In an increasingly digital financial landscape, the humble bank check might seem like a relic of a bygone era. Yet, for specific transactions—particularly those involving significant sums, high stakes, or the need for guaranteed funds—bank checks remain an indispensable tool. From purchasing a home to settling legal obligations, these financial instruments offer a level of security and assurance that digital transfers or personal checks often cannot. However, this enhanced security comes with a cost, and understanding “how much is a bank check” involves more than just a simple fee schedule. It requires a dive into the various types of checks, the factors influencing their price, and a comparison with alternative payment methods. This article aims to demystify the costs associated with bank checks, providing insights for savvy financial management.

Understanding Bank Checks: More Than Just Paper

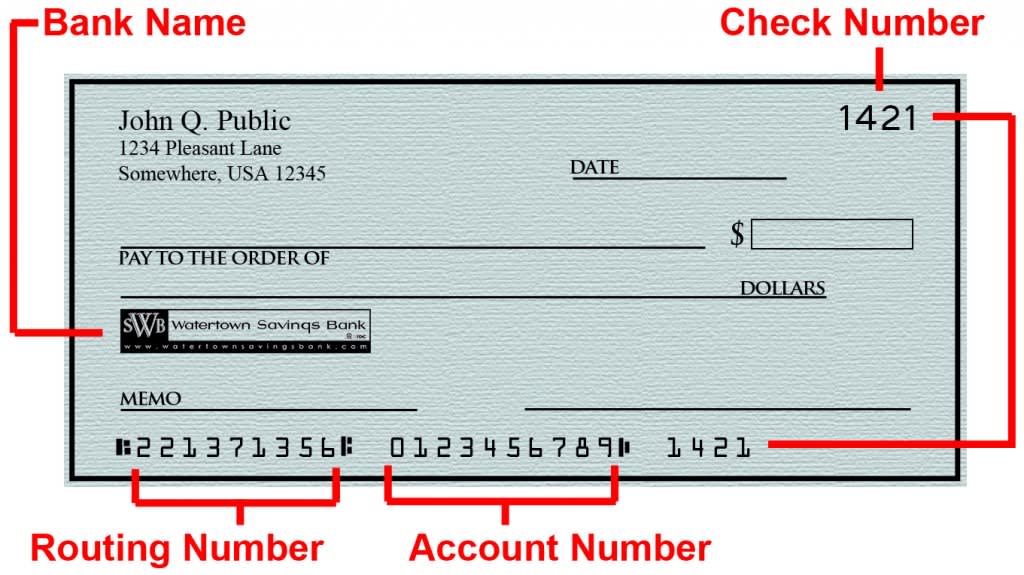

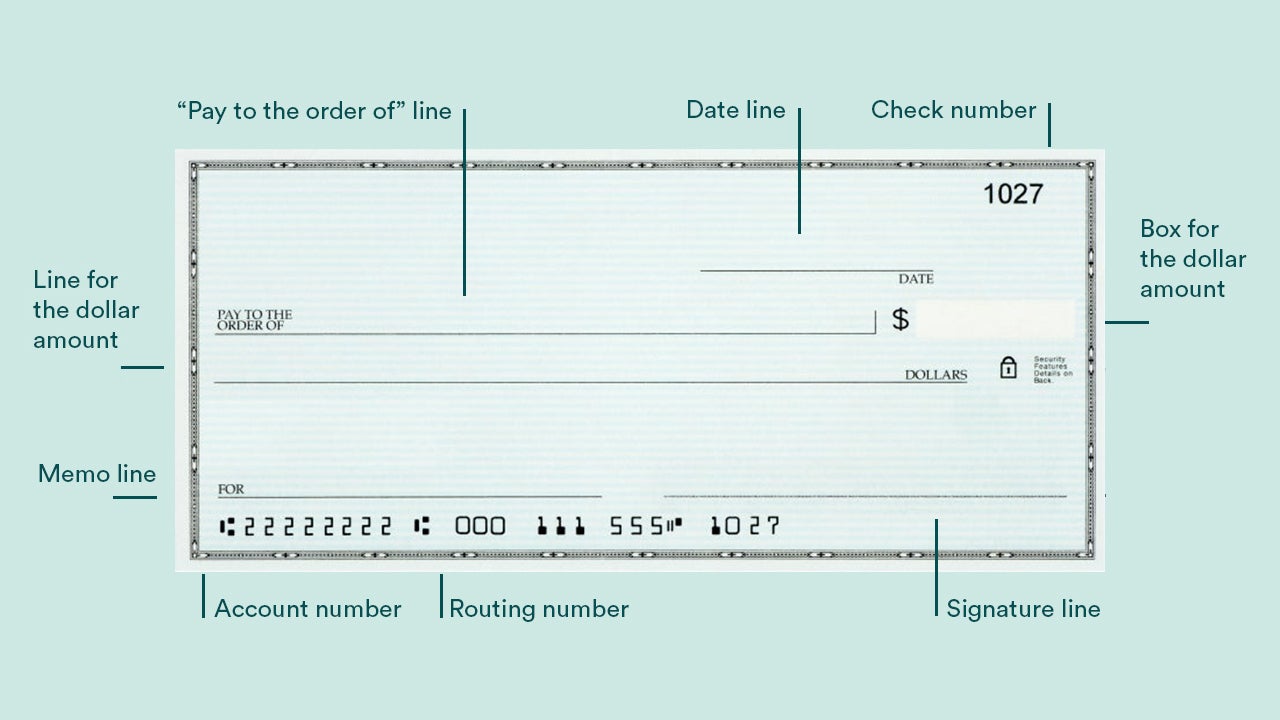

Before delving into the costs, it’s crucial to distinguish between the different types of “bank checks” often sought by consumers. While the term might broadly refer to any check issued or guaranteed by a financial institution, the specifics matter significantly when it comes to both their function and their price tag.

What Constitutes a “Bank Check”?

When people ask about “bank checks,” they are typically referring to one of two primary instruments, both fundamentally different from a personal check:

- Cashier’s Check: Issued directly by a bank or credit union, a cashier’s check draws funds directly from the financial institution’s own account, not from the customer’s personal account. The customer pays the bank the amount of the check plus any fees, and the bank then issues a check as the payer. This process ensures the funds are guaranteed by the bank itself, making it a highly secure form of payment, as it cannot bounce.

- Certified Check: This is essentially a personal check that has been verified and guaranteed by the issuing bank. The bank verifies that the account holder has sufficient funds to cover the check, earmarks those funds, and then certifies the check by stamping it. While it uses the customer’s account, the bank’s certification guarantees payment, reducing the risk for the recipient.

- Money Order: Often confused with bank checks due to their guaranteed nature, money orders are typically issued by post offices, convenience stores, or some banks for smaller amounts. They are prepaid and guaranteed but generally have lower maximum limits than cashier’s or certified checks.

