The annual rhythm of tax season can feel both inevitable and, for many, a source of anxiety. As we turn the calendar page, a common question resurfaces: “When can we start filing taxes for 2024?” It’s a crucial inquiry that signals the beginning of an important financial responsibility for millions of Americans. To clarify, when we talk about “filing taxes for 2024,” we are generally referring to the tax return for the 2023 tax year, which is prepared and submitted in the calendar year 2024. This period demands a meticulous approach to financial record-keeping, an understanding of current tax laws, and timely action. This guide will provide a comprehensive overview of when you can expect to file, what you need to prepare, and strategies to navigate the tax season effectively, ensuring you meet your obligations and potentially maximize your financial outcomes.

The Official Start of Tax Season: What to Expect

The Internal Revenue Service (IRS) is the ultimate authority when it comes to announcing the official start date for tax season. While the exact date can shift slightly from year to year, it typically falls in late January. This announcement is eagerly anticipated by taxpayers, tax professionals, and tax software providers alike, as it marks the moment the IRS systems are ready to begin processing returns.

IRS Announcements and Key Dates

Historically, the IRS has opened its filing season around the third or fourth week of January. For instance, the 2023 tax season (for tax year 2022) officially began on January 23, 2023. This pattern provides a strong indication of when we can expect the 2024 filing season to commence. The IRS makes this announcement publicly through press releases and updates on its official website. It’s advisable to monitor these official channels as January approaches to get the precise date. This opening day is significant because it’s when the IRS begins accepting and processing electronically filed tax returns, and also when most tax software and professional preparers can officially submit returns on behalf of their clients. While you might be able to prepare your return earlier, actual submission must wait until this date.

Why the IRS Waits

The IRS doesn’t simply open its doors on January 1st. There are several critical reasons for this deliberate delay. Primarily, the agency needs time to finalize programming and test its systems to ensure they can accurately process all forms and account for any new tax legislation or changes. The end of the calendar year often sees a flurry of legislative activity, and the IRS must integrate these changes into its processing infrastructure. Furthermore, employers and financial institutions have deadlines (typically late January to early February) to issue essential tax documents like W-2s and various 1099 forms. Waiting until these documents are widely available ensures taxpayers have the necessary information to file accurate returns from the outset, reducing the need for amendments later. This synchronization helps prevent errors and streamlines the overall filing process for both taxpayers and the agency.

Early Preparations You Can Make

Even before the IRS officially opens the filing season, there’s plenty you can do to get a head start. Proactive preparation can significantly reduce stress and the likelihood of errors. Begin by gathering all potential tax documents as they arrive. Create a dedicated folder, either physical or digital, where you can store W-2s, 1099s, receipts for deductible expenses, and any other relevant financial statements. Review your income and expenses from the past year. If you had significant life changes – like marriage, a new baby, purchasing a home, or starting a new job – understand how these might impact your tax situation. Accessing your IRS online account can also be beneficial for retrieving past tax transcripts, checking your estimated tax payments, or confirming the status of a previous year’s refund. These early steps ensure that once the filing season officially begins, you’ll be well-equipped to complete your return efficiently and accurately.

Gathering Your Essential Tax Documents

The cornerstone of an accurate tax return is comprehensive documentation. Without the right forms and statements, you risk errors, delays, or even missing out on valuable deductions and credits. The period leading up to the filing season is prime time for these documents to arrive in your mailbox or digital inbox.

Income Documentation (W-2s, 1099s)

The most common income documents are your W-2s from employers. By law, employers must furnish these forms to employees by January 31st. If you’ve worked for multiple employers in the tax year, you’ll receive a W-2 from each. Beyond W-2s, many individuals receive various 1099 forms:

- 1099-NEC (Nonemployee Compensation): For independent contractors or self-employed individuals paid over $600.

- 1099-MISC (Miscellaneous Income): For other types of income like rent, prizes, or awards.

- 1099-INT (Interest Income): From banks and other financial institutions for interest earned.

- 1099-DIV (Dividends and Distributions): From investments, including stocks and mutual funds.

- 1099-R (Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.): For withdrawals from retirement accounts.

- 1099-G (Certain Government Payments): For unemployment compensation, state/local tax refunds, etc.

- 1099-K (Payment Card and Third-Party Network Transactions): For income received through payment apps or online marketplaces.

Ensure you collect all relevant 1099s, as they document income that the IRS is also aware of.

Deduction and Credit Documentation

To claim valuable deductions and credits, you need supporting documentation. This includes:

- Mortgage Interest Statement (Form 1098): For homeowners, detailing mortgage interest paid.

