The thought of filing taxes can often evoke a mix of confusion and apprehension. For many, the annual ritual seems a universal requirement, a financial rite of passage that everyone must undertake regardless of their earnings. However, the reality is more nuanced. Not everyone is legally obligated to file a federal income tax return. The question of “how much money to file taxes” isn’t just about a fixed dollar amount; it’s about understanding specific income thresholds, your filing status, age, and a variety of other factors that determine your tax responsibilities.

Navigating the complexities of the U.S. tax code can be daunting, but clarifying your filing obligation is the crucial first step in managing your financial health and avoiding potential penalties. This article will demystify these requirements, helping you determine whether you need to file a tax return and why, even if not strictly required, it might still be in your best financial interest to do so. We’ll explore the critical income thresholds, the impact of various life circumstances, and the often-overlooked benefits of proactive tax engagement, ensuring you are well-equipped to make informed decisions about your tax obligations.

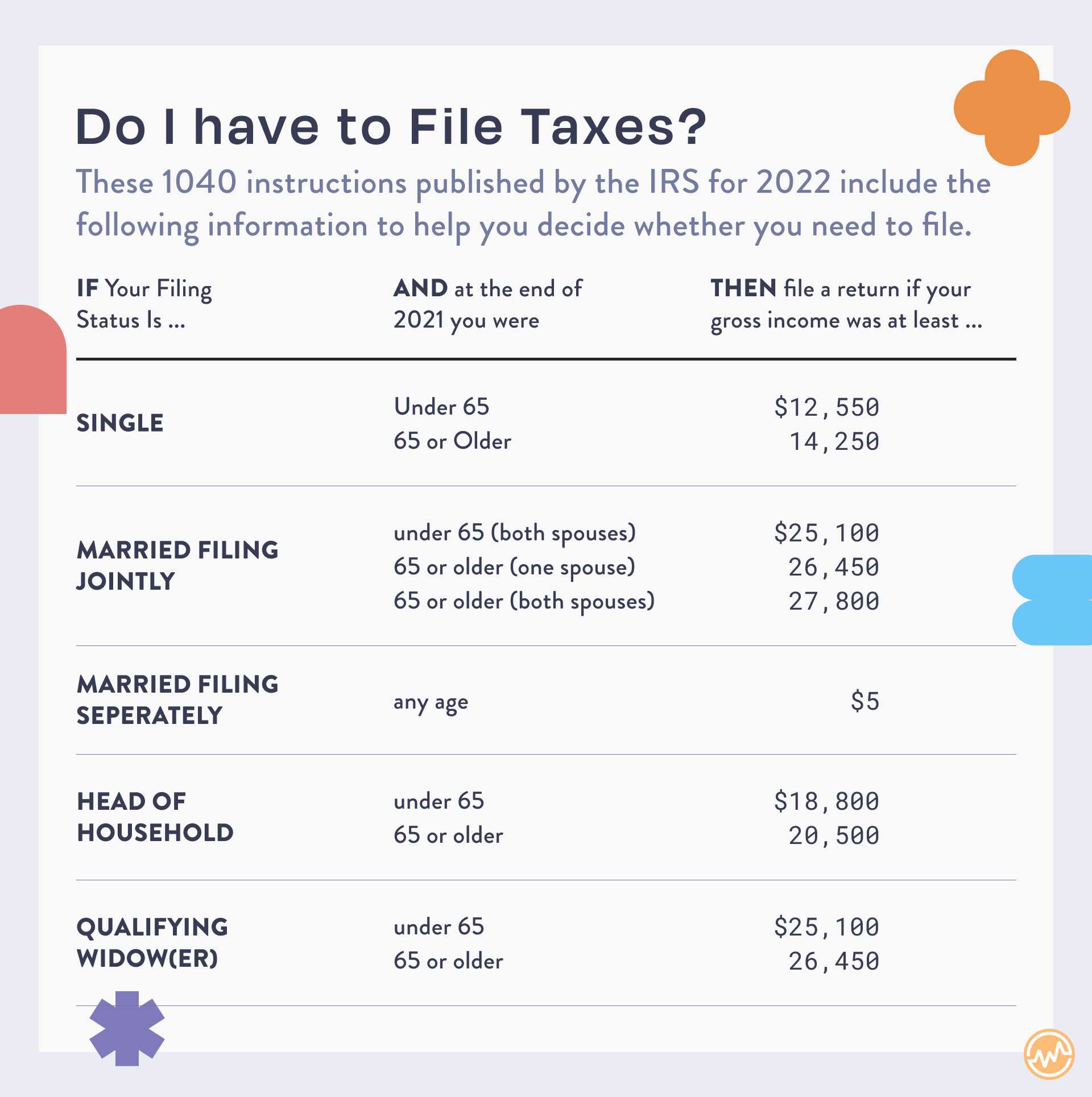

The Basics: Who Needs to File a Tax Return?

The Internal Revenue Service (IRS) sets specific income thresholds that determine whether an individual must file a federal income tax return. These thresholds are not static; they change annually due to inflation adjustments and are influenced by several personal factors, primarily your gross income, filing status, and age. Understanding these core components is fundamental to assessing your filing obligation.

Understanding Gross Income

Gross income is the total of all income you receive from all sources that is not exempt from tax. This includes wages, salaries, tips, interest, dividends, rental income, business income, and even certain types of unemployment compensation or gambling winnings. It’s crucial to distinguish gross income from adjusted gross income (AGI), which is gross income minus certain deductions. For filing requirement purposes, the IRS primarily looks at your gross income. If your gross income exceeds a certain threshold, you are generally required to file, regardless of whether you ultimately owe taxes.

The Standard Deduction and Filing Thresholds

