In the intricate world of personal finance and business operations, few concepts are as central, yet frequently misunderstood, as the Form 1099. For millions of independent contractors, freelancers, gig economy participants, and small business owners across the United States, understanding what a 1099 is, why it exists, and how to properly manage the income it represents is not merely helpful—it’s absolutely essential for financial health and tax compliance. Far from being an obscure piece of IRS bureaucracy, the 1099 is the lynchpin for reporting non-employment income, impacting everything from your quarterly tax payments to your eligibility for deductions.

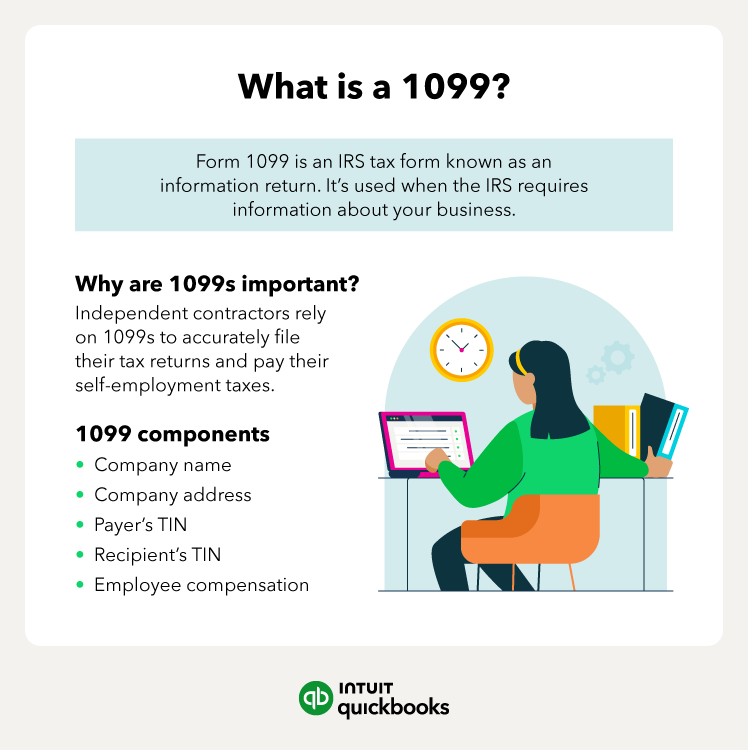

At its core, a 1099 is an information return issued by a payer to both the recipient of certain types of income and the Internal Revenue Service (IRS). Unlike a W-2 form, which reports wages paid to an employee, a 1099 reports payments made to non-employees for services rendered, dividends received, interest earned, or other miscellaneous income. This distinction is critical because it places the onus of tax withholding and payment squarely on the recipient, introducing a unique set of responsibilities and opportunities for financial planning. Navigating the world of 1099 income requires diligence, foresight, and a solid grasp of tax law, transforming what might seem like a simple income report into a foundational element of sound financial management for the self-employed.

Understanding the Essence of Form 1099

To truly grasp the significance of Form 1099, one must delve into its fundamental purpose and identify the key players involved in its issuance and receipt. This understanding forms the bedrock upon which effective financial planning for independent earners is built.

The Fundamental Purpose of 1099 Forms

The primary function of any 1099 form is to report income to the IRS that isn’t considered traditional wages from an employer. This ensures transparency and helps the IRS track income streams that might otherwise go unreported, thereby promoting tax compliance. For the individual receiving the 1099, it serves as an official record of income received, which must then be reported on their annual tax return. Without these forms, the informal economy and contract work would be much harder for tax authorities to monitor, leading to potential revenue loss for the government and an uneven playing field for taxpayers. The existence of 1099 forms helps maintain the integrity of the tax system by providing a clear paper trail for all parties.

Who Receives a 1099?

The recipients of 1099 forms are diverse, encompassing anyone who earns income outside of a traditional employer-employee relationship that meets specific thresholds. This includes:

- Independent Contractors and Freelancers: Writers, designers, consultants, programmers, photographers, and countless others who offer their services on a project or contract basis.

- Gig Economy Workers: Drivers for ride-sharing apps, food delivery personnel, task runners, and others who earn income through digital platforms.

- Small Business Owners: Sole proprietors, partnerships, and LLCs that provide services to other businesses.

- Recipients of Miscellaneous Income: Individuals receiving royalties, rents from rental properties (if managed by a third party), prizes and awards, or certain legal settlement payments.

- Investors: Those earning interest from bank accounts (1099-INT), dividends from investments (1099-DIV), or distributions from retirement accounts (1099-R).

If you perform work for a business and are not considered their employee, or if you receive other qualifying income, you are likely to receive one or more 1099 forms.

Who Issues a 1099?

The responsibility for issuing 1099 forms falls upon any individual or entity (including businesses, non-profits, and even individuals) that pays a non-employee at least $600 for services rendered in a calendar year, or meets other specific thresholds for various income types. For instance, a business that hires a freelance graphic designer for a project exceeding $600 must issue a 1099 to that designer. Similarly, banks issue 1099-INT for interest payments above $10, and investment firms issue 1099-DIV for dividend distributions. This requirement ensures that income paid out is properly documented at its source, creating a robust system for income reporting and verification.