- Student Loan Interest Statement (Form 1098-E): For those paying student loan interest.

- Tuition Statement (Form 1098-T): For education credits.

- Childcare Expense Statements: Receipts or statements from daycare providers, including their tax ID.

- Charitable Contribution Records: Receipts for cash donations, appraisals for non-cash donations, and acknowledgement letters for donations over certain thresholds.

- Medical Expense Records: If you itemize, keep track of out-of-pocket medical and dental expenses.

- Property Tax Records: For homeowners.

- Business Expenses: For self-employed individuals, detailed records of all business-related income and expenses are critical.

Investment and Retirement Account Statements

If you have investments, you’ll receive additional forms:

- Form 1099-B (Proceeds From Broker and Barter Exchange Transactions): Reports capital gains and losses from stock sales, mutual funds, etc.

- Consolidated 1099s: Many brokerage firms combine various 1099s (INT, DIV, B) into one consolidated statement.

- Form 5498 (IRA Contribution Information): Details contributions made to IRAs, though these usually arrive later in the year after the tax deadline, as contributions can be made up until the tax deadline itself.

Other Important Forms

Don’t overlook other potentially crucial documents:

- Health Insurance Forms (1095-A, 1095-B, 1095-C): If you purchased health insurance through the marketplace, received employer-sponsored coverage, or have Medicaid/Medicare, these forms confirm your health coverage status. Form 1095-A is particularly important if you received premium tax credits.

- Schedule K-1 (Partner’s Share of Income, Deductions, Credits, etc.): For individuals involved in partnerships, S corporations, or certain trusts and estates. These forms can sometimes arrive later than other documents, potentially delaying filing.

Organizing these documents as they arrive will save you significant time and stress once you begin preparing your return.

Choosing Your Filing Method: Navigating the Options

With all your documents in hand, the next decision is how to actually file your return. There are several viable methods, each with its own advantages and disadvantages, catering to different levels of tax complexity and personal preferences.

Professional Tax Preparers

For those with complex tax situations, significant life changes, or simply a desire for expert assistance, a professional tax preparer can be invaluable. This includes Certified Public Accountants (CPAs), Enrolled Agents (EAs), or other qualified tax preparers.

- Benefits: Expertise in complex tax law, identification of all eligible deductions and credits, assistance with audits, peace of mind, and time-saving.

- Costs: Can range from a few hundred dollars to several thousand, depending on the complexity of your return.

- When to Consider: If you own a business, have investments, significant rental income, foreign income, or want personalized financial planning advice. Always verify their credentials and ensure they have an IRS Preparer Tax Identification Number (PTIN).

Tax Software Solutions

For many individuals, tax software offers a cost-effective and efficient way to file taxes. Popular options include TurboTax, H&R Block Tax Software, TaxAct, and FreeTaxUSA.

- Features: Guided question-and-answer formats, automatic calculations, error checks, direct e-filing. Most offer different versions (e.g., free, deluxe, premier) based on the complexity of your return.

- Pros: Generally cheaper than professional preparers, convenient (can be done from home), user-friendly interfaces, often include state filing options.

- Cons: Requires some self-reliance, may not catch every nuance of complex situations, can still be confusing for those unfamiliar with tax concepts.

Most software providers allow you to start inputting information even before the IRS officially opens the filing season, holding your return until it’s time to submit.

Free File Options (IRS Free File Program)

The IRS offers a program called Free File, which allows eligible taxpayers to prepare and e-file their federal tax returns for free using guided tax software.

- Eligibility: Typically, your Adjusted Gross Income (AGI) must be below a certain threshold (which changes annually). For example, for the 2023 tax year, the AGI limit was $79,000 for most providers participating in the program.

- How to Access: You must access Free File through the IRS.gov website to ensure you’re using a legitimate partner product. Do not go directly to a company’s website, as you may be routed to a paid version.

- Benefits: Completely free for federal returns (some state returns may also be free), provides the same high-quality software experience as paid versions, secure e-filing.

For those who do not qualify for Free File, the IRS also offers “Free File Fillable Forms,” which are electronic versions of paper IRS forms that you fill out yourself. This option is best for taxpayers comfortable doing their own tax calculations without software assistance.

DIY Paper Filing

The traditional method of printing out forms, filling them in manually, and mailing them to the IRS is still an option, though it’s increasingly less common.

- Pros: No software or preparer fees.

- Cons: Prone to manual errors, slower processing (refunds take longer), requires you to calculate everything yourself, postage costs.

- Recommendation: E-filing is highly recommended due to its speed, accuracy checks, and confirmation of receipt.