The key takeaway is that both cashier’s and certified checks offer a higher level of security than personal checks because the funds are either held by the bank or guaranteed by it. This assurance is precisely why they are preferred for significant transactions, and also why banks charge for their issuance.

Why Are They Used?

The primary reasons individuals and businesses opt for bank checks revolve around trust and security, particularly for high-value transactions where the recipient needs absolute assurance of payment.

- Security for Large Transactions: For payments like a down payment on a house, a vehicle purchase from a private seller, or a significant deposit, recipients often demand a cashier’s or certified check. This protects them from the risk of a personal check bouncing.

- Proof of Funds: The issuance process of these checks inherently provides proof that the funds were available and transferred, which can be critical for legal, contractual, or tax purposes.

- Avoiding Delays: Unlike personal checks, which can sometimes be subject to holds by the receiving bank, guaranteed checks often clear more quickly, allowing transactions to proceed without unnecessary delays.

- Situations Requiring Guaranteed Funds: Certain legal settlements, court fees, or real estate closings may specifically mandate payment via a cashier’s or certified check to ensure the payment is irrevocably made.

The Cost Breakdown: Factors Influencing Bank Check Fees

The cost of a bank check isn’t uniform; it fluctuates based on several variables, primarily the type of check, the issuing institution, and your relationship with that institution. Understanding these factors is key to predicting and potentially minimizing your expenses.

Cashier’s Checks vs. Certified Checks: A Price Comparison

While both offer guaranteed funds, their pricing structures can differ slightly, though often they fall into a similar range.

- Cashier’s Checks: These generally cost between $5 and $15 per check at most traditional banks. Some banks might charge slightly more, up to $20 or $25. Because the bank is drawing from its own funds, the administrative overhead and risk assessment are reflected in this fee.

- Certified Checks: Fees for certified checks are often in a similar ballpark, typically ranging from $5 to $10. Since the funds are simply being verified and earmarked from your existing account, the administrative effort might be marginally less than generating a new check from the bank’s ledger, sometimes resulting in a slightly lower fee.

It’s important to note that these are general ranges. The exact fee can vary significantly from one financial institution to another.