The filing thresholds are directly linked to the standard deduction amount for your specific filing status, plus any additional standard deduction for age or blindness. Essentially, if your gross income is less than your standard deduction amount, you might not be required to file.

For the 2023 tax year (filed in 2024), here are some simplified federal filing thresholds for most taxpayers (these are examples and subject to change annually; always consult official IRS publications):

- Single: $13,850

- Married Filing Separately: $5

- Married Filing Jointly: $27,700

- Head of Household: $20,800

- Qualifying Widow(er): $27,700

These thresholds increase if you are age 65 or older or blind. For example, a single individual age 65 or older might have a higher filing threshold. The logic is that if your income is below the standard deduction, your taxable income would likely be zero, meaning no tax liability. However, there are critical exceptions.

Special Circumstances Requiring a Filing

Even if your gross income falls below the general filing thresholds, certain situations mandate that you file a tax return. These exceptions are important to recognize:

- Self-Employment Income: If your net earnings from self-employment were $400 or more, you must file a tax return to pay self-employment taxes (Social Security and Medicare taxes). This applies even if you have a full-time job and earn only a small amount from a side gig.

- Special Taxes Due: You must file if you owe any special taxes, such as alternative minimum tax, household employment taxes, or uncollected Social Security and Medicare tax on tips.

- Advance Premium Tax Credit: If you received advance payments of the premium tax credit through the Health Insurance Marketplace, you must file a return to reconcile those payments with the actual credit you qualify for.

- Net Investment Income Tax: Certain high-income individuals may owe the Net Investment Income Tax, requiring a filing.

- Foreign Earned Income: U.S. citizens or resident aliens living abroad may have specific filing requirements, even if they exclude foreign earned income.

Ignoring these specific conditions can lead to penalties, underscoring the importance of reviewing all applicable IRS guidelines beyond just the general income thresholds.

Beyond the Thresholds: When Filing is Still a Good Idea

While meeting a filing requirement is a legal obligation, there are numerous scenarios where filing a tax return, even when not strictly mandated, can lead to significant financial benefits. Proactive filing can unlock refunds and credits that might otherwise go unclaimed, putting money back into your pocket.