Understanding Key Deadlines and Potential Extensions

Meeting deadlines is paramount in tax filing. Missing them can result in penalties and interest. Understanding the critical dates and how to handle unforeseen delays is a key aspect of responsible financial management.

The Primary Filing Deadline

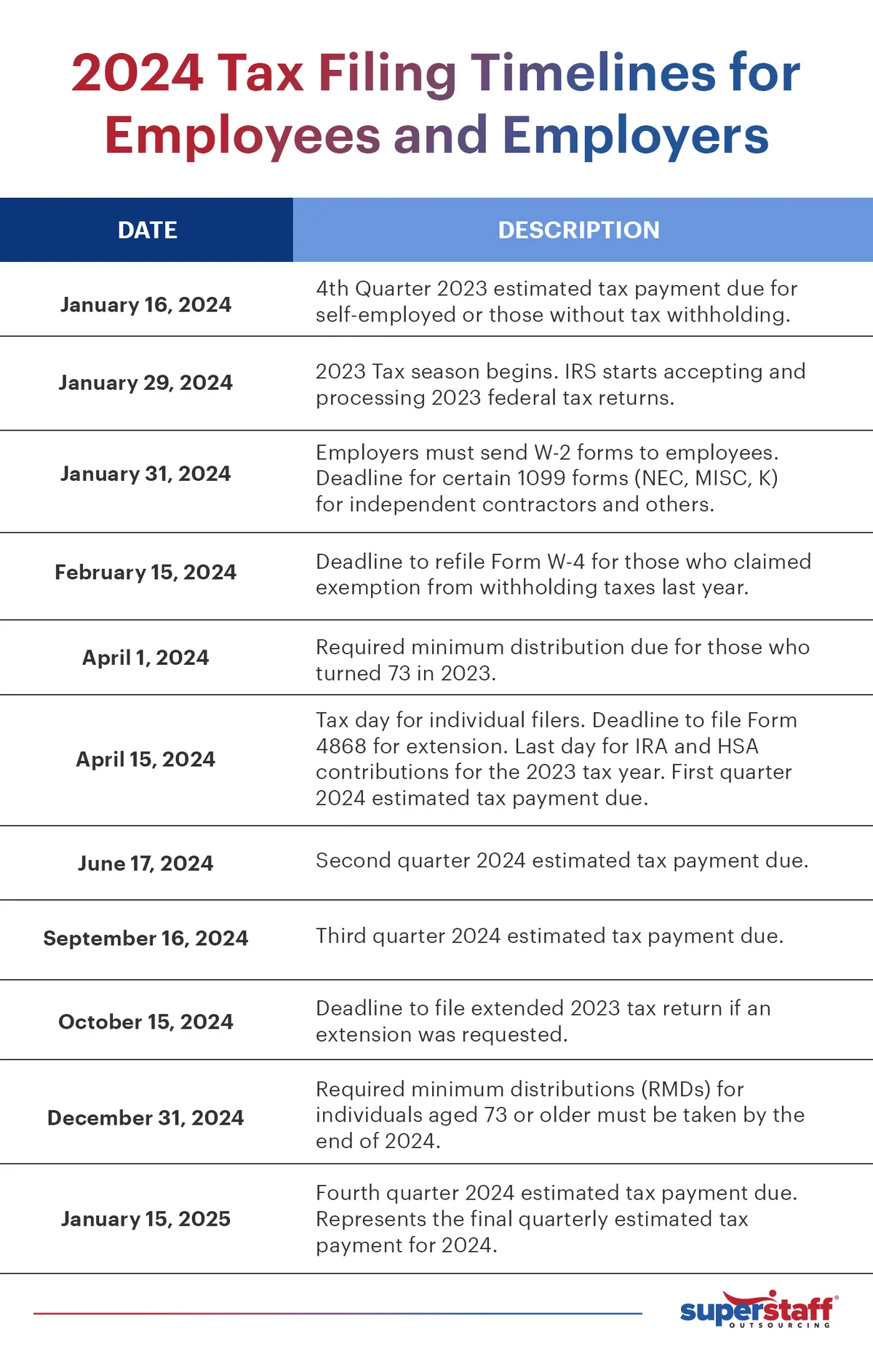

For most individual taxpayers, the primary deadline to file federal income tax returns and pay any taxes owed for the 2023 tax year is April 15, 2024. If April 15th falls on a weekend or holiday, the deadline is typically shifted to the next business day. It’s crucial to remember that state income tax deadlines may differ, so check your state’s tax agency for their specific dates.