Key Types of 1099 Forms You Should Know

While the term “1099” is often used generically, it refers to a family of forms, each designed to report specific types of non-employment income. Understanding the nuances of the most common 1099 forms is vital for accurate tax preparation.

Form 1099-NEC: Nonemployee Compensation

This form has become the cornerstone for reporting freelance and contract income. Reintroduced by the IRS for the 2020 tax year, Form 1099-NEC (Nonemployee Compensation) replaced Box 7 of Form 1099-MISC as the primary method for businesses to report payments of $600 or more to independent contractors, freelancers, and other non-employees for services performed in the course of trade or business. Its reintroduction streamlined reporting specifically for service-based income, making it easier for both payers and recipients to identify and report nonemployee compensation separately from other miscellaneous income types. If you’re a freelancer, consultant, or gig worker, this is likely the most common 1099 form you’ll encounter.

Form 1099-MISC: Miscellaneous Information

Prior to 2020, Form 1099-MISC (Miscellaneous Information) was the primary form for reporting nonemployee compensation. While 1099-NEC now handles most contractor payments, 1099-MISC remains relevant for reporting other types of miscellaneous income. This includes payments of at least $600 for:

- Rents (e.g., from rental properties managed by an agency, or if you receive rent payments for office space)

- Royalties (e.g., from books, music, or intellectual property)

- Prizes and awards

- Other income payments (such as those from certain legal settlements or medical and health care payments)

- Payments to an attorney (even if the total is less than $600)

It’s crucial to differentiate between 1099-NEC and 1099-MISC to ensure proper income classification on your tax returns.

Form 1099-K: Payment Card and Third Party Network Transactions

In an increasingly digital economy, Form 1099-K (Payment Card and Third Party Network Transactions) has gained significant prominence. This form is issued by third-party payment networks (e.g., PayPal, Stripe, Square, Venmo for business accounts) and credit card companies to report the gross amount of payments processed through their platforms. It’s particularly relevant for:

- Online Sellers: E-commerce businesses, Etsy shop owners, and anyone selling goods or services through online marketplaces.

- Gig Economy Platforms: Ride-sharing drivers, food delivery personnel, and other service providers whose payments are facilitated by apps.

- Small Businesses: Brick-and-mortar stores that accept credit card payments through a processing service.

Historically, 1099-K had high reporting thresholds. However, recent legislative changes (specifically for tax year 2023 onwards, with some adjustments) have aimed to lower these thresholds, meaning more individuals receiving payments through these platforms will receive a 1099-K, regardless of whether they consider themselves “in business.” This change significantly impacts many casual sellers and small-scale entrepreneurs, underscoring the need for careful tracking of all digital income.

Other Notable 1099 Forms

Beyond the big three, there’s a range of other specialized 1099 forms, each serving a particular purpose:

- Form 1099-INT: Reports interest income (e.g., from savings accounts, CDs, bonds).

- Form 1099-DIV: Reports dividends and distributions from stocks and mutual funds.

- Form 1099-R: Reports distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, etc.

- Form 1099-B: Reports proceeds from broker and barter exchange transactions (e.g., stock sales).

- Form 1099-G: Reports certain government payments, such as unemployment compensation or state tax refunds.

While less common for the typical freelancer, being aware of these forms highlights the comprehensive nature of 1099 reporting in the financial ecosystem.

Navigating Your Tax Obligations as a 1099 Worker

Receiving 1099 income comes with distinct tax responsibilities that differ significantly from those of a W-2 employee. Proactive planning is paramount to avoid surprises come tax season.

Self-Employment Tax Explained

One of the most significant distinctions for 1099 workers is the requirement to pay self-employment tax. Unlike employees, whose Social Security and Medicare taxes are split with their employer, independent contractors are responsible for the entire amount. Self-employment tax is essentially the combined employer and employee share of Social Security (12.4% on earnings up to a certain limit) and Medicare (2.9% on all earnings), totaling 15.3% on your net earnings from self-employment. This tax applies to your net earnings, which is your gross income minus your allowable business expenses. It’s a substantial percentage and often catches new freelancers off guard, emphasizing the need to factor it into financial planning.

Estimated Taxes: Paying as You Go

Since no employer is withholding taxes from their paychecks, 1099 workers are generally required to pay estimated taxes quarterly. The “pay-as-you-go” system ensures that taxpayers are remitting income tax and self-employment tax throughout the year, rather than facing a massive bill (and potential penalties) at year-end. These payments are typically due on April 15, June 15, September 15, and January 15 of the following year. Calculating estimated taxes involves projecting your annual income and deductible expenses, then factoring in your self-employment tax, income tax, and any credits. Failing to pay enough estimated tax throughout the year can result in penalties, making accurate quarterly payments a critical aspect of 1099 income management.

