Tax season can often feel like a daunting annual pilgrimage into a labyrinth of forms, figures, and financial jargon. For many, the sheer volume of required documentation and the underlying complexity can be overwhelming, leading to procrastination or even costly errors. Yet, at its core, tax preparation is a structured process of gathering specific information and submitting it to the relevant authorities. Understanding what you need is the first, and arguably most crucial, step towards a smooth, accurate, and potentially optimized tax filing experience. This guide aims to demystify the process, providing a comprehensive checklist of documents, details, and strategic considerations essential for every taxpayer.

I. Foundational Personal Information: The Basics of Your Identity

Before delving into income or deductions, the Internal Revenue Service (IRS) and state tax authorities need to know who is filing and who is covered by the return. This foundational data forms the bedrock of your tax submission.

Your Identity and Contact Details

At a minimum, you’ll need the following for yourself and your spouse (if filing jointly):

- Full Legal Name: As it appears on your Social Security card.

- Social Security Number (SSN): This is your unique taxpayer identification number. Accuracy is paramount here; a single digit error can cause significant delays.

- Date of Birth: Essential for age-related credits or deductions.

- Current Mailing Address: Where the IRS will send any correspondence or your refund check (if applicable).

- Occupation: A simple descriptor of your primary job.

- Phone Number and Email Address: While not always mandatory for the physical return, these are often requested by tax software or preparers for communication.

Dependents’ Information

If you are claiming dependents, whether they are children, relatives, or other qualifying individuals, you’ll need similar basic information for each:

- Full Legal Name: Again, as it appears on their Social Security card.

- Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN): This is non-negotiable for claiming dependents.

- Date of Birth: Critical for determining eligibility for various child-related tax benefits.

- Relationship to You: E.g., son, daughter, grandchild.

- Number of Months Lived With You: This helps establish residency requirements for certain credits.

Correctly identifying and including dependent information can unlock valuable tax credits, such as the Child Tax Credit, Credit for Other Dependents, or the Earned Income Tax Credit, significantly reducing your overall tax liability.

Bank Account for Refunds or Payments

While not a document in itself, having your bank account details readily available is essential for modern tax filing.

- Bank Name: The financial institution holding your account.

- Account Number: Your specific account identifier.

- Routing Number: A nine-digit code that identifies your bank.

Providing these details enables direct deposit of your refund, which is typically much faster and more secure than waiting for a paper check. Conversely, if you owe taxes, direct debit allows for seamless electronic payment from your account.

II. Income Documentation: Tracking Your Earnings

The cornerstone of any tax return is a complete and accurate reporting of all your income sources. The IRS requires various forms from employers, financial institutions, and other payers to ensure transparency and accountability. Understanding which forms apply to you is critical.

