The phrase “avoiding taxes” often conjures images of illicit schemes and offshore accounts. However, in the realm of personal and business finance, “tax avoidance” refers to the entirely legal and ethical practice of minimizing your tax liability through legitimate means, utilizing the deductions, credits, and strategies permitted by tax law. This is distinct from “tax evasion,” which is illegal and carries severe penalties. Understanding how to legally reduce your tax burden is a critical component of sound financial planning, allowing individuals and businesses to retain more of their hard-earned money and reinvest it into their financial future.

In a complex financial landscape, navigating tax codes can seem daunting. Yet, with a proactive approach and a clear understanding of the opportunities available, you can significantly optimize your tax position. This comprehensive guide will explore various strategies, from fundamental principles to advanced techniques, empowering you to make informed decisions that benefit your bottom line. Our goal is to demystify the process and provide actionable insights for individuals, families, and business owners striving for greater financial efficiency.

Understanding the Fundamentals of Tax Reduction

Before diving into specific strategies, it’s essential to establish a foundational understanding of what tax reduction entails and the core concepts that drive it. This clarity will serve as your compass in the intricate world of taxation.

Distinguishing Between Tax Avoidance and Tax Evasion

The first and most crucial distinction to make is between tax avoidance and tax evasion.

Tax avoidance involves using legal methods to reduce your tax liability. This includes taking advantage of legitimate deductions, credits, exemptions, and tax-advantaged accounts or structures explicitly allowed by tax laws. It’s about structuring your financial affairs in the most tax-efficient way possible. For instance, contributing to a 401(k) or IRA to lower your taxable income is a form of tax avoidance.

Tax evasion, on the other hand, is the illegal act of deliberately misrepresenting your financial situation to avoid paying taxes. This includes hiding income, falsely claiming deductions, or fabricating expenses. Tax evasion is a criminal offense with severe consequences, including hefty fines, imprisonment, and damage to one’s reputation. Our focus, unequivocally, is on legal and ethical tax avoidance.

The Importance of Proactive Tax Planning

Many people approach taxes as an annual chore, scrambling to gather documents just before the filing deadline. However, effective tax reduction is a year-round activity. Proactive tax planning involves making financial decisions throughout the year with an eye toward their tax implications. This means not just reacting to your tax situation but actively shaping it.

By planning ahead, you can identify opportunities to defer income, accelerate deductions, choose optimal investment strategies, and structure your finances in a way that aligns with your long-term goals while minimizing your tax burden. Waiting until April 14th to think about your taxes means you’ve likely missed numerous opportunities to save. A proactive approach allows for strategic adjustments that can yield significant savings over time.

Key Tax Concepts: Deductions, Credits, and Exemptions

To effectively reduce your taxes, you must grasp the fundamental mechanisms through which this is achieved:

- Deductions: These reduce your taxable income. For every dollar you deduct, your taxable income decreases by a dollar, meaning you pay tax on a smaller amount. Common deductions include contributions to traditional IRAs, student loan interest, and health savings account (HSA) contributions. You can either take the standard deduction (a fixed amount determined by the IRS based on your filing status) or itemize your deductions (listing specific eligible expenses like mortgage interest, state and local taxes, and charitable contributions). You choose whichever results in a lower taxable income.

- Credits: These directly reduce your tax liability dollar for dollar. A $1,000 tax credit reduces the amount of tax you owe by $1,000. Credits are generally more valuable than deductions because they subtract directly from your tax bill, rather than just reducing the income on which your tax is calculated. Examples include the Child Tax Credit, Earned Income Tax Credit, and education credits. Some credits are even refundable, meaning if the credit reduces your tax liability below zero, you can receive the difference back as a refund.

- Exemptions: Historically, exemptions reduced your taxable income for yourself, your spouse, and your dependents. While personal exemptions were effectively eliminated for federal income tax purposes from 2018 through 2025 due to the Tax Cuts and Jobs Act (TCJA), the underlying concept of reducing taxable income for certain reasons remains. Many states still have exemptions, and the spirit of providing relief for individuals and families is now often captured through expanded standard deductions and various tax credits.

Understanding these concepts is paramount. They are the tools you will use to carve out a more favorable tax position.

Strategies for Individuals to Minimize Taxes

For most individuals, tax planning starts with optimizing personal financial choices. A significant portion of tax savings comes from utilizing retirement accounts, health savings accounts, and understanding which deductions and credits apply to your unique situation.