Bank-Specific Fees and Policies

The institution you bank with plays a pivotal role in determining the cost.

- Major Banks (e.g., Chase, Bank of America, Wells Fargo): These large national institutions often charge standard fees within the $5 to $15 range. However, they may offer perks for certain account tiers. For instance, customers with premium checking accounts, substantial balances, or specific relationship packages might receive a certain number of cashier’s or certified checks for free each month or year.

- Credit Unions: Often lauded for their customer-centric approach and lower fees, credit unions are frequently a more economical option. Many credit unions offer cashier’s checks for free or at a significantly reduced cost (e.g., $2-$5) as a standard member benefit, regardless of account tier. This is one of the distinct advantages of banking with a credit union if minimizing such fees is a priority.

- Online Banks: While many online banks excel in low-cost everyday banking, their physical presence is limited, which complicates the issuance of physical bank checks. Some online banks may offer to mail a cashier’s check for a fee, but the process might involve delays. Others may rely on wire transfers or bill pay services as their primary large-sum transaction methods.

Additional Costs and Considerations

Beyond the initial issuance fee, other situations can incur costs.

- Stop Payments: If a bank check is lost, stolen, or needs to be canceled, initiating a stop payment order is a complex and often costly process. Because the bank has guaranteed the funds, stopping payment involves a significant administrative burden and potential risk. Fees can range from $25 to $40 or more, and typically require filling out an affidavit and waiting for a specific period for the bank to verify the check hasn’t been cashed.

- Reissues: If a check is lost and a stop payment is successfully placed, you will likely need a new check issued. This might incur another standard issuance fee in addition to the stop payment fee.

- Expedited Delivery: If you need a bank check mailed to you or a third party quickly, banks might offer expedited shipping services for an additional charge, which can vary based on urgency and destination.

Beyond the Branch: Alternative Secure Payment Methods and Their Costs

While bank checks offer unique advantages, they aren’t the only option for secure payments. Exploring alternatives can sometimes offer cost savings, greater convenience, or faster transaction times, depending on your specific needs.

Money Orders: A Lower-Cost Alternative?

For smaller sums, money orders can be a compelling alternative.

- Cost: Money orders are generally much cheaper than bank checks, often costing less than $2 each. The U.S. Postal Service (USPS) is a popular issuer, with fees typically under $2 for amounts up to $1,000. Other vendors like Walmart, grocery stores, and convenience stores also offer them with comparable fees.

- Limitations: The main limitation is the maximum amount. Most money orders cap out at $1,000, making them unsuitable for very large transactions. They are ideal for paying rent, utilities, or small purchases where cash isn’t desirable, and proof of payment is needed.

Wire Transfers: Speed and Higher Fees

![]()

Wire transfers are electronic transfers of funds directly from one bank account to another, often across different financial institutions or even international borders.

- Cost: Wire transfer fees are significantly higher than bank checks, typically ranging from $25 to $50 for domestic transfers and even more for international ones (often $35-$60+).

- Advantages: Their primary advantage is speed and immediacy. Funds can be transferred within hours or even minutes, making them ideal for time-sensitive transactions. They also offer a high degree of security once initiated.

- Disadvantages: The higher cost and the irrevocability of the transfer (once sent, it’s very difficult to retrieve) are the main drawbacks. You must be absolutely certain of the recipient’s details.

Digital Alternatives: Zelle, PayPal, and Bill Pay

For certain types of payments, various digital platforms offer speed and convenience, often at no direct cost to the sender.

- Zelle/Venmo/Cash App: These peer-to-peer payment apps allow instant transfers between individuals, usually for free. However, they are typically limited to smaller amounts (e.g., Zelle often has daily limits of $2,500-$5,000, and Venmo/Cash App have lower limits for unverified accounts). They lack the formal documentation and guaranteed-by-bank assurance of a cashier’s check, making them unsuitable for large, high-stakes transactions with unknown parties.

- Bank Bill Pay: Most banks offer free online bill pay services that can send payments to individuals or businesses. While often electronic, some banks can mail a paper check (similar to a personal check) on your behalf. These are free but lack the guaranteed funds aspect of a cashier’s check and are subject to normal check clearing times.

- ACH Transfers: Automated Clearing House (ACH) transfers are electronic funds transfers from one bank to another, used for direct deposit, bill payments, etc. While typically free for consumers, they are not instantaneous and do not offer the “guaranteed funds” aspect for the recipient in the same way a cashier’s check does upon receipt.