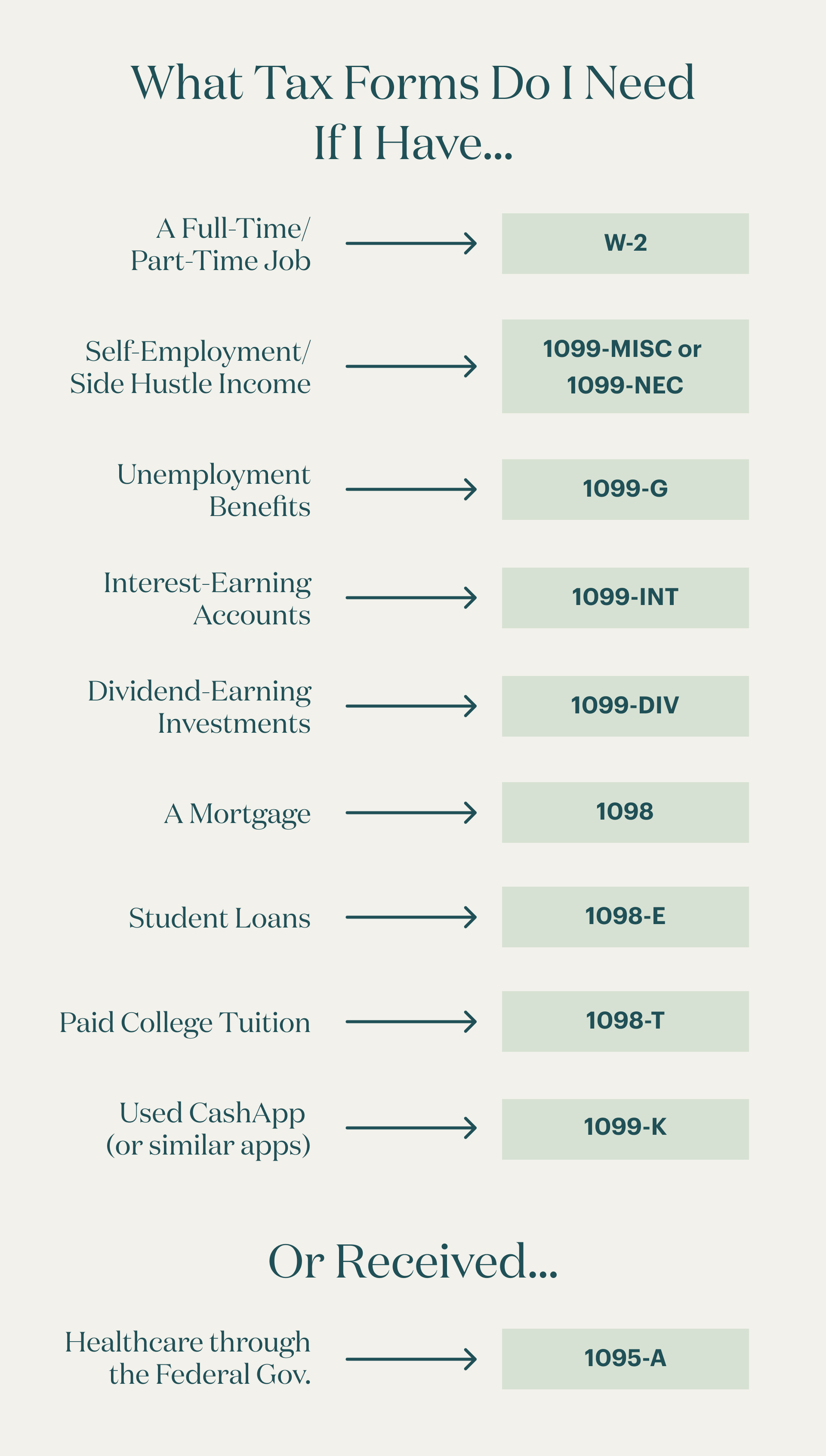

Wage Earners: W-2 Forms

If you are employed by a company, your primary income document will be Form W-2, Wage and Tax Statement. You should receive a W-2 from each employer you worked for during the tax year, typically by January 31st of the following year. This form summarizes:

- Your total wages, salaries, and tips.

- The federal income tax withheld from your paychecks.

- State and local taxes withheld.

- Contributions to retirement plans (e.g., 401(k)).

- Other benefits, such as health insurance premiums paid pre-tax.

Ensure you have a W-2 for every job you held throughout the year. If you haven’t received one by early February, contact your former employer directly.

Freelancers and Independent Contractors: 1099 Forms

For those who work for themselves, engage in contract work, or earn income from various gigs, Form 1099 is your equivalent to a W-2. There are several variations:

- Form 1099-NEC (Nonemployee Compensation): This is the most common for freelancers and independent contractors who received payments of $600 or more from a single payer.

- Form 1099-MISC (Miscellaneous Information): Used for various types of income not covered by other 1099 forms, such as rental income, prizes, or royalty payments, when those amounts exceed certain thresholds.

- Form 1099-K (Payment Card and Third Party Network Transactions): If you received payments through third-party payment networks (e.g., PayPal, Venmo, Stripe) for goods or services, you might receive this form, particularly if your transactions exceed specific thresholds (though the threshold for 2023 was higher than originally planned due to legislative delays).

It’s important to note that even if you don’t receive a 1099 form for all your self-employment income (e.g., from smaller clients or cash payments), all income must be reported to the IRS. Maintaining meticulous records of invoices and payments received is paramount for self-employed individuals.