Maximize Retirement Contributions

One of the most powerful tax-reduction strategies is contributing to tax-advantaged retirement accounts.

- 401(k)s: If offered by your employer, contributing to a traditional 401(k) allows you to defer taxes on your contributions and earnings until retirement. This reduces your current taxable income. Many employers also offer a matching contribution, which is essentially free money. Roth 401(k)s, while not providing an upfront tax deduction, allow for tax-free withdrawals in retirement.

- Individual Retirement Accounts (IRAs): Similar to 401(k)s, traditional IRA contributions may be tax-deductible, reducing your current taxable income. Roth IRAs offer tax-free growth and withdrawals in retirement, provided certain conditions are met, making them ideal for those who anticipate being in a higher tax bracket later in life. The choice between Traditional and Roth depends on your current income, expected future income, and tax bracket.

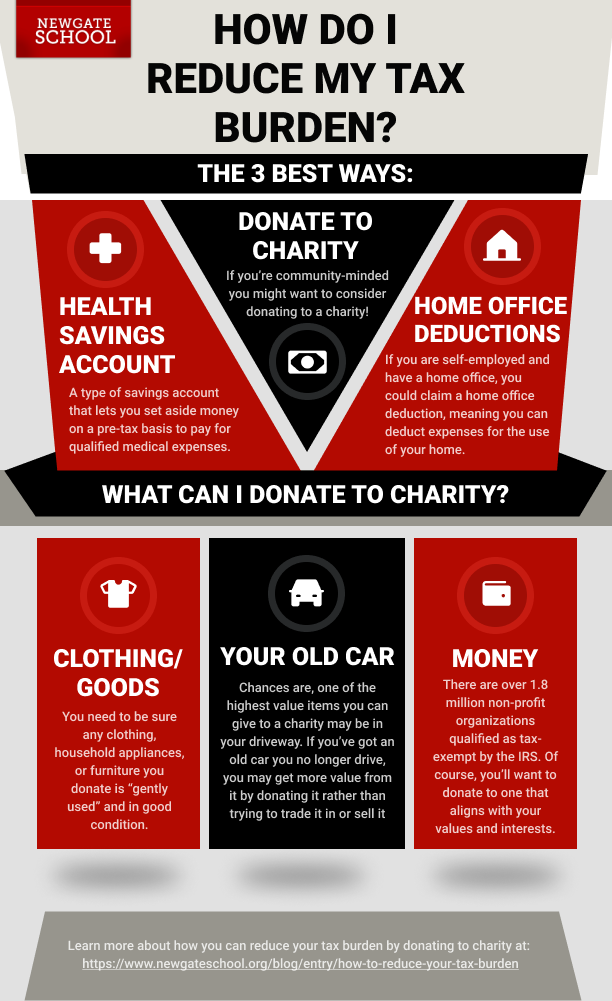

Utilize Health Savings Accounts (HSAs)

HSAs are often called the “triple tax advantage” accounts, making them an incredibly powerful tool for those with high-deductible health plans (HDHPs).

- Tax-Deductible Contributions: Contributions to an HSA are tax-deductible, reducing your taxable income in the year they are made.

- Tax-Free Growth: The money in an HSA grows tax-free.

- Tax-Free Withdrawals: Withdrawals are tax-free when used for qualified medical expenses at any age. After age 65, you can withdraw funds for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income. HSAs can effectively serve as an additional retirement account if medical expenses are managed wisely.

Leverage Tax-Advantaged Investment Accounts

Beyond retirement and health, other accounts offer specific tax benefits:

- 529 Plans: Designed for educational savings, contributions to 529 plans grow tax-free, and withdrawals for qualified educational expenses are also tax-free. Some states even offer a state income tax deduction for contributions.

- Capital Gains Strategies: Understanding the difference between short-term (taxed at ordinary income rates) and long-term (taxed at lower capital gains rates) capital gains can help you strategize asset sales. Additionally, tax-loss harvesting (discussed later) can offset capital gains.

- Taxable Brokerage Accounts: Even in standard investment accounts, strategies like investing in tax-efficient funds (e.g., municipal bonds for tax-free interest) or holding investments for the long term can minimize your annual tax liability.

Claim Eligible Deductions and Credits

Staying informed about available deductions and credits is crucial.