Claiming Tax Refunds and Credits

Perhaps the most compelling reason to file a tax return when not required is to receive a refund. Many individuals have taxes withheld from their paychecks throughout the year (e.g., federal income tax, Social Security, Medicare). If the amount withheld exceeds the amount of tax you actually owe, the IRS will issue you a refund – but only if you file a return. Common scenarios include:

- Over-withholding: Your employer may have withheld more federal income tax than necessary based on your W-4 form.

- Refundable Tax Credits: These are credits that can result in a refund even if you owe no tax or if the credit amount is more than your tax liability. Key refundable credits include:

- Earned Income Tax Credit (EITC): A substantial credit for low-to-moderate income working individuals and families. The maximum credit can be thousands of dollars, making it a critical financial lifeline.

- Child Tax Credit (CTC): A credit for qualifying children, a portion of which may be refundable.

- American Opportunity Tax Credit (AOTC): A credit for educational expenses, up to 40% of which is refundable.

- Premium Tax Credit (PTC): Assists eligible individuals and families with low or moderate income to afford health insurance purchased through the Health Insurance Marketplace.

Without filing a return, these valuable credits and any overpaid taxes remain with the government.

Self-Employment Income

As mentioned, if you have net earnings from self-employment of $400 or more, you must file to pay self-employment taxes. However, even with lower net earnings, or if you had significant business expenses that resulted in a loss, filing can be beneficial. Filing allows you to:

- Report Income and Expenses: Establish an official record of your business activities, which can be useful for future loans or demonstrating a legitimate business.

- Claim Deductions: Reduce your overall tax liability by deducting legitimate business expenses, even if they result in a net loss that can be carried forward to future years.

- Contribute to Retirement: Self-employment income is essential for contributing to self-employed retirement accounts like a SEP IRA or Solo 401(k), which require reported income.

Premium Tax Credits and Health Coverage

If you or a family member purchased health insurance through the Health Insurance Marketplace (often healthcare.gov or a state equivalent) and received advance payments of the premium tax credit, you must file a federal income tax return. This is to reconcile the advance payments you received with the actual premium tax credit you are entitled to based on your final income for the year. Failing to file could lead to issues with future subsidies and potential repayment of advance credits if your income was higher than estimated. Even if you received no advance payments but qualify for the credit, filing allows you to claim it.

Navigating Different Income Types and Filing Statuses

The complexity of tax filing requirements grows when considering various income sources and personal circumstances. Your marital status, whether you support dependents, and the nature of your income (earned vs. unearned) all play a significant role in determining your filing obligation and potential tax liability.

Impact of Filing Status (Single, Married Filing Jointly, etc.)

Your filing status is a critical determinant of your standard deduction amount, tax rates, and eligibility for certain credits. The five main filing statuses are:

- Single: Unmarried individuals.

- Married Filing Jointly: Married couples who choose to file one joint return.

- Married Filing Separately: Married couples who choose to file individual returns.

- Head of Household: Unmarried individuals who pay more than half the cost of keeping up a home for a qualifying person.

- Qualifying Widow(er) with Dependent Child: For a surviving spouse for up to two years after the death of a spouse, if they have a dependent child.

Each status has a different standard deduction and income threshold. For instance, the threshold for “Married Filing Separately” is generally very low ($5 for 2023), designed to ensure that spouses who choose to file separately still report their income, whereas “Married Filing Jointly” has the highest threshold. It’s vital to select the correct filing status as it can significantly impact your tax liability and whether you need to file.

Dependent Status and Your Filing Obligation

Being claimed as a dependent on another person’s tax return, typically a parent, does not exempt you from your own filing requirements. Dependents generally must file if their gross income (earned and unearned combined) exceeds certain thresholds, which are often lower than for non-dependents. For instance:

- Earned Income: If a dependent’s earned income (wages, salary) exceeds the standard deduction for a dependent, they must file. This deduction is often the greater of $1,250 or their earned income plus $400 (up to the regular standard deduction).

- Unearned Income: If a dependent’s unearned income (interest, dividends) exceeds $1,250 (for 2023), they must file.