Investment Income: 1099-B, 1099-DIV, 1099-INT

If you have investments, your brokerage firm or financial institution will issue specific 1099 forms:

- Form 1099-B (Proceeds From Broker and Barter Exchange Transactions): Reports gains or losses from the sale of stocks, bonds, or other securities.

- Form 1099-DIV (Dividends and Distributions): Details ordinary dividends, qualified dividends, and capital gain distributions from stocks and mutual funds.

- Form 1099-INT (Interest Income): Reports interest earned from savings accounts, CDs, money market accounts, and some bonds.

These forms are crucial for calculating your capital gains/losses and reporting other investment income accurately.

Retirement Income: 1099-R

If you received distributions from pensions, annuities, IRAs, or other retirement plans, you’ll receive Form 1099-R. This form indicates the total amount distributed and the taxable portion of that distribution.

Other Income Sources

Don’t overlook other potential income streams:

- Social Security Benefits (Form SSA-1099): If a portion of your Social Security benefits is taxable based on your overall income.

- Unemployment Compensation (Form 1099-G): Reports unemployment benefits received.

- Rental Income and Expenses: While not necessarily a 1099 form, you’ll need detailed records of all rental income received and expenses paid for any properties you rent out.

- Gambling Winnings (Form W2-G): If your winnings exceed certain thresholds, the payer will issue this form.

III. Deductions and Credits: Optimizing Your Tax Bill

Once all income is accounted for, the next step is to explore opportunities to reduce your taxable income or your tax liability directly through deductions and credits. This is where strategic tax planning can significantly impact your financial outcome.

Understanding Deductions vs. Credits

- Deductions: Reduce your taxable income. For example, a $1,000 deduction for someone in a 24% tax bracket saves them $240 in taxes.

- Credits: Directly reduce the amount of tax you owe, dollar for dollar. A $1,000 tax credit reduces your tax bill by $1,000. Some credits are refundable, meaning you could get money back even if you owe no tax.

Common Deductions and the Choice Between Standard vs. Itemized

Most taxpayers will choose between taking the standard deduction or itemizing their deductions.

- Standard Deduction: A fixed dollar amount that reduces your taxable income, varying based on your filing status (single, married filing jointly, head of household). For many, this is the simplest and most advantageous option.

- Itemized Deductions: A collection of specific eligible expenses that you can subtract from your adjusted gross income (AGI). You’ll need records for:

- Medical and Dental Expenses: Only the amount exceeding 7.5% of your AGI is deductible. Keep receipts for doctor visits, prescriptions, and health insurance premiums paid out-of-pocket.

- State and Local Taxes (SALT): This includes income, sales, and property taxes, but is capped at $10,000 per household.

- Home Mortgage Interest (Form 1098): Reports the interest paid on your home mortgage.

- Charitable Contributions: Receipts for cash donations and appraisals for non-cash donations are crucial.

- Casualty and Theft Losses: Limited to losses from federally declared disaster areas.

You should itemize only if your total itemized deductions exceed the standard deduction amount for your filing status.

Education-Related Expenses and Credits

If you or your dependents are pursuing higher education, several tax breaks might apply:

- Form 1098-T (Tuition Statement): Issued by educational institutions, detailing tuition payments and scholarships.

- American Opportunity Tax Credit (AOTC): A partially refundable credit for undergraduate education expenses.

- Lifetime Learning Credit (LLC): A non-refundable credit for undergraduate, graduate, or professional course expenses.

- Student Loan Interest Deduction: You can deduct up to $2,500 in student loan interest paid (Form 1098-E).

Retirement Contributions

Contributions to certain retirement accounts can be tax-deductible:

- Traditional IRA Contributions: You’ll need records of any contributions made, as these can be deductible, lowering your taxable income.

- Self-Employed Retirement Plans (SEP IRA, SIMPLE IRA, Solo 401(k)): Documentation of contributions to these plans is essential for self-employed individuals.

