting you to investigate new deductions or credits.

- Prevent errors: Serve as a template to ensure you haven’t forgotten anything critical from one year to the next.

Identifying Potential Deductions and Credits

Tax laws are complex, but understanding common deductions and credits can significantly reduce your tax liability or increase your refund. Familiarize yourself with:

- Standard vs. Itemized Deductions: Most taxpayers take the standard deduction, but if your itemized deductions (e.g., mortgage interest, state and local taxes, medical expenses, charitable contributions) exceed the standard amount, itemizing could save you money.

- Common Credits: These include the Child Tax Credit, Earned Income Tax Credit (EITC), American Opportunity Tax Credit (AOTC), Lifetime Learning Credit, and various clean energy or energy efficiency credits. Eligibility for credits often depends on income thresholds and specific criteria, so careful review is essential.

Choosing Your Filing Method: Software vs. Professional

Deciding how you’ll prepare and file your taxes is another crucial step:

- DIY Tax Software: Solutions like TurboTax, H&R Block, and TaxAct offer user-friendly interfaces that guide you through the process, often with various tiers catering to different levels of complexity. This can be cost-effective for straightforward returns.

- Online Services: The IRS offers “IRS Free File” for eligible taxpayers (generally those with income below a certain threshold), providing access to guided tax preparation software from commercial partners at no cost.

- Tax Professionals: For complex returns, significant life changes, or if you simply prefer expert assistance, a Certified Public Accountant (CPA) or Enrolled Agent (EA) can provide invaluable guidance, ensure accuracy, and help identify all eligible deductions and credits.

Strategic Filing: Advantages of Early Filing vs. The Risks of Delay

The timing of your tax filing can have significant implications for your financial well-being and peace of mind. While the option to extend is available, understanding the pros and cons of filing early versus waiting until the last minute is crucial.

Benefits of Filing Early

- Faster Refunds: The most tangible benefit for many. The sooner you file, the sooner the IRS processes your return and issues any refund you’re due.

- Less Stress: Getting your taxes done well in advance eliminates the last-minute scramble and anxiety, freeing up mental space for other priorities.

- More Time to Pay if You Owe: If you discover you owe taxes, filing early gives you more time to arrange for payment by the April 15th deadline, rather than facing an immediate bill with little warning.

- Reduced Risk of Identity Theft: Filing your return before fraudsters can use your Social Security number to file a fake return in your name protects you from a potentially lengthy and frustrating identity theft recovery process.

- Opportunity to Correct Errors: Early filers have more time to review their returns thoroughly and make corrections if needed, minimizing the chance of IRS scrutiny.

Common Pitfalls of Procrastination

- Rushed Mistakes: Filing under pressure can lead to errors, missed deductions, or incorrect calculations, potentially triggering an audit or delaying a refund.

- Missed Deductions/Credits: A hurried process might mean overlooking eligible deductions or credits, resulting in a higher tax bill than necessary.

- Difficulty Getting Professional Help: Tax professionals are swamped closer to the deadline. Waiting too long might mean you can’t find an appointment or pay surge pricing.

- Potential for Penalties: If you owe taxes and miss the April 15th payment deadline, you will incur penalties and interest, which can significantly increase your overall tax burden.

What to Do If You Can’t File on Time: The Extension Process

Life happens, and sometimes meeting the April 15th deadline is genuinely impossible. In such cases, the IRS offers a straightforward solution: filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return.

- How to File: You can file Form 4868 electronically through tax software, via a tax professional, or by mail. It’s a simple form that only requires basic identifying information.

- Extension to File, Not to Pay: Reiterate this critical point. An extension gives you until October 15th to submit your return, but any taxes you owe are still due by April 15th.

- Estimate and Pay: If you’re filing an extension, you should make your best estimate of your tax liability and pay that amount by April 15th. If you underpay, you’ll still be subject to penalties and interest on the unpaid amount. If you overpay, the excess will be refunded or credited to the next year.

Beyond Filing: Post-Submission Considerations and Future Planning

Once your tax return is filed, the immediate pressure is off, but your engagement with your finances shouldn’t end there. There are important post-submission considerations and proactive steps you can take for future financial health.

Understanding Your Refund or Payment Obligations

- Receiving a Refund: If you’re due a refund, the IRS typically issues it within 21 days for e-filed returns with direct deposit. Consider how you’ll utilize this extra cash – perhaps to build an emergency fund, pay down high-interest debt, invest for retirement, or make a significant purchase. Strategically allocating your refund can have a lasting positive impact on your financial standing.

- Making a Payment: If you owe taxes, ensure you make the payment by the April 15th deadline (or by October 15th if you filed an extension and paid an estimated amount by April 15th). The IRS offers various payment methods, including direct debit from your bank account, credit or debit card payments (though these often involve a processing fee), and payment plans if you cannot pay the full amount immediately.

The Importance of Record Keeping

Tax season doesn’t end when you hit “submit.” Proper record-keeping is vital for several reasons:

- Audit Protection: If the IRS ever audits your return, you’ll need documentation to substantiate all income, deductions, and credits claimed.

- Future Reference: Retaining past returns and supporting documents provides a valuable financial history.

- How Long to Keep Records: Generally, the IRS recommends keeping tax records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. For specific situations, like if you filed a claim for a loss from worthless securities or bad debt deduction, the period can extend to seven years.

Planning for the Next Tax Year

A key aspect of sound financial planning is to use insights from your current tax filing to prepare for the future.

- Adjusting Withholdings: If you received a large refund, it might mean you’re overpaying taxes throughout the year. Consider adjusting your W-4 form with your employer to have less tax withheld, putting more money in your pocket each payday. Conversely, if you owed a significant amount, you might want to increase your withholdings to avoid a large tax bill next year.

- Setting Up Estimated Payments: If you’re self-employed or have non-W-2 income, re-evaluate your estimated tax payments for the current year (2024 tax year) to ensure you’re paying enough to avoid penalties.

- Saving for Future Tax Liabilities: If you anticipate owing taxes next year, start setting aside money regularly in a separate savings account.

- Reviewing Tax-Advantaged Accounts: Maximize contributions to 401(k)s, IRAs, HSAs, and other tax-advantaged accounts. These not only help you save but also provide significant tax benefits.

- Consulting a Financial Advisor: Consider meeting with a financial advisor or tax professional to review your overall financial strategy and identify opportunities for tax optimization and wealth growth.

The 2024 tax filing season, primarily for your 2023 income, is an annual opportunity to ensure your financial house is in order. By understanding the key dates, preparing thoroughly, and making informed decisions about when and how to file, you can navigate the process efficiently, reduce stress, and potentially enhance your financial well-being. Proactive engagement with your taxes isn’t just a compliance exercise; it’s a fundamental pillar of effective personal finance management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.