Estimated Taxes

If you are self-employed, an independent contractor, or have significant income not subject to withholding (e.g., interest, dividends, rental income), you may be required to pay estimated taxes throughout the year. These payments are typically due quarterly:

- Quarter 1 (Jan 1 to Mar 31): Due April 15, 2024

- Quarter 2 (Apr 1 to May 31): Due June 15, 2024

- Quarter 3 (June 1 to Aug 31): Due September 15, 2024

- Quarter 4 (Sep 1 to Dec 31): Due January 15, 2025 (for the 2024 tax year)

Failing to pay enough estimated tax throughout the year can result in penalties, even if you receive a refund when you file your annual return.

Filing for an Extension

If you find that you cannot file your tax return by the April 15th deadline, you can request an extension. Filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return, will grant you an automatic six-month extension to file your return, typically pushing the deadline to October 15th.

- Important Note: An extension to file is not an extension to pay. If you owe taxes, you must still estimate and pay them by the April 15th deadline to avoid interest and penalties. Failing to pay on time, even with an extension to file, will result in penalties and interest accruing on the unpaid amount from April 15th until the date you pay.

Penalties for Late Filing and Payment

The IRS imposes penalties for both late filing and late payment.

- Failure to File Penalty: This is 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid taxes. If your return is more than 60 days late, the minimum penalty is $485 (for returns due in 2024) or 100% of the tax due, whichever is less.

- Failure to Pay Penalty: This is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25%.

- Interest: In addition to penalties, the IRS charges interest on underpayments and unpaid taxes, which can fluctuate.

It’s crucial to understand these consequences and take action to avoid them, either by filing on time or by requesting an extension and paying your estimated tax liability.

Proactive Tax Planning for the Future

Tax season doesn’t have to be an annual scramble. By adopting proactive tax planning strategies, you can minimize stress, optimize your financial position, and potentially reduce your tax liability year after year.

Quarterly Check-ins and Withholding Adjustments

Don’t wait until January to review your tax situation. Throughout the year, especially after significant life events (new job, marriage, birth of a child, major income changes), perform a “tax check-up.”

- Adjust Withholding: Use the IRS Tax Withholding Estimator (IRS.gov/W4App) to ensure your employer is withholding the correct amount of tax from your paychecks. Adjusting your W-4 can help you avoid a large tax bill at the end of the year or a large refund (which essentially means you gave the government an interest-free loan).

- Review Estimated Taxes: If you pay estimated taxes, review your income and expenses quarterly to ensure your payments are accurate.

Maximizing Deductions and Credits

Understanding and utilizing available deductions and credits is key to reducing your taxable income.

- Itemize vs. Standard Deduction: Keep good records throughout the year for potential itemized deductions (medical expenses, state and local taxes, mortgage interest, charitable contributions). At tax time, compare the total of your itemized deductions against the standard deduction for your filing status and choose the option that yields the lower tax bill.

- Retirement Contributions: Maximize contributions to tax-advantaged retirement accounts like 401(k)s and IRAs. Traditional IRA contributions are often deductible, and contributions to Roth accounts grow tax-free.

- Health Savings Accounts (HSAs): If you have a high-deductible health plan, contribute to an HSA. Contributions are tax-deductible, grow tax-free, and qualified withdrawals are tax-free.

- Education Credits: Explore credits like the American Opportunity Tax Credit or Lifetime Learning Credit if you or your dependents are pursuing higher education.

Record-Keeping Best Practices

The bedrock of effective tax planning is meticulous record-keeping.

- Digital vs. Physical: Choose a system that works for you. Digitize receipts and statements, or maintain organized physical folders.

- Categorize Expenses: For self-employed individuals, categorize all business income and expenses regularly to simplify Schedule C preparation.

- Proof of Donations: Keep receipts for all charitable contributions, and for larger donations, ensure you have official acknowledgment letters.

- Hold onto Records: The IRS generally recommends keeping tax records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. For certain situations (e.g., claiming a loss from worthless securities), the period can extend to seven years.

Staying Informed About Tax Law Changes

Tax laws are not static. They can change annually due to new legislation, economic adjustments, or updates from the IRS.

- Reliable Sources: Regularly check the IRS website, reputable financial news outlets, or consult with a qualified tax professional to stay abreast of changes that could affect your tax situation.

- Impact on Planning: New laws might introduce new deductions or credits, alter income thresholds, or change contribution limits for retirement accounts. Being informed allows you to adapt your financial strategies accordingly.

In conclusion, while the official start of tax filing for 2024 (for the 2023 tax year) typically occurs in late January, responsible tax management is a year-round endeavor. By understanding the process, gathering your documents proactively, choosing the right filing method, and being mindful of deadlines, you can navigate tax season with confidence and ensure your financial health remains on solid ground.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.