- Itemized vs. Standard Deduction: Always evaluate whether itemizing deductions (mortgage interest, state and local taxes up to a limit, charitable contributions, medical expenses above a certain threshold) would result in a larger deduction than the standard deduction.

- Homeownership: Mortgage interest deduction (within limits) and property tax deductions can significantly reduce taxes for homeowners.

- Student Loan Interest: You can deduct a limited amount of student loan interest paid during the year.

- Dependent Care Credit: If you pay for childcare while you work or look for work, you might be eligible for this credit.

- Education Credits: The American Opportunity Tax Credit and Lifetime Learning Credit can help offset higher education expenses.

- Energy-Efficient Home Improvements: Certain home improvements might qualify for residential clean energy credits.

Tax Optimization for Businesses and Self-Employed Individuals

For entrepreneurs and small business owners, tax planning becomes even more intricate, but also offers a broader array of opportunities to reduce tax liability through business structure, deductions, and specialized retirement plans.

Choosing the Right Business Structure

The legal structure of your business has profound tax implications:

- Sole Proprietorship: Simple to set up but offers no legal distinction between you and your business. Profits are taxed on your personal income tax return.

- Limited Liability Company (LLC): Provides liability protection. Can be taxed as a sole proprietorship, partnership, or even an S-Corp or C-Corp, offering flexibility in tax treatment.

- S-Corporation (S-Corp): Avoids double taxation (profits taxed at both corporate and individual levels). Income and losses are passed through to the owners’ personal income without being subject to corporate tax rates. Owners can also pay themselves a “reasonable salary,” which is subject to payroll taxes, but then distribute remaining profits as “distributions,” which are not subject to self-employment taxes (Social Security and Medicare), leading to significant savings.

- C-Corporation (C-Corp): Subject to corporate income tax rates, and then dividends paid to shareholders are taxed again at the individual level (double taxation). However, C-Corps offer greater flexibility for reinvesting profits within the business and can be attractive for businesses planning to raise capital or go public.

Consulting with an accountant or tax attorney is crucial to determine the most advantageous structure for your specific business.

Maximizing Business Deductions

Businesses can deduct almost any ordinary and necessary expense incurred in the course of business.

- Operating Expenses: Rent, utilities, supplies, marketing, insurance, legal and accounting fees are all deductible.

- Depreciation: For long-lived assets like equipment, vehicles, and buildings, you can deduct a portion of their cost over their useful life. Section 179 deduction and bonus depreciation allow you to deduct a significant portion, or even the full cost, of certain assets in the year they are placed in service.

- Home Office Deduction: If you use a part of your home exclusively and regularly for business, you can deduct a portion of your home expenses (mortgage interest, property taxes, utilities, insurance, repairs).

- Vehicle Expenses: Business use of your personal vehicle can be deducted using either the standard mileage rate or actual expenses (gas, oil, repairs, insurance, depreciation).

- Travel and Entertainment (Limited): Business travel expenses are deductible. While the deduction for business meals is generally 50%, some rules (like for restaurant meals in 2021-2022) might offer 100% deduction.

- Employee Benefits: Health insurance premiums, retirement plan contributions, and other benefits provided to employees are deductible business expenses.

Retirement Plans for the Self-Employed

Self-employed individuals have excellent options for saving for retirement while reducing their taxable income:

- SEP IRA: Simple to set up, allows for very high contribution limits (up to 25% of compensation or a maximum dollar amount, whichever is less). Contributions are tax-deductible.

- Solo 401(k): Ideal for business owners with no employees (other than a spouse). Allows for both employee (deferral) and employer (profit-sharing) contributions, potentially leading to even higher tax-deductible contributions than a SEP IRA.

- SIMPLE IRA: A good option for small businesses with a few employees, offering lower administrative costs than a traditional 401(k).

Understanding Estimated Taxes and Quarterly Payments

For self-employed individuals and those with significant income not subject to withholding, it’s essential to pay estimated taxes quarterly. The IRS requires you to pay income tax as you earn or receive income throughout the year. Failing to do so can result in penalties. Calculating and paying estimated taxes correctly ensures you stay compliant and avoid unwelcome surprises at tax time.

Advanced Tax Planning Techniques

Beyond the common strategies, more sophisticated techniques can further optimize your tax position, especially for those with higher incomes or complex financial situations.