Deductions and Write-Offs: Maximizing Your Savings

The silver lining for 1099 workers is the ability to deduct legitimate business expenses, which can significantly reduce their taxable income and, consequently, their tax liability. Keeping meticulous records of all business-related expenditures is crucial. Common deductions include:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you can deduct a percentage of rent, utilities, insurance, and depreciation.

- Business Travel: Costs associated with business trips, including transportation, lodging, and meals (subject to limits).

- Professional Development: Expenses for courses, workshops, and certifications directly related to your business.

- Health Insurance Premiums: If you’re self-employed and not eligible for an employer-sponsored health plan, you can often deduct your premiums.

- Business Supplies and Equipment: Computers, software, stationery, and other tools necessary for your work.

- Marketing and Advertising: Website costs, business cards, online ads, and professional memberships.

- Professional Services: Fees paid to accountants, lawyers, or other consultants.

Maximizing these write-offs requires diligent record-keeping and a good understanding of what constitutes a “ordinary and necessary” business expense according to the IRS.

Best Practices for 1099 Income Management

Effective management of 1099 income goes beyond simply filing taxes; it involves strategic financial habits throughout the year.

Meticulous Record-Keeping

This cannot be stressed enough. Every dollar earned and every dollar spent on business-related activities should be tracked. This includes:

- Income Tracking: Maintain records of all invoices, payments received, and contracts.

- Expense Tracking: Keep receipts, bank statements, and credit card statements for all business expenses. Categorize these expenses logically.

- Mileage Logs: If you use your vehicle for business, a detailed mileage log is indispensable.

Digital tools, spreadsheets, or accounting software can streamline this process, making tax season far less stressful and ensuring you capture all eligible deductions.

Setting Aside Funds for Taxes

A common rule of thumb for 1099 workers is to set aside a significant portion of every payment received for taxes. While the exact percentage varies based on income level, deductions, and state taxes, earmarking anywhere from 25% to 35% (or even more for high earners) of your gross income specifically for estimated taxes is a prudent strategy. This money should ideally be kept in a separate, interest-bearing savings account, allowing it to grow slightly while remaining readily available for quarterly payments.

Seeking Professional Guidance

While self-preparation is an option, especially for simpler tax situations, consulting with a qualified tax professional (such as a CPA or Enrolled Agent) can be invaluable for 1099 workers. They can help:

- Accurately calculate estimated taxes.

- Identify all eligible deductions and credits.

- Ensure compliance with complex tax laws.

- Provide strategic advice for long-term financial planning.

- Represent you in case of an IRS audit.

The investment in professional guidance often pays for itself through optimized tax savings and peace of mind.

Utilizing Financial Tools

A plethora of financial tools is available to assist 1099 workers. Bookkeeping software (e.g., QuickBooks Self-Employed, FreshBooks, Wave), budgeting apps, and dedicated tax preparation platforms (e.g., TurboTax Self-Employed, H&R Block Premium) can automate expense tracking, categorize transactions, generate financial reports, and even facilitate estimated tax payments. Choosing the right tools can save countless hours and reduce the likelihood of errors.

Common Pitfalls and How to Avoid Them

Even with the best intentions, 1099 workers and the businesses that engage them can fall into common traps. Awareness is the first step to avoidance.

Misclassifying Employees vs. Independent Contractors

For businesses that hire workers, correctly classifying someone as an independent contractor versus an employee is paramount. The IRS has strict guidelines and tests (e.g., behavioral control, financial control, type of relationship) to determine worker status. Misclassification can lead to significant penalties, back taxes, and legal issues for the business, as well as depriving workers of employee benefits and protections.

Ignoring Estimated Tax Deadlines

One of the most frequent mistakes made by 1099 workers is failing to make timely and sufficient estimated tax payments. This can result in underpayment penalties from the IRS. It’s crucial to mark these deadlines on your calendar, calculate your payments accurately, and remit them promptly. Setting up automated reminders or using tax software that helps with these calculations can mitigate this risk.

Forgetting Deductible Expenses

Without diligent record-keeping, it’s easy to overlook eligible business deductions. Every forgotten receipt or untracked expense means paying more in taxes than legally required. Make it a habit to record expenses as they occur, rather than trying to reconstruct them at year-end.

Not Reconciling 1099 Forms with Records

When you receive a 1099-NEC or 1099-K, it’s essential to compare the reported income with your own records. Discrepancies can occur, and it’s your responsibility to reconcile them. If a payer has overstated your income on a 1099, you must contact them to request a corrected form. Reporting incorrect income can lead to IRS inquiries and complications.

Understanding “what’s 1099” is far more than knowing a tax form number; it’s about embracing a distinct financial paradigm that comes with self-employment. For the ever-growing population of freelancers, independent contractors, and small business owners, the 1099 forms represent not just income, but also the gateway to unique tax obligations, strategic deductions, and the profound responsibility of managing one’s own financial future. By proactively understanding these forms, meticulously managing records, setting aside funds for taxes, and seeking expert guidance when needed, 1099 workers can navigate the complexities with confidence, ensuring compliance and optimizing their financial outcomes. The 1099 isn’t just a document; it’s a testament to financial independence, demanding a thoughtful and informed approach to thrive in the modern economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.