- Combined Income: If their gross income (earned plus unearned) exceeds the larger of $1,250 or their earned income plus $400 (up to the regular standard deduction), they must file.

Even if not required, a dependent should file if they had taxes withheld from their pay to claim a refund.

Investment Income and Other Unearned Income

Beyond wages, various forms of unearned income can trigger a filing requirement. This includes:

- Taxable Interest and Dividends: If you receive more than a certain amount (e.g., $1,500 in 2023 from certain sources), the payer may send you a Form 1099-INT or 1099-DIV, and this income counts towards your gross income.

- Capital Gains: Proceeds from selling investments like stocks, bonds, or real estate generally count as income.

- Rental Income: Income from renting out property.

- Social Security Benefits: A portion of Social Security benefits may be taxable if your combined income (AGI + nontaxable interest + half of your Social Security benefits) exceeds certain base amounts ($25,000 for single, $32,000 for married filing jointly).

- Gambling Winnings: Even small amounts of gambling winnings may be taxable and require reporting, often triggering a filing obligation.

It’s critical to track all sources of income, as the combined total determines whether you cross the filing threshold. Tax forms like 1099-MISC, 1099-NEC, 1099-B, and 1099-G report various types of unearned income, serving as indicators that you might have a filing responsibility.

The Consequences of Not Filing (or Filing Incorrectly)

Ignoring your tax obligations can lead to a cascade of negative financial repercussions. The IRS has robust mechanisms for identifying non-filers and inaccurate returns, and the penalties for non-compliance can far outweigh the initial effort of filing correctly and on time.

Penalties for Failure to File and Pay

The IRS imposes two primary penalties for late or incorrect tax returns:

- Failure to File Penalty: This is typically 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid taxes. If your return is more than 60 days late, the minimum penalty is $485 (for 2023), or 100% of the tax due, whichever is smaller. This penalty is generally more severe than the failure to pay penalty.

- Failure to Pay Penalty: This is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25%. This penalty applies even if you file on time but don’t pay.

Both penalties can accrue simultaneously, potentially leading to a significant increase in your tax bill. Additionally, interest is charged on underpayments and unpaid penalties, compounding the financial burden. The IRS can also pursue more severe actions, such as placing a lien on your property or levying your bank accounts or wages, if tax debts become substantial and are ignored.

Statute of Limitations and Unfiled Returns

The statute of limitations generally dictates the time frame within which the IRS can assess additional tax, or you can claim a refund. For most returns, it’s three years from the date you filed the original return or the due date of the return, whichever is later. However, this period does not begin if you don’t file a return.

- No Statute of Limitations for Non-Filers: If you never file a tax return, there is no statute of limitations for the IRS to assess tax. This means the IRS can pursue taxes owed for unfiled returns indefinitely.

- Extended for Substantial Understatement: If you substantially understate your income (by more than 25%), the statute of limitations extends to six years.

- Fraud: In cases of fraud, there is no statute of limitations.

This “forever” consequence for non-filers is a powerful incentive to get caught up on any unfiled returns. The IRS offers various programs for taxpayers who voluntarily come forward to file past-due returns, often providing more lenient terms than if they had to initiate collection actions.

The Importance of Accurate Record-Keeping

Accurate record-keeping is the bedrock of responsible tax filing. Without proper documentation, you risk:

- Missing Deductions and Credits: You might overlook legitimate deductions or credits you’re entitled to, leading to a higher tax bill than necessary.

- Errors on Your Return: Inaccuracies can lead to delays, audits, or penalties.

- Difficulty During an Audit: If selected for an audit, the burden of proof is on you to substantiate all income, deductions, and credits claimed. Without detailed records, you could face disallowance of claims and additional tax assessments.

Maintain organized records of income (W-2s, 1099s), expenses (receipts, mileage logs for business), investment statements, and any other relevant financial documents for at least three to seven years, depending on the type of record and potential for audit. Digital records are increasingly acceptable and can simplify storage and retrieval.