While digital options excel in convenience and low cost for everyday transactions, they rarely fully replace the specific assurances offered by a bank check for very large, high-risk, or legally mandated payments.

Smart Strategies for Minimizing Bank Check Expenses

Understanding the costs is one thing; actively working to reduce them is another. With a little planning and awareness, you can often mitigate or even eliminate fees associated with bank checks.

Leveraging Your Bank Account Benefits

Your existing banking relationship might already offer solutions.

- Premium Accounts: Many banks waive fees for cashier’s or certified checks for customers holding premium checking accounts, those with high average daily balances, or those who maintain specific investment relationships with the bank. Review your account’s fee schedule or speak with a bank representative to understand if you qualify.

- Relationship Pricing: Some institutions offer “relationship pricing” where fees are reduced or waived if you utilize multiple services (e.g., checking, savings, mortgage, investments) with them.

- Credit Union Membership: As mentioned, credit unions are a fantastic resource for lower fees across the board, including bank checks. If you frequently need guaranteed funds, opening an account with a local credit union might be a smart financial move.

Planning Ahead: Avoiding Rush Fees

While not always applicable to bank checks directly, the principle of planning can save money. If you need a check mailed or an alternative service like a wire transfer, avoiding last-minute requests can prevent expedited processing or shipping fees. Always allow ample time for standard processing and delivery.

Exploring Credit Unions and Online Banks

If your current bank charges prohibitive fees and you don’t qualify for waivers, consider diversifying your banking relationships.

- Credit Union Account: Even if it’s not your primary bank, having an account at a credit union specifically for services like cashier’s checks can be a cost-effective strategy.

- Online Banking for Everyday Needs: While online banks might not always be the best for immediate physical bank checks, they often offer competitive rates, low or no monthly fees, and free ACH transfers, which can save money on other types of transactions.

The Value Proposition: When Is a Bank Check Worth the Cost?

Despite the fees, bank checks retain their value in specific scenarios where the benefits of security, certainty, and official documentation outweigh the expense. Understanding these situations helps justify the cost and ensures you’re making the most appropriate payment choice.

Mitigating Risk in High-Value Transactions

For life’s most significant financial milestones, risk mitigation is paramount.

- Real Estate Purchases: When making a down payment or closing on a home, a cashier’s check provides irrefutable proof of funds that satisfies all parties and legal requirements.

- Vehicle Purchases: Buying a car from a private seller often involves a cashier’s check to ensure the seller receives guaranteed funds before relinquishing the title.

- Large Investments/Deposits: Certain investment opportunities or large deposits may require a guaranteed check to ensure the funds are immediately available and irrevocably committed.

In these situations, the few dollars spent on a bank check are a small price to pay for the peace of mind and transactional security they provide.

Ensuring Payment Certainty for Recipients

From the recipient’s perspective, a bank check eliminates the uncertainty inherent in personal checks.

- Business Transactions: Suppliers or service providers dealing with new clients or high-value contracts may request a cashier’s check to ensure prompt and guaranteed payment.

- Legal Settlements: In court-ordered payments, restitution, or large settlement disbursements, the certainty of a guaranteed check is often a legal requirement.

- Avoiding Fraud: For sellers or recipients concerned about fraudulent checks, a bank-guaranteed instrument significantly reduces their exposure to risk.

Legal and Practical Requirements for Certain Payments

Sometimes, the choice isn’t optional; it’s a mandate.

- Escrow Payments: Funds held in escrow, particularly in real estate, often require cashier’s checks to guarantee the funds are legitimate and will not bounce.

- Court Fees and Fines: Many courts will only accept guaranteed funds for specific fees or fines, especially those of a higher value, to ensure payment is received.

- Government Agencies: Certain federal or state agencies may require guaranteed funds for specific permits, licenses, or tax payments.

In these instances, “how much is a bank check” becomes a secondary concern to the imperative of meeting a specific requirement. The small fee is an unavoidable cost of doing business or fulfilling an obligation.

In conclusion, while the digital age offers myriad payment options, bank checks—cashier’s and certified checks in particular—continue to serve a vital role for secure, high-value, and legally mandated transactions. The costs, typically ranging from $5 to $15, are an investment in security and certainty. By understanding the different types of checks, the factors influencing their fees, and exploring alternatives, consumers can make informed financial decisions, ensuring they choose the most appropriate and cost-effective payment method for their specific needs. Smart financial management involves not just avoiding unnecessary expenses, but also recognizing when a particular cost provides indispensable value.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.