Tax-Loss Harvesting

This strategy involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. If your capital losses exceed your capital gains, you can deduct up to $3,000 of the net loss against your ordinary income each year. Any remaining loss can be carried forward indefinitely to offset future gains. This is a powerful tool to manage investment portfolios and minimize tax on profits.

Gifting Strategies and Estate Planning

Strategic gifting can reduce your taxable estate and support loved ones while minimizing gift taxes.

- Annual Gift Tax Exclusion: You can give away a certain amount each year (e.g., $18,000 per recipient in 2024) to as many people as you want without incurring gift tax or using up your lifetime exclusion.

- 529 Plans and Medical/Educational Payments: Direct payments to educational institutions or medical providers for someone else are not considered taxable gifts, regardless of the amount.

- Estate Planning: For larger estates, techniques like trusts (e.g., irrevocable trusts) can be used to remove assets from your taxable estate, reducing potential estate taxes for your heirs.

Charitable Contributions

Donating to qualified charities can provide a tax deduction.

- Cash Donations: Generally deductible up to 60% of your Adjusted Gross Income (AGI).

- Non-Cash Donations: Donating appreciated stock or other property held for more than a year can be particularly tax-efficient. You can deduct the fair market value of the asset and avoid paying capital gains tax on the appreciation.

- Donor-Advised Funds (DAFs): These allow you to make an irrevocable charitable contribution, receive an immediate tax deduction, and then recommend grants from the fund to specific charities over time. This is excellent for lumping contributions in a high-income year and distributing them later.

Geopolitical and State-Level Considerations

Tax considerations aren’t limited to federal law. State and local taxes can vary significantly.

- State Income Tax: Some states have no state income tax, while others have high rates. Residency planning can be a factor for individuals with flexibility.

- Property Taxes: These vary widely by locality and can be a significant deduction (though capped at $10,000 for state and local taxes, or SALT, at the federal level).

- Sales Tax: While not typically a direct deduction, understanding how sales tax impacts purchasing decisions can be part of overall financial planning.

The Role of Professional Guidance and Tools

While understanding these strategies is crucial, implementing them effectively often benefits from professional expertise and the right tools.

When to Hire a Tax Professional

For most people, a professional tax preparer is a valuable asset.

- Complexity: If your financial situation is complex (e.g., you own a business, have significant investments, multiple income streams, or international income), a Certified Public Accountant (CPA) or Enrolled Agent (EA) can ensure compliance and identify overlooked savings.

- Staying Updated: Tax laws change frequently. Professionals stay current with these changes, ensuring you benefit from new provisions and avoid potential pitfalls.

- Audit Support: In the rare event of an audit, a professional can represent you and navigate the process.

- Strategic Planning: A good tax advisor does more than just prepare your return; they offer year-round advice on financial decisions that impact your taxes.

Utilizing Tax Software and Financial Tools

For simpler tax situations, and even for those working with professionals, tax software can be immensely helpful.

- DIY Software: Programs like TurboTax, H&R Block, and TaxAct guide you through the process, helping you identify deductions and credits.

- Accounting Software: For businesses, tools like QuickBooks or Xero integrate with tax preparation software, streamlining the record-keeping and reporting process.

- Financial Planning Apps: Many personal finance apps help categorize spending and track income, making tax preparation easier by keeping your financial data organized.

Maintaining Meticulous Records

Regardless of how you prepare your taxes, maintaining thorough and organized records is non-negotiable. Keep all income statements (W-2s, 1099s), receipts for deductible expenses, bank statements, investment statements, and previous tax returns. Digital copies are often sufficient and can be easily stored and backed up. Good record-keeping is essential for accurate filing, supports any claims you make, and is invaluable if you ever face an audit.

Conclusion

Legally reducing your tax burden is not about finding loopholes; it’s about making informed financial decisions within the framework of existing tax laws. From maximizing contributions to retirement accounts and health savings accounts to strategically structuring your business and leveraging advanced investment techniques, the opportunities to optimize your tax position are numerous.

The key to successful tax avoidance is proactive, year-round planning. It requires continuous education, diligent record-keeping, and often, the guidance of experienced tax professionals. By treating tax planning as an integral part of your overall financial strategy, you empower yourself to retain more of your income, accelerate wealth accumulation, and achieve your financial goals with greater efficiency. Embrace the power of intelligent tax planning – it’s one of the most impactful ways to build a stronger financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.