Child and Dependent Care Expenses

If you paid for childcare while you (and your spouse, if filing jointly) worked or looked for work, you might qualify for the Child and Dependent Care Credit. You’ll need:

- Name, address, and SSN/EIN of the care provider.

- Total amount paid to each provider.

IV. Tax Payments and Prior Year Information

Beyond current year income and deductions, your tax history and any payments already made during the tax year play a significant role in determining your final tax liability.

Prior Year Tax Information

Having a copy of your previous year’s tax return (Form 1040) is incredibly useful, if not outright necessary, for several reasons:

- Adjusted Gross Income (AGI): Your prior year’s AGI is often required for identity verification when e-filing.

- Carryovers: Information on capital loss carryovers, passive activity loss carryovers, or other deductions/credits that couldn’t be fully used in the prior year may be relevant.

- Basis Information: For certain investments or assets, the previous year’s return may hold clues about your cost basis, which is essential for calculating current year gains or losses.

- Reference: It serves as a handy guide for remembering deductions or income sources you’ve reported in the past.

Estimated Tax Payments Made

If you are self-employed, have significant investment income, or other income not subject to withholding, you are likely required to make estimated tax payments throughout the year (Form 1040-ES). You’ll need:

- Dates and amounts of all estimated tax payments made: This includes payments sent directly to the IRS, payments made with an extension request, or credits from an overpayment on your prior year’s return.

- State estimated tax payments: Don’t forget payments made to your state tax authority.

Failing to report these payments accurately can lead to an incorrect calculation of taxes owed or even penalties for underpayment.

W-4 Form Adjustments

While not a direct tax document to be submitted, understanding your W-4 Form history (Employee’s Withholding Certificate) can provide insights into how much federal income tax was withheld from your paychecks. If you notice a significant discrepancy between what you owed last year and what was withheld this year, reviewing your W-4 (and adjusting it for the upcoming tax year) is a wise financial move to avoid large refunds (which means you’ve given the government an interest-free loan) or, worse, a hefty tax bill.

V. Tools and Best Practices for Tax Preparation

Gathering all these documents can be a substantial undertaking. However, employing good organizational habits and leveraging available tools can transform the process from a dreaded chore into a manageable task.

Organizing Your Documents

- Dedicated Folder/Digital File: As soon as a relevant tax document arrives (e.g., W-2, 1099, 1098), immediately place it in a designated physical folder or upload it to a specific digital folder on your computer or cloud storage.

- Categorization: Consider using sub-folders or dividers for income, deductions, and personal information.

- Ongoing Record Keeping: Don’t wait until January. Throughout the year, keep receipts for deductible expenses (medical, charitable, business) and maintain clear records of any non-W2 income or significant financial transactions. A simple spreadsheet can be invaluable for tracking expenses.

Utilizing Tax Software or Professional Help

Deciding between DIY tax software and a professional tax preparer depends on your financial situation and comfort level.

- Tax Software (e.g., TurboTax, H&R Block, FreeTaxUSA): Ideal for most taxpayers with straightforward returns. These programs guide you step-by-step, flagging potential deductions and credits, and often allow for e-filing. They typically store your prior year’s data, making subsequent filings easier. Be prepared to input all your gathered documents accurately.

- Professional Tax Preparer (e.g., CPA, Enrolled Agent): Recommended for individuals with complex tax situations, such as significant self-employment income, rental properties, stock options, foreign income, or those who have experienced major life changes (marriage, divorce, new business). A professional can offer personalized advice, ensure compliance, and potentially identify deductions you might have overlooked. They will require all your documents to compile the return.

The Importance of Record Keeping

The IRS generally recommends keeping tax records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. For certain items, like property basis or retirement contributions, you may need to keep records indefinitely. This includes all W-2s, 1099s, receipts for deductions, bank statements, and a copy of your filed tax return. In the event of an audit, these records are your primary defense.

In conclusion, “what do I need for my taxes?” boils down to a comprehensive collection of personal details, income statements, and expense records. By understanding these requirements and adopting proactive organizational habits, you can approach tax season with confidence, ensuring accuracy, minimizing stress, and potentially optimizing your financial outcome.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.