Practical Steps and Resources for Tax Filing

Once you’ve determined your filing obligation, the next step is to prepare and submit your return. Fortunately, a wealth of resources is available to simplify this process, whether you prefer a do-it-yourself approach or professional assistance.

Choosing Your Filing Method (Software, Professional, Free Options)

The method you choose for filing depends on the complexity of your tax situation and your comfort level with financial software.

- Tax Software: Companies like TurboTax, H&R Block, and TaxAct offer user-friendly software (both desktop and online versions) that guide you through the process, perform calculations, and help identify deductions. They come in various tiers, from free for simple returns to paid versions for more complex scenarios (e.g., self-employment, investments).

- Professional Tax Preparers: For complex situations, significant life changes (marriage, divorce, starting a business), or simply peace of mind, a certified public accountant (CPA) or enrolled agent (EA) can be invaluable. They offer expert advice, ensure accuracy, and can represent you before the IRS if needed.

- IRS Free File Program: If your adjusted gross income (AGI) is below a certain threshold (e.g., $79,000 for 2023), you may qualify for the IRS Free File program, which offers free tax preparation and e-filing through various software providers. This is an excellent option for many taxpayers.

- Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE): These IRS-sponsored programs offer free tax help to qualified individuals, including low-to-moderate-income people, persons with disabilities, the elderly, and those with limited English proficiency. Certified volunteers provide basic income tax return preparation.

Key Documents You’ll Need

Regardless of your chosen filing method, gathering the necessary documents beforehand will streamline the process:

- Proof of Identity: Social Security numbers (SSN) or Individual Taxpayer Identification Numbers (ITIN) for yourself, your spouse, and any dependents.

- Income Statements: W-2s (wages), 1099s (interest, dividends, self-employment, pensions, unemployment, etc.), K-1s (from partnerships, S-corporations, trusts).

- Deduction and Credit Documentation: Statements for student loan interest (Form 1098-E), mortgage interest (Form 1098), property taxes, medical expenses, charitable contributions, childcare expenses, education expenses (Form 1098-T), and health insurance premiums/Form 1095-A (for Marketplace plans).

- Last Year’s Tax Return: Helpful for referencing prior year information.

- Bank Account Information: For direct deposit of any refund.

Organizing these documents in advance saves time and reduces stress during tax season.

Proactive Tax Planning Throughout the Year

Tax filing shouldn’t be a once-a-year scramble. Effective tax planning is an ongoing process that can significantly impact your financial well-being.

- Adjust Withholding (W-4): Review your W-4 form annually, especially after major life changes (marriage, new baby, new job), to ensure the correct amount of tax is withheld from your paycheck. This helps avoid a large tax bill or an excessively large refund (which means you’ve given the government an interest-free loan).

- Estimate Self-Employment Tax: If self-employed, make estimated tax payments quarterly to cover your income and self-employment taxes, avoiding penalties.

- Maximize Deductions and Credits: Keep meticulous records of all potential deductions and credits. Consider contributing to tax-advantaged accounts like 401(k)s, IRAs, or HSAs, which reduce your taxable income.

- Stay Informed: Tax laws change. Staying updated through reliable sources (like the IRS website, reputable financial news, or your tax professional) can help you adapt your planning.

By integrating tax considerations into your year-round financial strategy, you can minimize surprises, optimize your tax position, and gain greater control over your financial future.

Understanding “how much money to file taxes” is more than just knowing a dollar amount; it’s about comprehending your specific situation within the broader tax landscape. While income thresholds provide a baseline, factors like filing status, age, type of income, and potential eligibility for refundable credits often dictate your true obligation and financial opportunity. Even if not legally required to file, doing so can unlock valuable refunds and credits, putting money back into your pocket. Conversely, neglecting a filing requirement can lead to significant penalties, interest, and long-term issues with the IRS. By staying informed, maintaining accurate records, and leveraging available resources, you can navigate your tax responsibilities with confidence, ensuring compliance and optimizing your financial outcomes. Proactive tax planning is not merely a chore but a crucial component of sound personal financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.